Buyer Beware of States With a High Number of Muni Bankruptcies

Buyer Beware of States With a High Number of Muni Bankruptcies

(Bloomberg) -- Municipal bankruptcies are so rare that bondholders scour each for potential precedents. But they’re far more common in some states than others, according to data from Municipal Market Analytics Inc.

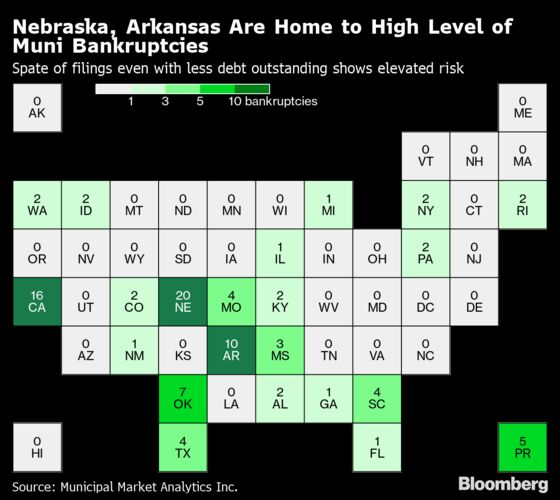

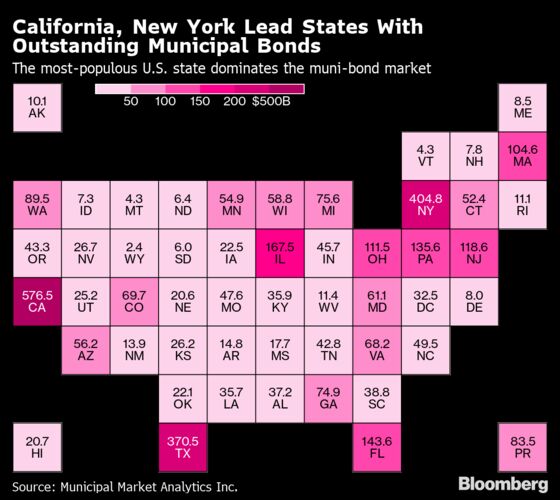

Of the 94 filed since 2007, California saw 16, the second most, MMA figures show. That’s understandable given the most populous U.S. state’s dominance among bond issuers in the $3.8 trillion market and its permissive attitude to such filings, which included the cities of Vallejo, Stockton and San Bernardino.

But more surprising: Nebraska has the highest number of failures with 20, although issuers in the state represent just 0.57% of municipal debt outstanding. Arkansas is third with 10 filings, though it accounts for just 0.41% of outstanding debt. In both states, special districts that finance development projects -- not cities with broad tax power -- have driven most of the bankruptcies, although the most recent Arkansas case was a tiny rural town facing a water bill bigger than its budget.

Local governments and agencies can only seek court protection based on state law, so it’s natural that some states have more. Cities in Illinois, for instance, can’t file. It also shows that municipal professionals encouraging bankruptcies are likely to influence similar decisions for other clients in the state, said Matt Fabian, a partner at the Concord, Massachusetts-based research firm.

“An investor has to assume an elevated risk of restructuring,” he said.

Fabian isn’t recommending avoiding debt from the high-bankruptcy states. But he suggests investors demand more in return for the risk, if possible in a market where yields are very low. He also said they should be prepared to do more surveillance on the bond issuer after buying its debt and insist on more disclosures than is typically required beforehand.

“Maybe you make the banker work a little bit harder before you buy the bond,” he said.

--With assistance from Cedric Sam.

To contact the reporter on this story: Romy Varghese in San Francisco at rvarghese8@bloomberg.net

To contact the editors responsible for this story: James Crombie at jcrombie8@bloomberg.net, Michael B. Marois, William Selway

©2019 Bloomberg L.P.