CLO Market Faces Record Callable Debt Just as Sentiment Turns

CLO Market Faces Record Callable Debt Just as Sentiment Turns

(Bloomberg) -- A record amount of collateralized loan obligations will be eligible to be reset or refinanced next month, potentially putting more pressure on prices. But the concerns may be for naught as the malaise weighing on credit markets could derail part of the push.

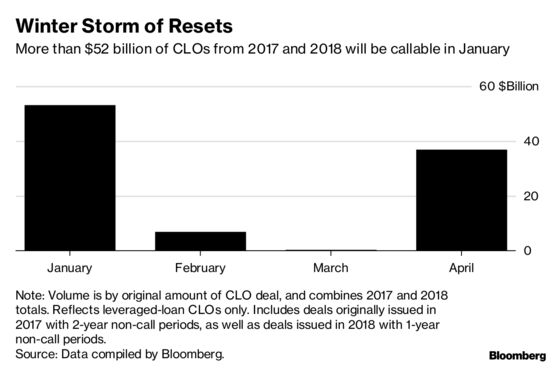

More than $52 billion of CLOs originally issued in 2017 and 2018 could be refinanced or reset in January, according to data compiled by Bloomberg. However, if spreads remain near the widest levels in over a year, the exercise may be unprofitable for many managers.

“Generally speaking, execution of refi/reset/re-issue can be more challenging compared to new-issue in a volatile environment,” JPMorgan analysts Rishad Ahluwalia and Heather Rochford wrote in a recent research note.

The fact that AAA CLO spreads are nearly as wide or wider than the original spread when they were first issued means that there is less of a cost savings for undertaking a refinancing or reset, Deutsche Bank analysts wrote in a recent report.

The start of next year could mirror what happened in the fall. In October, a then-record $20 billion of callable CLO debt issued in 2016 became eligible to be refinanced or reset, but managers only did about $6.6 billion of deals that month, according to data compiled by Bloomberg News.

CLO spreads have steadily widened since March due to a record supply this year and higher costs for Asian investors amid a strengthening dollar. The recent volatility in equity and other credit markets, including in the leveraged loans that underpin the instruments, has also added to woes.

Since leveraged loans underlying CLOs are tied to floating rates and benefit from rate increases, the Fed’s decision to reduce the number of hikes next year has made them somewhat less attractive to investors compared with earlier in the year.

Average spreads on top-rated CLO tranches have steadily widened this year amid record annual supply of $129 billion. Average AAA new-issue spreads are at about 126 basis points above the London interbank offered rate, up from March when spreads touched the tightest level since the financial crisis at 97.35 basis points, the data show. Monthly new-issue CLO sales dropped 55 percent so far in December compared with a year earlier.

This year there’s been a record $91.2 billion of CLO resets, and $35.5 billion of refinancings issued, according to data compiled by Bloomberg News. Monthly CLO reset issuance peaked this year in April at $10.9 billion, versus only $1.2 billion so far in December.

Spreads on reset CLOs have also drifted wider to an average of about 115 basis points over Libor at the beginning of December from about 104 basis points in June. Octagon Credit Partners postponed a reset of a deal originally issued in 2014 amid market turmoil earlier this month.

©2018 Bloomberg L.P.