Cloudera and Hortonworks Are a Match Made Underwater

Cloudera and Hortonworks Are a Match Made Underwater

(Bloomberg Opinion) -- Sometimes the universe offers up a gift of symbolism. One corporate merger this week reveals the hangover of the mini-bubble that quietly burst in Silicon Valley.

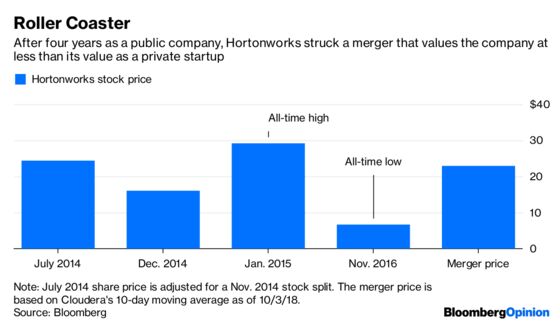

On Wednesday, two young software companies, Hortonworks Inc. and Cloudera Inc., said they planned to combine. Hortonworks shareholders will trade in their stock for Cloudera’s at an effective value of $22.82 for each Hortonworks share, based on the moving average share price over the 10 prior trading days. Remember that number.

More than four years ago, before Hortonworks was a public company, it sold shares to a group of investors at a price that was higher than this week’s effective merger price: $24.37 a share. That means that after more than four years, Hortonworks’ value in its merger still didn’t return the company to its 2014 worth.

I’m not saying Hortonworks didn’t get every penny it could in deal negotiations with Cloudera. The company’s notoriously aggressive bankers, Qatalyst Partners, would have seen to that.

My point is that the Hortonworks deal spotlights the aftereffects of a peculiar time in recent technology history when investors’ money seemed to flow almost indiscriminately into young and fast-growing companies like Hortonworks (and Cloudera). Saner heads prevailed, investors got a bit more picky after 2015 or so, and after a little-noticed reset in startup valuations the cash spigot is flowing like never before to a select group of hot tech newcomers.

So what, then? No harm done? Even those 2014 Hortonworks stock buyers — including the company then called Hewlett-Packard, Yahoo and the startup investment firm Benchmark — may not still hold the Hortonworks shares they bought at the time. In the case of Benchmark and Yahoo, they bought Hortonworks stock at several points before the IPO and most likely still made a profit on their investment.

It’s not clear from Hortonworks disclosures whether the company’s employees have stock that was tied to the inflated value of the company before its IPO. Workers are often the big losers when tech companies are overvalued and then deflate.

Hortonworks has moved on from its headline-grabbing valuation decline in 2014. Its investors, and those of Cloudera, reacted warmly to the companies’ union. Shares of Cloudera climbed about 9 percent on Thursday. Thanks to that stock spike, Hortonworks stock is now worth about $24.39 a share — a touch higher than the 2014 private stock sale.

The kicker in all this: Cloudera, too, is valued lower today on the stock market than it was when it was a private tech company. It’s a perfect, seafaring union of two underwater companies.

Several years before Cloudera’s IPO last year, the company sold shares in a private transaction for $30.92 each. On Thursday, after the stock spiked on enthusiasm about its Hortonworks merger, Cloudera shares changed hands at $18.70 each.

It was the computer chip company Intel Corp. that bought $742 million in Cloudera stock from the company, early investors and employees at that effective price of $30.92 in 2014, when startup investing was at a fever pitch. Intel made the stock purchase for strategic reasons to keep a closer eye on Cloudera and grab a seat on its board, and therefore didn’t mind if it was overpaying. It’s now clear that Intel, which remains the largest stockholder in Cloudera, drastically overpaid for its shares. It’s also not clear that the strategic benefits of investing in Cloudera were worth it.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shira Ovide is a Bloomberg Opinion columnist covering technology. She previously was a reporter for the Wall Street Journal.

©2018 Bloomberg L.P.