CLOs Risk Starring Role in This Recession When Default Wave Hits

CLOs Risk Starring Role in This Recession When Default Wave Hits

(Bloomberg) -- Michael Lewis’s “The Big Short” told the story of CDOs, now infamous debt securities that played a starring role in the last financial crisis. This time around their cousins could be thrust center stage.

The market for collateralized loan obligations is currently pricing just a fraction of the likely wave of defaults caused by the coronavirus, according to UBS Group AG. The warning comes as a slew of data this week points to the scale of the unfolding economic collapse, with U.S. gross domestic product shrinking the most since 2008 in the first quarter.

Some of the biggest CLOs -- packages of loans to companies with speculative-grade ratings -- are heavily exposed to industries bearing the brunt of the slowdown like leisure, retail and energy. Many of those sectors are likely to languish even after lockdown measures are eased, UBS reckons.

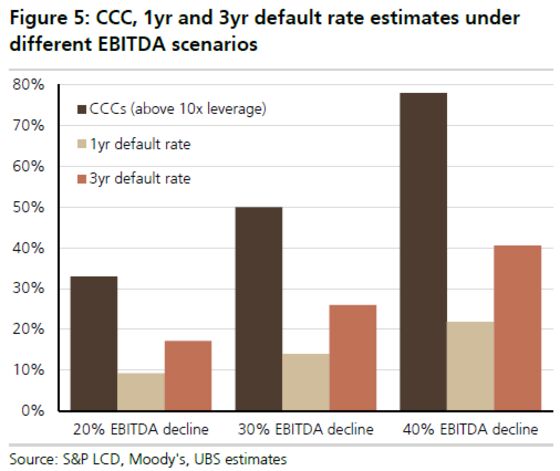

The Swiss bank forecasts default rates in the double digits and a barrage of downgrades that will push between a third and half of loan pools into the lowest CCC ratings category.

“This suggests downside risks if mobility restrictions persist or broader recessionary effects hit,” strategists including Matthew Mish wrote in a note.

Loan prices have been recovering from their March lows after the Federal Reserve pledged trillions to save financial markets from collapse, joining a remarkable rebound across risk assets even as economic data tanked. They now imply a default rate of 5% to 6%, according to UBS.

The Fed-inspired price rise is perhaps unjustified for companies hit by lockdown measures and outside the central bank’s bond-buying umbrella, according to the strategists.

“We expect widening in leveraged-loan spreads as we do not believe easing in mobility restrictions will bring demand back to normalized levels in aggregate, but more specifically for key sectors like leisure, hotels/gaming, retail and energy,” Mish and his colleagues wrote. “While the monetary and fiscal response has been robust, the leveraged-loan market overall and more specifically PE-owned, highly leveraged firms appear to have fallen (intentionally) between the cracks.”

In their optimistic scenario -- where restrictions lift in May and life gets back to normal by June -- 9% of leveraged loans would default within a year. If lockdowns are in effect until June and normalcy returns at the end of August, defaults would hit 14% of loans, they said. In the worst case -- the virus keeps returning in waves until the middle of next year -- UBS sees the rate at 22%.

Spillover

CLOs emerged from the financial crisis mostly untainted and went on to become a money spinner for Wall Street. It was collateralized debt obligations -- pools of loans to consumers, rather than businesses -- that featured in the 2008 crisis by helping fuel the housing boom and then bust.

The unprecedented shutdown in activity needed to contain the coronavirus outbreak has put companies at the front line of the 2020 crisis. S&P Global has cut or put on watch for downgrade about a fifth of the corporate loans used as collateral for CLOs it rates. And expected losses endanger the ratings of $22 billion of CLOs rated by Moody’s Investors Service.

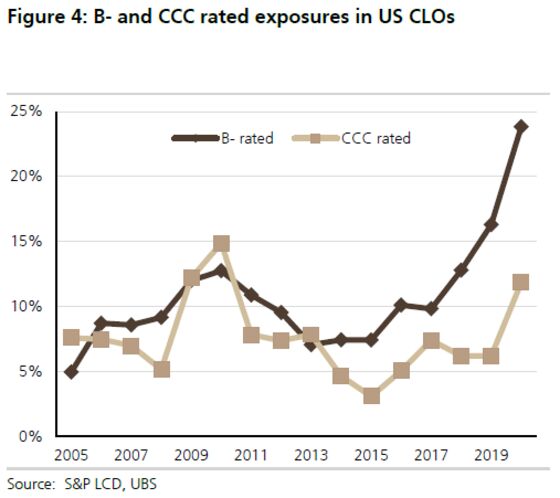

Ratings downgrades carry a bigger sting in the tail for CLO structures than for plain-vanilla bonds because too much CCC rated debt can trip up safety mechanisms. Firms that manage CLOs may be forced into fire sales of downgraded debt or compelled to gate cash payments to investors in lower-rated portions to preserve it for those at the top.

Most deals limit exposure to CCC rated debt to 7.5% of the portfolio. Any CCC loans over the limit will be subject to mark-to-market rules, which means they’ll be counted at the current trading value rather than at par, reducing the value of the entire portfolio.

Whether problems in the CLO market will spread and infect the wider economy, like CDOs, is a bigger question. Mish says a ripple effect is possible.

CLO debt is riding on the backs of the same weak middle-market companies behind the boom in private credit, potentially pressuring other leveraged industries.

“The risk of defaults in waves is really if we see the weakness in sectors most affected by Covid-19 spill over to impact other sectors like in prior recessions,” Mish said in a message.

©2020 Bloomberg L.P.