Bristol-Celgene Deal Opposition Needs a Dose of Reality

Bristol-Celgene Deal Opposition Needs a Dose of Reality

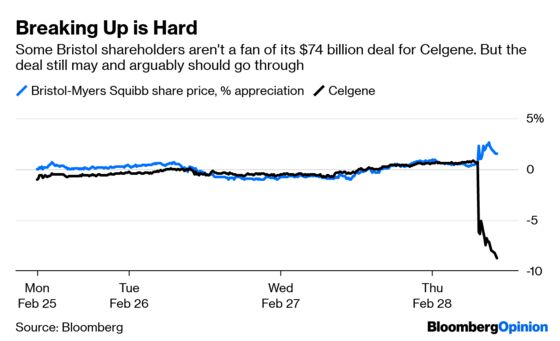

(Bloomberg Opinion) -- Whispers of discontent around Bristol-Myers Squibb Co.’s $74 billion acquisition of Celgene Corp. have turned into a roar.

It started Wednesday afternoon, when one of Bristol-Myers’s biggest shareholders came out against the deal. Wellington Management Co. put out a press release announcing that it’s not a fan, saying the takeover is too risky, undervalues Bristol-Myers’s shares, may be difficult to execute, and that unspecified “alternative paths” to value could be more attractive. Then on Thursday morning, activist investor Starboard Value – which has amassed a small stake in the company – said it, too, will oppose the deal. Its open letter to shareholders calls the transaction “poorly conceived and ill-advised.”

This is certainly a big wager for Bristol-Myers, but it may be investor’s best bet. The rationale is solid and from where I sit, it offers the potential to unlock more value for the drugmaker than any other alternative.

The principal danger of the deal is the prospect of earlier-than-expected generic competition for Celgene’s blockbuster blood-cancer treatment Revlimid. Analysts don’t expect sales of the drug, which are expected to pass $10 billion this year, to seriously decline until 2023. Earlier competition could cost Bristol-Myers billions.

But that’s a risk Bristol-Myers is clearly comfortable with, and it’s the reason the company was able to purchase Celgene at a discount. While the $74 billion price tag appears daunting, from a valuation standpoint the deal is among the cheapest big biotech transactions in recent history relative to trailing Ebitda, according to Bloomberg Intelligence.

The worst-case scenario – full-fledged generic entry next year – remains unlikely. Even a couple of years of unimpeded Revlimid sales would provide massive cash flow that would allow Bristol-Myers to rapidly pay down debt. The bargain Bristol is getting and the additional boost from Celgene’s broad and interesting pipeline of new drugs make the deal a risk worth taking.

The weakest part of the argument against the deal is the most crucial one, that a standalone Bristol-Myers would be better off and that someone might swoop in to acquire the company.

There’s a reason that Bristol-Myers is attempting this ambitious takeover. Its independent growth potential rests almost entirely on two drugs, blood thinner Eliquis and its immune-boosting cancer drug Opdivo. Eliquis is involved in patent litigation. Opdivo – which is even more crucial because Eliquis profits are split with Pfizer – has often failed to live up to high expectations. Poor decisions and mixed clinical trial results have ceded big chunks of the market to Merck & Co.’s rival Keytruda. And while Bristol-Myers has billions tied up in R&D designed to expand Opdivo’s use, the company’s recent track record doesn’t boost confidence that those efforts will pay off in an increasingly crowded market.

Starboard’s letter suggests that Bristol-Myers would be better off as a stand-alone company, but is missing a compelling argument for exactly why that’s the case. Its big idea for boosting the firm’s value is cost-cutting and margin improvement. That won’t help much if Opdivo’s struggles continue.

Starboard’s real hope is that someone will acquire Bristol-Myers. That’s unlikely to happen. Few firms have the financial firepower to pay an attractive premium on top of the drug giant’s $84 billion market value, and several of those market direct competitors to Opdivo or Eliquis. Hoping that a pharma giant shares an apparently very high opinion of Opdivo strikes me as wishful thinking.

The deal opponents seem to think that there are more attractive acquisitions than Celgene out there. Those won’t come cheap, though. The last two weeks saw Bristol-Myers’s biggest rival pay a premium of more than 300 percent on a biotech acquisition. If there’s another target or series of targets out there that would generate similar cash flow and secure as broad a collection of pipeline assets as Celgene, I’d love to hear about it.

If Wellington and Starboard truly want to derail this deal, they need to come out with a more compelling and detailed argument.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Max Nisen is a Bloomberg Opinion columnist covering biotech, pharma and health care. He previously wrote about management and corporate strategy for Quartz and Business Insider.

©2019 Bloomberg L.P.