CLO Sales Reach $14 Billion in Busiest Month Since Early 2019

CLO Sales Reach $14 Billion in Busiest Month Since Early 2019

(Bloomberg) -- Sales of collateralized loan obligations rebounded in October as managers raced to get ahead of the U.S. presidential election and yield-hungry investors bought into a sector that’s lagged a broad rally in credit markets.

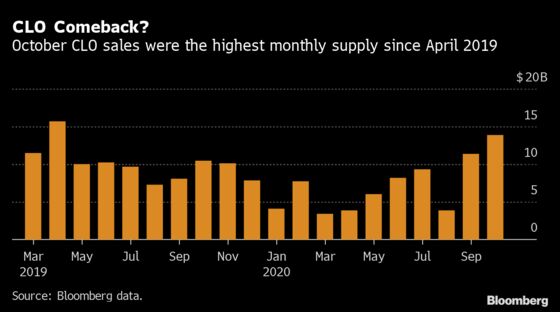

U.S. CLO volume reached $13.8 billion last month, a 20% increase over September and the most since $15.7 billion was issued in April 2019, according to data compiled by Bloomberg. Overall, 2020 sales stand at about $72 billion, down 30% compared to the same point last year.

“The explosion in CLO deal flow this autumn is greater than what we originally hoped for,” said Larry Berkovich, a partner at Allen & Overy, who represents CLO managers. “There’s a sense of current optimism.”

New sales shut down for nearly a month back in March as the pandemic rocked markets. Transactions started picking up steam in mid to late April, buoyed by improving economics for the deals in which portfolio managers package and sell leveraged loans into chunks of varying risk and return.

Liability spreads on AAA slices have nearly retraced to pre-Covid levels, and currently stand at 135 basis points to 140 basis points over Libor for top-tier managers. That’s a vast improvement from the early days of the pandemic, when CLO AAA spreads widened to as much as 230 to 250 basis points, depending on the manager.

Spread tightening has been key in improving the so-called arbitrage -- the gap between the interest earned from the underlying leveraged loans and the cost of borrowing to purchase the assets. A healthier arbitrage enhances the economics of the transactions, which makes it easier to attract CLO equity capital to sponsor new deals.

The recovery in securitized credit has generally lagged that of corporate bonds, making the sector an appealing source of relative value for investors. Structural protections embedded at the AAA ratings tier, combined with leveraged-loan prices that have rallied from March lows and remain stable, are also helping fuel investor interest.

The month-over-month spike in issuance “contradicts election-year supply trends,” JPMorgan Chase & Co. analysts led by Rishad Ahluwalia wrote in a Monday research note. “In the previous five election years since 2000, supply decreased from September to October by an average negative 32%, with the exception being 2016, when it was flattish.”

Of course, there was no pandemic to contend with during those years, and hence no pent-up demand spurring a late-year return to normality.

“Looking at current trends and how quickly spreads have tightened, there’s no indication that CLO issuance shouldn’t go up next year,” said Allen & Overy’s Berkovich. “But that could very quickly be qualified by the election results, as well as what kind of further support comes from Congress and from the Federal Reserve to prop up the economy.”

©2020 Bloomberg L.P.