Brexit Endgame Spurs Investors to Buckle Up for a Wild Ride

Brexit Endgame Spurs U.K. Investors to Buckle Up for a Wild Ride

(Bloomberg) -- In a year that’s featured a global pandemic and a tidal wave of liquidity from central banks, investors are bracing themselves for a risk they’ve ignored for most of 2020: Brexit.

The prospect of the U.K. and European Union reaching a trade agreement by an October deadline is looking less likely, with Britain saying this week it’s willing to walk away and break international law in the process. That risks the pound falling to a 35-year low, stocks that lag international peers, and bond yields turning negative for the first time amid bets on Bank of England interest-rate cuts, fund managers say.

“If we have a big selloff in risk assets, and a bad Brexit outcome, then there’s no reason the pound couldn’t fall back through the March lows,” said Mike Riddell, a portfolio manager at Allianz Global Investors. That would mean a 12% slump to around $1.14, the lowest since 1985.

The stalemate in discussions has already seen the pound suffer its longest losing streak since March when Covid-19 started to rip through the country, and has sent the yield on haven short-term bonds to record lows.

Until recently, the risks associated with failed trade talks had been in the background, overshadowed by the economic fallout of the coronavirus. The pound, which has acted as a market barometer to Brexit since the 2016 referendum, had been rallying along with other currencies in Group-of-10 nations against the U.S. dollar.

No-Deal Odds

Complacency around Brexit prompted Riddell to add to a short pound position in recent months and use sterling as a risk-off hedge, mainly against the U.S. dollar and the yen. NatWest Group Plc has upped the chances of no deal to 40%, a result it sees dragging sterling down to $1.20. Nomura International Plc sees the odds rising to 50% over time.

By contrast analysts in a Bloomberg survey expect only a mild drop in the currency to $1.30 by end-2020 and then gains next year. Economists from Goldman Sachs Group Inc., JPMorgan Chase & Co. and Morgan Stanley all still anticipate a deal on commerce will be in place for the end of December.

But with formal talks between the U.K. and EU resuming this week, the risks are back on investors’ radar. Prime Minister Boris Johnson signaled he would let the talks collapse if a deal isn’t made before mid-October rather than compromise. Officials have also drafted a law that risks undermining the negotiations, a move that Northern Ireland Minister Brandon Lewis conceded would break international law.

The EU’s chief Brexit negotiator Michel Barnier is “worried and disappointed.”

| Read More: |

|---|

|

The flare-up in trade tensions has increased the cost of hedging swings in sterling over three months to the highest level since April, while Johnson’s comments spurred the biggest jump for six months in options betting on a fall in the currency by December.

Value Trap

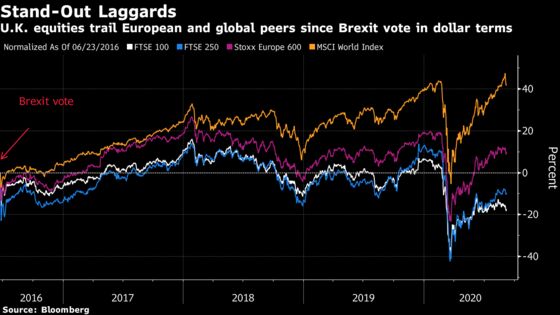

Brexit has been a drag on the nation’s equities, with the FTSE 100 falling to a record low against the MSCI World Index. While a slide in the pound may provide a boost for exporters, investors are more underweight on the U.K. than on any other country examined in a Bank of America fund survey for August.

“We see the U.K. as a value trap,” said Seema Shah, chief strategist at Principal Global Investors. “Valuations might be attractive but fundamentals are not.”

In addition to Brexit, the U.K. is suffering one of the biggest hits to growth in Europe from the pandemic, and must decide next month whether to keep supporting millions of furloughed workers or face a surge in unemployment.

That could mean more pain for U.K. Plc, which combined with concern over a painful transition from the EU, may further fuel demand for the safety of gilts. Benchmark yields have fallen near a record set during the pandemic shock in March, and the rate on two-year bonds dropped to an all-time low of minus 0.156%.

John Roe, head of multi-asset funds at Legal & General Investment Management, expects government bonds to rally if fears that trade talks will collapse drive up the possibility of U.K. interest rates going negative. No deal could lead the BOE to slash rates to minus 0.5%, said Ross Walker, NatWest’s co-head of global economics.

Money markets have already brought forward pricing on a BOE cut below zero to March, compared to September earlier this week. The potential for turmoil also raises the chances for more central bank bond buying.

“It’s worth remembering that the Bank of England’s forecasts are based on the U.K. reaching a full trade agreement with the EU,” said Daniela Russell, head of U.K. rates strategy for HSBC Holdings Plc, who sees 10-year yields falling to zero by the end of the year.

There’s a 40% chance yields could go below that to turn negative in the next year, said Jan von Gerich, a chief strategist at Nordea Bank Abp.

Bare Bones

A ‘bare-bones’ free trade deal would be enough to avoid such a scenario and lead Aberdeen Standard Investments to be underweight gilts, said Aaron Rock, an investment director.

And Citigroup Inc. foreign-exchange strategist Adam Pickett said the market hasn’t priced in the likelihood of the U.K. and the EU moving toward a last-minute agreement, targeting a pound climb back to $1.35.

Brexit fatigue could be one reason why markets are so far mostly positioned for a deal. Either way, fund managers will be glad to see the back of an issue that has forced them to work nights after late votes that flipped markets, defeated two prime ministers and divided the country.

“It has dragged on long enough,” said Rock at Aberdeen Standard. “It will be better for all concerned if we can move on.”

©2020 Bloomberg L.P.