Campbell Isn't Any Worse, But Can It Get Better?

Campbell Isn't Any Worse, But Can It Get Better?

(Bloomberg Opinion) -- At least Campbell Soup Co.’s new CEO, Mark Clouse, isn’t starting off his tenure with any major surprises.

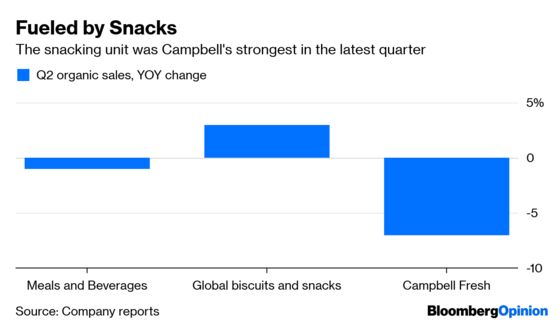

The packaged-food behemoth reported Wednesday that organic sales, a measure that excludes acquisitions and other factors, were about flat from a year earlier. Campbell’s global biscuits and snack division provided strength, with brands such as Pepperidge Farm and Goldfish selling well. The meals and beverages unit, which includes its namesake soup line, struggled, with organic sales declining 1 percent from a year earlier. Its fresh-food unit, meanwhile, was a serious drag on overall results.

The company reaffirmed its full-year guidance, a sign that this quarter landed about how executives had expected.

Campbell’s latest results offer some validation of the strategy that an interim CEO who preceded Clouse had laid out for the company. The plan is to find buyers for its international business and the fresh division. I’ve noted before I thought dumping the fresh business was a logical move, and this quarter’s results make it easy to see why. But they also raise a key question: Who is going to want to take it off Clouse’s hands?

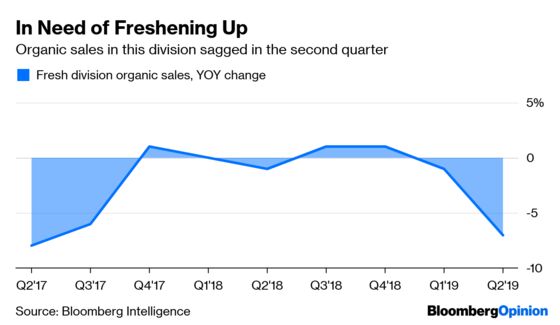

Organic sales at Fresh slumped 7 percent from a year earlier, a worse result than had been seen in recent quarters on this measure. Its operating loss was $14 million, steeper than the $11 million loss in the same quarter last year.

The company had cautioned this division would feel more pain in 2019 as two of its major contracts for private-label refrigerated soup weren’t renewed. The absence of this business was cited in the press release as a reason for the sales decline – but it wasn’t the only reason. The company also recorded weakening sales of its Bolthouse Farms refrigerated beverages and Garden Fresh Gourmet products. And the $346 million impairment charge that Campbell took on the division in the quarter doesn’t exactly support the notion that this business is a diamond in the rough.

Clouse’s best hope for selling the remaining fresh brands is an appeal to the fact that they are, on paper, a great fit for changing consumer eating habits. Shoppers are gravitating toward fresh, refrigerated items that they perceive as healthier than shelf-stable ones. Clouse could make the case that Campbell simply isn’t the right steward for these assets, but someone else could be.

Campbell already has made some modest progress on its bid to walk away from the fresh business. It announced earlier this month that it reached an agreement to sell one of its plants for manufacturing refrigerated soup. On Tuesday, it said it had struck a deal for its Garden Fresh Gourmet business to be sold. So perhaps that offers some hope that there will be interest in the remaining Bolthouse Farms business, which includes carrots.

I suppose Campbell investors can take some comfort in the fact that the international brands might be an easier sell. Arnott’s biscuits, for example, contributed to organic sales growth in the biscuits division this quarter.

Of course, saving Campbell will require more than dealmaking, and some of what Clouse said on his first earnings call with investors sounded on point to me. In particular, he cited the need to “improve the value proposition” of its core soup business, including by rethinking its pricing and promotion strategy for that product. Lowering prices and investing in marketing could indeed be helpful, especially at a moment when grocers are coming on strong with their own private-label goods. (This is the dynamic Warren Buffett cited earlier this week in talking about the headwinds facing Kraft Heinz Co., a business in which his Berkshire Hathaway Inc. is a major shareholder.)

Still, the food business overall is at a crossroads, making for challenges across the board. Just look at the Wednesday plunge in shares of Dean Foods Co., which has made investors jittery with its announcement that it is considering a sale.

Clouse has plenty of difficult work ahead. The faster he can unload the rest of the fresh division, the better.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Sarah Halzack is a Bloomberg Opinion columnist covering the consumer and retail industries. She was previously a national retail reporter for the Washington Post.

©2019 Bloomberg L.P.