Chorus for Long-Term Bond Bets Grows on ECB Stimulus Potential

Chorus for Long-Term Bond Bets Grows on ECB Stimulus Potential

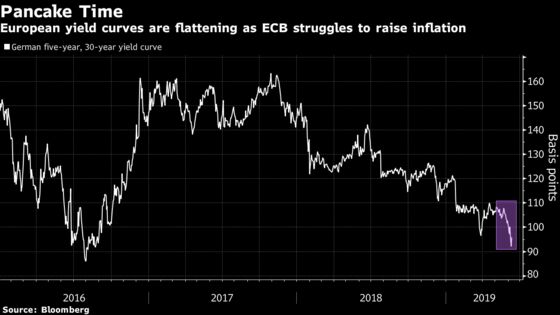

(Bloomberg) -- A worsening European economy is spurring calls for yield curves to get even flatter.

NatWest Markets, Barclays Plc and Bank of America Merrill Lynch are among those urging investors to buy longer-dated bonds instead of shorter-dated ones after the European Central Bank opened up the possibility of further stimulus measures.

The recommendations for flatter yield curves reflect fears Europe could become stuck in a low-inflationary world similar to that of Japan. Traders in money markets are now betting that the ECB will have to cut interest rates by the middle of next year, while expectations for price increases are hovering at the lowest level on record.

“The world is increasingly in a bad place,” wrote NatWest’s head of European macro research Andrew Roberts, who was among the first to predict German bund yields turning negative this year. “Buy more 10-year and 30-year European fixed income.”

Yield curves flattened Tuesday as long-end bonds rallied, taking the rate on Germany’s 30-year notes down to 38 basis points. That represented a premium of less than 100 basis points over five-year bonds, near the lowest since 2016. The whole of Germany’s yield curve up to 15 years is now negative.

Curves had steepened Monday after the U.S. postponed the imposition of tariffs on Mexico, showing the risk that any improvement in trade-conflict sentiment or euro-area data holds for those extending duration in portfolios. But that proved short-lived and speculation that the ECB may restart actively buying bonds through its quantitative-easing program is expected to continue to give support to longer-dated debt.

Any restart of QE would likely push the central bank into German securities above seven years maturity, helping to drive further flattening, given its previous requirement to only buy bonds that yield above its deposit rate. Barclays recommends investors position for a flattening of the 10-year, 30-year euro swap curve, a proxy for yield curves in the region.

“The ECB could be thought of as having taken a first step towards the ‘Japanification’ of euro curves,” said Sphia Salim, a strategist at Bank of America Merrill Lynch, in a note to clients. “Now the prospects of an ECB behind the curve or one that is willing to restart QE add to our bullish view outright and in spreads in the 10-year-plus sector.”

To contact the reporter on this story: John Ainger in London at jainger@bloomberg.net

To contact the editors responsible for this story: Ven Ram at vram1@bloomberg.net, Neil Chatterjee

©2019 Bloomberg L.P.