Wiped Out Once Again, Argentina Bulls Sift Through the Ashes

Burned Again, Argentina’s One-Time Bulls Sift Through the Ashes

(Bloomberg) -- There are sell-offs and there are sell-offs. But what occurred in Argentina last week is on a scale of its own.

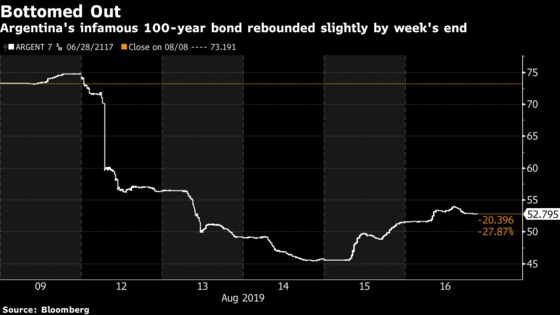

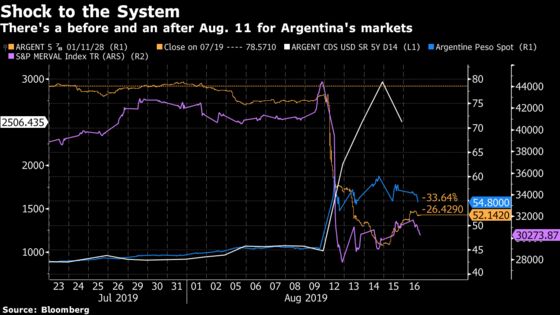

The local stock market tanked 45% in dollar terms and bond prices tumbled 34% after a surprise in the primary election Aug. 11 that was widely seen as foretelling a victory for the opposition populists when the presidential vote takes place in October. The peso tumbled 18% while credit-default swaps blew out so much that the implied chance of missed payment over five years surged to 80%. Funds managed by Michael Hasenstab of Franklin Templeton absorbed losses of almost $2 billion in just two days.

The tectonic shift in Argentine risk assessment was so violent because inaccurate polling meant so few saw it coming, and now investors are left to sort through the ramifications. South America’s second-biggest economy has traditionally been a market of booms and busts, and some one-time bulls who got burned last week may see no option but to either sell at heavy losses or find a new narrative to try to convince themselves -- and their furious clients -- that this was just a temporary setback.

What if Alberto Fernandez, the candidate who has vowed to undo at least some of President Mauricio Macri’s market-driven reforms, isn’t so bad? What if he’s more like Luiz Inacio Lula da Silva, the former labor leader who led Brazil to a long bout of prosperity after a 2002 election victory that terrified investors? What if the new government can get an IMF deal like the one that sparked a rally in Ukraine’s bonds in 2015?

“If he names a team with credibility and seeks a debt re-profiling under the IMF program, it could be positive,” said Alejo Costa, a strategist at BTG Pactual Argentina in Buenos Aires. “They could extend maturities, have some room to reduce financing needs and avoid a restructuring.”

Investors want Fernandez to continue working with the IMF after the lender’s $56 billion bailout package last year, and recognize that a default wouldn’t benefit anyone. They want him to show restraint on government spending, and take advantage of the currency selloff to bolster the fiscal balance sheet and encourage growth in export-led businesses.

But that’s far from certain to happen under a Fernandez administration that includes former President Cristina Fernandez de Kirchner as his running mate. Macri took over for her four years ago after she led arguably the most radical government in Argentina in decades, nationalizing pension plans, freezing energy prices and imposing currency controls all while escalating a years-long feud with holders of bonds the country defaulted on in 2001.

“The initial signals have all been worrisome,” Siobhan Morden, Latin America fixed income strategist at Amherst Pierpont Securities in New York, wrote in a note. “The markets assume the worst on recent memory of the interventionist/isolationist strategy of the Kirchner era, while it’s difficult to expect the best without any encouragement from the Fernandez team.”

The next administration will take over in December, and the state of the economy then will be a major factor as to whether the next government will be successful.

Fitch Ratings and S&P Global Ratings came down on the side of the pessimists Friday as they cut the country’s credit rating. Fitch put the grade at CCC, a level that implies default is a real possibility.

“Both sovereign financing and solvency risks have increased,” the company said in a statement.

Of course the reality is that market players can always find a reason for optimism if their holdings require it. After all, there was a bull case for Kirchner ally Daniel Scioli if he had won the election in 2015 against Macri, basically the idea that he’d realize he would need to regain investors’ trust to survive.

While traders continue to wait for more encouraging signs from Fernandez and details on who he may name to his cabinet, bonds are cautiously trending back up. Stocks are off the worst of their lows, and the peso gained Thursday and Friday.

An adviser to Fernandez, former deputy finance minister Emmanuel Alvarez Agis, held a call with investors last week and spoke at a public event in Buenos Aires where he said the current monetary policy is the right one. Another confidant, Matias Kulfas, said Fernandez has a willingness to repay debt and is against imposing capital controls.

Kathryn Rooney, the head strategist at Bulltick LLC in Miami, says there’s a 60% chance that a Fernandez administration turns out to be more investor friendly than some fear.

The new government likely prefers to “inherit a functioning economy rather than a dysfunctional one,” she said.

And if it’s too much to believe that Fernandez won’t ultimately prove ruinous for debt investors, there’s always the hope -- however slim -- that someway, somehow Macri will win re-election. The first round of the vote is slated for Oct. 27, with a runoff coming four weeks later if necessary. In last Sunday’s dry run, Macri lost by 15 percentage points.

--With assistance from George Lei and Ben Bartenstein.

To contact the reporter on this story: Daniel Cancel in Sao Paulo at dcancel@bloomberg.net

To contact the editors responsible for this story: David Papadopoulos at papadopoulos@bloomberg.net, Brendan Walsh

©2019 Bloomberg L.P.