Rahm Emanuel Shouldn’t Gamble on Chicago’s Pensions

Rahm Emanuel Shouldn’t Gamble on Chicago’s Pensions

(Bloomberg Opinion) -- Mayor Rahm Emanuel of Chicago, a former investment banker, should understand why issuing debt to fund pensions is a risky idea.

Emanuel, who is leaving office in May, told city council members on Wednesday that he would set in motion a plan for Chicago to sell what he branded as “fund stabilization bonds.” Officials have floated the prospect of an offering as large as $10 billion, which would be the largest-ever for a locality. Even that wouldn’t even completely solve the problem: Chicago’s four pension systems are underfunded by a combined $28 billion. Even with the sale, the funding status of the systems would rise to just 50 percent, still well below what any observer would consider healthy.

The city would essentially be gambling that its retirement plans could earn a long-term return greater than the interest rate it pays on the taxable securities. Say that’s 5 percent. Sure, the plans’ projected rate of return is about 7.5 percent, but does anyone really think that’s a surefire target in the years to come? Among those who are skeptical about future returns is Ray Dalio, founder of Bridgewater Associates, which has made the most money for investors in the history of the hedge fund industry.

The short-term appeal is tempting, of course. “Issuing these bonds, and depositing the proceeds directly into our pension funds, would immediately increase the health of our pension funds to levels not seen in at least a decade before asking more of Chicago’s hard-pressed taxpayers,” said Emanuel, who during his tenure has increased property taxes and utility fees to help boost pension contributions. And in a masterful spin job, the mayor warned that the clock is ticking to complete the deal because “at some point that window will close” because of rising interest rates. In reality, the market is growing doubtful that U.S. yields will move much higher from where they’ve been this year.

In August, Bloomberg News’s Chicago Bureau Chief Elizabeth Campbell asked some municipal-bond investors what they thought of the pension-bond proposal. The closest thing to praise was from from Wells Fargo Asset Management’s Dennis Derby, who said it was “a very interesting idea” because Chicago must “do something to address the pension shortfalls.” That’s not exactly a ringing endorsement. Others oppose the idea outright, in part because there might not be enough demand for the debt.

Instead of relying on a pension-bond gimmick almost 10 years after the end of a recession, when equities and other high-earning assets are showing signs of weakness, Emanuel’s final few months in office would be better spent pushing for an amendment to the state’s constitution that would allow existing benefits for public employees to be reduced. Both Chicago and Illinois, the lowest-rated U.S. state, desperately need some flexibility to stave off a full-blown crisis. He said on Wednesday that he supports such a change.

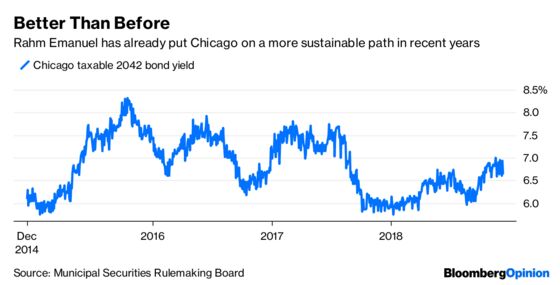

As it stands now, Emanuel would leave behind a strong track record as Chicago’s mayor, at least as far as the city’s finances are concerned. He made politically tough decisions to put the four retirement plans on a path to solvency and dealt with a surprising downgrade to junk from Moody’s Investors Service in 2015. At the time, Chicago was drawing comparisons to Detroit, which filed for bankruptcy two years earlier.

You don’t hear such talk now. But surely it would come back given Detroit’s own history with pension-obligation bonds. What happened to the investors and insurers who guaranteed $1 billion of debt from 2006 that was put into the retirement funds? Those securities were canceled, and they received $141 million in new notes and land instead. That was a worse recovery than for pensioners.

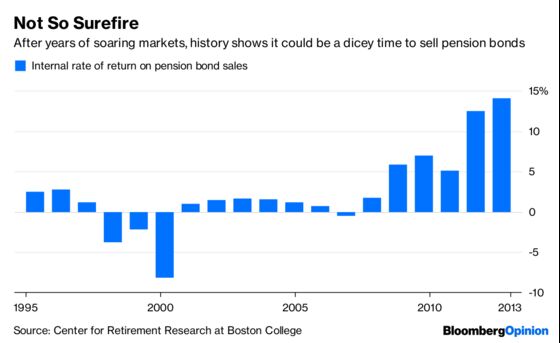

Then again, as Bloomberg News’s Danielle Moran noted, governments have occasionally come out ahead by issuing pension bonds. The caveat is that they have to correctly time the market, which clearly Detroit clearly didn’t do (the S&P 500 peaked in October 2007). Given the length of the current expansion, it seems a questionable time to throw $10 billion at the broad market and hope for success.

It ultimately comes down to whether you believe Chicago’s pension situation is salvageable by traditional means. That would be a long and arduous process. If not, what would the city really have to lose by rolling the dice?

Emanuel has built a strong enough foundation for the city to avoid gambling away its future. He said in October that “They do not build statues for people who restore fiscal stability.” Well, history looks even less fondly on those who make rash financial decisions that only make the situation worse.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2018 Bloomberg L.P.