CLOs Are Finally Taking a Beating Like Rest of Credit Market

CLOs Are Finally Taking a Beating Like Rest of Credit Market

(Bloomberg) -- The once-red hot market for corporate loans bundled into securities is starting to cool as investors ponder whether the Federal Reserve may rein in rate increases to counter signs of slowing economic growth.

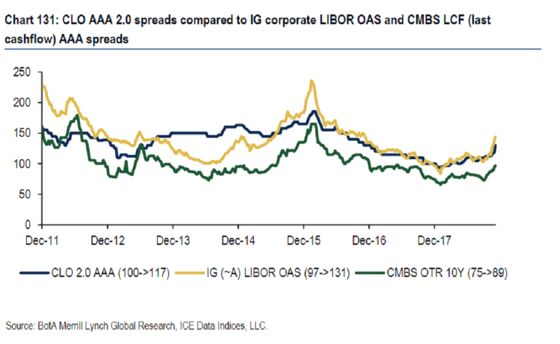

Collateralized loan obligation spreads in the secondary market have widened over the London interbank offered rate more than investment-grade corporate bonds for the first time this year. It’s a sign the weakness seen across credit markets for months, especially in the leveraged loans that make up CLOs, has finally caught up to the asset class.

Spreads of CLOs rated BBB -- just above junk status -- have widened as much as 60 basis points since the beginning of December, according to Citigroup Inc.

The risk that investors may be unable to make a timely exit from the securities and chances of fewer Fed hikes are to blame for the CLO market’s sudden weakness, Bank of America Corp. analysts said in a recent note.

“Liquidity remains challenged heading into year-end, with more investors choosing to stay on the sidelines,” a team of Bank of America analysts led by Chris Flanagan wrote in a Dec. 14 research report. “CLOs’ relatively contained spread widening compared to other products earlier this quarter means some catch-up may still loom on the horizon.”

Tumbling leveraged loan prices, which have fallen since October to a more than two-year low this week, are also weighing on the instruments that bundle them into securities. Since the loans are tied to floating rates and benefit from increases, expectations the Fed could reduce the number of hikes next year has made them less attractive to investors. CLOs add in buffers for investors for more protection.

A record supply this year and higher costs for Asian investors due to a stronger dollar have also driven CLO spreads wider.

CLOs are finally seeing the weakness that spread through most of the credit market over the last few months. They have outperformed everything else all year, and still have higher returns year-to-date than high-grade debt.

“If you look at the recent two weeks’ spread widening, then yes, CLO AAAs have widened slightly more (than corporates), but year-to-date, total-return-wise, CLO investment-grade tranches are still outperforming high-grade corporate bonds,” said Citigroup analyst Lijing Wang in an interview.

To contact the reporter on this story: Adam Tempkin in New York at atempkin2@bloomberg.net

To contact the editors responsible for this story: Christopher DeReza at cdereza1@bloomberg.net, Randall Jensen, Dave Liedtka

©2018 Bloomberg L.P.