Chilean Assets Are at the Mercy of Sunday’s Presidential Vote

Chilean Assets Are at the Mercy of Sunday’s Presidential Vote

(Bloomberg) -- Chilean assets are in store for a volatile week in the aftermath of presidential elections that will determine if the country sticks with its free-market economy or takes a turn to the left with more regulation and social spending.

The peso and stocks have been among the world’s worst performers over the past six months amid growing speculation that left-winger Gabriel Boric could emerge as the victor in Sunday’s vote and usher in higher taxes, increased rights for workers and an end to the privately-run pension system. Analysts say his victory would likely put further pressure on asset prices, with some predicting another 10% drop for the stock market.

But a come-from-behind triumph for conservative Jose Antonio Kast could have the opposite effect as investors price in a re-commitment to the economic orthodoxy that transformed Chile over the past four decades into one of Latin America’s richest countries. Kast’s priorities include cutting taxes, fewer concessions on expanding social supports and shrinking the government’s size.

Most polls had shown Boric with a solid lead in the run-up to the vote, though more recent surveys indicated Kast was narrowing the gap. Either way, Chile is staring down its most polarized election in recent memory, along with a separate plan to rewrite the constitution, after a period of unprecedented social upheaval.

“In the past days, the market has been more inclined to see each candidate with a 50-50 chance of succeeding,” said Jorge Garcia, an investment manager at brokerage Nevasa in Santiago.

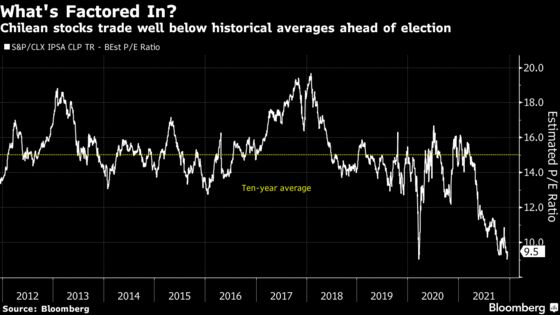

The peso has plunged 14% in the past six months, the second most among more than 30 major currencies tracked by Bloomberg. The S&P/CLX IPSA stock index is down a similar amount in dollar terms during that span, making it the sixth-worst performer among more than 90 global benchmarks.

Here’s a sampling of what analysts and economists are saying about the outlook for Chile’s markets.

Leonardo Suarez, an economist at Larrain Vial in Santiago:

- Suarez says the peso has already priced in a Boric victory, so there may not be much movement if that result is confirmed.

- “If Kast wins, we could see a temporary appreciation to around 800/USD, after which the FX rate could return to around CLP 850/USD in early 2022 due to local institutional and political uncertainty,” he wrote in a recent note to clients.

Luis Felipe Alarcon, an economist at Euroamerica in Santiago:

- A Boric victory could send the IPSA to as low as 3,900, from the current 4,400, he predicts. A Kast triumph could send the gauge to 4,900.

- In the fixed-income market, yields on 10-year government bonds could rise as much as 120 basis points if Boric wins, and fall close to 50 basis points if the opposite scenario takes hold, he said.

Caesar Maasry, an analyst at Goldman Sachs Group Inc. in New York:

- Chile’s stock valuations have fallen too far and the IPSA is likely to rally to 4,900 over the next 12 months, according to his forecasts.

- “While there is clearly great uncertainty around election outcomes and subsequent policy, the starting point appears quite low from a valuation standpoint,” he wrote in a note to clients Dec. 15.

Diego Celedon, an analyst at JPMorgan Chase & Co. in Santiago:

- Worst-case scenario was ruled out after the center-right outperformed in Chile’s legislative election.

- Still, the bank remains neutral on Chilean stocks due to political risks and 2022 constitutional referendum vote.

- A potential positive election outcome would be a source of further re-rating in the short term, but additional upside comes from policy implementation.

Guilherme Paiva and Juan Ayala, analysts at Morgan Stanley:

- The current macro framework for Chile should remain in place in 2022 regardless of who wins the race.

- “In a more heterodox macro policy scenario, we would see an initial unfavorable reaction in risk asset prices until some moderation eventually occurs.”

©2021 Bloomberg L.P.