What Comes After 2019’s Biggest Bond Deal? A Big Debt Diet

What Comes After 2019’s Biggest Bond Deal? A Big Debt Diet

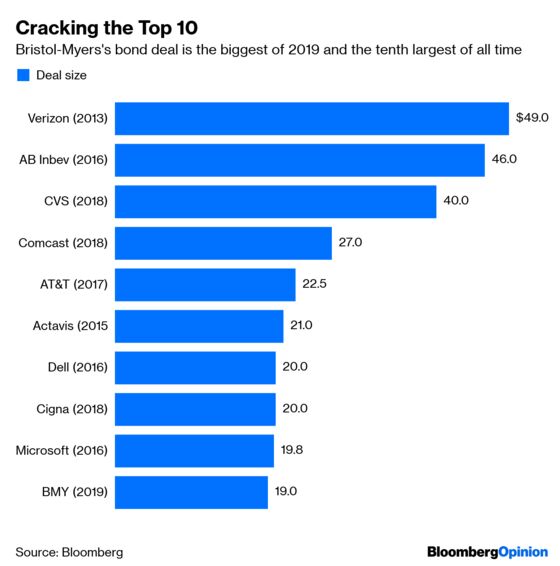

(Bloomberg Opinion) -- Bristol-Myers Squibb Co. easily completed the biggest U.S. corporate debt sale of 2019, issuing $19 billion of bonds at the cheaper end of its pricing scale. It’s part of the company’s plan to take on $32 billion of new debt, plus $20 billion of existing Celgene Inc. obligations, to eventually complete the largest biotechnology takeover in history.

Just don’t get used to how indebted Bristol-Myers is at the moment.

Over the next three years, the combined company should have “ample flexibility to delever rapidly,” Chief Executive Officer Giovanni Caforio said in early January. “Obviously, paying down the debt is the priority in the short term. But in the medium and in the long term, we will continue to be able to invest in science and innovation, and we're very comfortable with that.”

This lines up with the expectations of analysts at Moody’s Investors Service, who noted in a report last week that Bristol- Myers has a long history of conservative financial policies, keeping its ratio of debt to earnings before interest, taxes, depreciation and amortization at less than two. Still, the ratings company anticipates a one-level downgrade to A3, given the elevated leverage from the deal. S&P Global Ratings and Fitch Ratings are also reviewing their grades.

The idea of a “debt diet” and widespread deleveraging among U.S. companies caught on earlier this year, but with the S&P 500 Index having rebounded since then and the Federal Reserve holding off on further interest-rate increases, that sort of belt-tightening may seem less urgent. Just this week, my Bloomberg Opinion colleague Andrea Felsted noted that Anheuser-Busch InBev NV is at risk of getting distracted by shiny new deals, which could threaten its plans to pare down its $100 billion debt load.

Bristol-Myers's urgency might have something to do with what it's buying. Celgene gets over 60 percent of its sales from its best-selling blood cancer drug Revlimid, which could face generic competition sooner than expected if patent litigation doesn't go its way. In the meantime, though, it’s a cash cow.

Investors seem more confident that the combined Bristol-Celgene business will do better than just talk the talk, even after completing the 10th-largest bond deal ever. Its $4 billion of 10-year securities priced at a yield 105 basis points more than benchmark Treasuries, down from 120 basis points initially and right in line with the spread on the Bloomberg Barclays Investment-Grade Pharmaceuticals Index. Bristol-Myers’s 30-year bonds similarly tightened by 15 basis points.

Bloomberg Intelligence analysts Mike Holland and Madeleine Hart crunched the numbers and said they’d be cautious on fully buying in to the rating companies’ expectations for deleveraging. “Declines in branded and generic pricing growth, increasing pushback against high-cost therapies and rebates could hinder growth expectations and potentially affect optimistic cash-flow guidance,” they wrote Tuesday in a report. They expect the combined entity to have $48 billion in net debt, for 2.8 times leverage.

That’s perhaps not where management wants to be. But as my Bloomberg Opinion colleague Max Nisen has said, there are reasons Bristol-Myers is stepping out of its comfort zone and attempting an ambitious takeover. First, the price tag is relatively cheap from a valuation standpoint. Second, it could only really count on two drugs – blood thinner Eliquis and its immune-boosting cancer drug Opdivo – to grow on its own. It needs more options, even if Revlimid ends up facing generic competition sooner than expected.

That’s an R&D issue for down the road, as Caforio said. For however long the Revlimid exclusivity is still in play, the combined company will see ample cash pouring in. Which, if all goes according to plan, means the massive growth in debt will be short-lived.

--With assistance from Max Nisen.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2019 Bloomberg L.P.