Burger and Taco Restaurant Bonds Suffer as America Locks Down

Burger and Taco Restaurant Bonds Suffer as America Locks Down

(Bloomberg) -- Bonds that securitize revenues from restaurants such as Wendy’s, Domino’s Pizza and Taco Bell have seen big declines as consumers shelter at home.

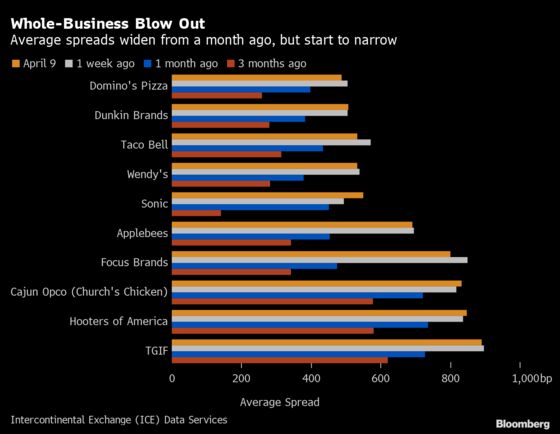

Restaurant chains that issue bonds backed by franchise fees, future royalties and other revenue-generating assets have seen them battered by the coronavirus pandemic. In many cases, average spreads on the so-called whole-business securitizations more than doubled, or even tripled, in secondary trading from three months ago. And more trouble may lie ahead as downgrades become increasingly likely.

“The negative impact on whole business securitizations from coronavirus will almost certainly be substantial, particularly for the restaurant sector,” S&P Global Ratings analysts said in a recent note. This is especially the case for those that rely on dine-in sales.

The restaurant industry was hurt as consumers began changing dining habits when the virus spread. While some have shifted to take-out or delivery only, the industry as a whole is losing revenue. More light should be shed on the matter as chains start reporting earnings in coming weeks.

Big Slip

In some cases, the spread widening was extreme. A BBB rated whole-business bond issued in 2018 from Sonic Capital LLC ballooned to 551 basis points over benchmarks by April 9 from an average of 141 basis points in January, according to ICE Data Services.

Meanwhile, three bonds in the BBB or BBB+ category from Focus Brands Inc., which owns recognizable mall chains such as Carvel Corp., Cinnabon International, and Moe’s Southwest Grill, traded at 801 basis points as of late last week from an average spread of 342 basis points in January, the ICE data show.

Bond yields have also increased. The average bond yield for the Focus Brands, for instance, was around 8.5% recently compared to roughly 5% in January, the data show.

These whole business ABS are a type of debt financing that lets companies issue bonds backed by assets like franchise fees, intellectual property, and licensing agreements. Through them, junk-rated, franchise-heavy companies with recognizable brands are able to issue bonds with investment-grade ratings, usually in the BBB tier, the lowest high-grade category.

This makes funding cheaper compared to costs in the corporate bond market. Whole-business ABS for other types of businesses that have been shuttered due to the pandemic, such as Planet Fitness Inc. gyms, also saw significant spread widening amid the chaos, and may face ratings stress.

Rating Companies Watch

While the risk premiums started to narrow slightly over the last week, credit ratings on some tranches face an uncertain future. Rating agencies say that the bonds may face downgrades, although this does not necessarily mean investors will take losses.

On April 13, Kroll Bond Rating Agency downgraded two slices of an already troubled deal from TGI Fridays Inc. to BB from BBB- after the coronavirus exacerbated ongoing issues with the company’s outlook. Last week, it put bonds from Planet Fitness and Massage Envy LLC on watch for possible downgrade.

On March 24, S&P warned nine slices from three whole business deals, Applebees/IHOP, TGI Fridays and Planet Fitness, could be downgraded, citing temporary closings of dine-in services at restaurants and the fitness clubs. The ratings company said consumers may remain hesitant to dine out even after social-distancing guidelines are made less stringent.

“We expect severe near-term sales declines” for both restaurants and fitness centers, S&P analysts said.

©2020 Bloomberg L.P.