Bonds to Fed: There’s Nothing Transient About Low Inflation

Bonds to Fed: There’s Nothing Transient About Low Inflation

(Bloomberg) -- As the Federal Reserve clings to hope that U.S. inflation will revive of its own accord, the bond market is practically screaming for intervention.

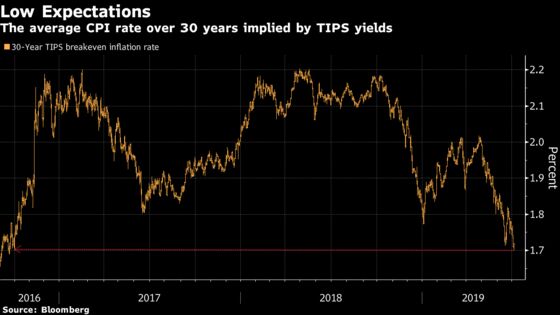

The Consumer Price Index rose 1.8% year-on-year in May, down from a 2018 peak of 2.9%. But the market’s view on where it’s headed is even more dire. As the 30-year Treasury bond’s yield slid below 2.50% Wednesday, its inflation-protected counterpart languished.

As a result, the gap between the two yields, representing the average expected CPI rate over the life of the securities, briefly collapsed to 1.7%, the lowest since September 2016.

While the Fed historically has viewed market-based inflation expectations cautiously, because of potential distortions arising from differences in relative liquidity and supply of inflation-protected bonds, the survey-based measures they’ve tended to put more stock in have plunged this year as well. The University of Michigan’s gauge of inflation expectations for the next five to 10 years declined to 2.2% in May, the lowest since the survey began.

It’s putting pressure on the central bank to consider cutting interest rates even with the unemployment rate at a near 50-year low of 3.6% in May and the S&P 500 at record highs. Inflation breakevens of various terms “remain near the lowest levels of the past two years, indicating the risk of more aggressive action from the Fed,” JPMorgan Chase & Co. rates strategists Jay Barry and Alex Roever wrote on July 1.

Cleveland Fed President Loretta Mester, making the case this week against a July interest-rate cut that futures market have fully priced in, said “declines in readings of longer-term inflation expectations’’ could help change her mind.

Mester said she’d also need to see “a few weak job reports’’ and other evidence of economic weakness. The June employment report to be released July 5 follows a surprise slowdown in job creation in May.

Another sign that investors are giving up waiting for the Fed to engineer a pick-up in inflation is the growing pile of Treasury inflation-protected securities on primary dealer balance sheets, said Guneet Dhingra, interest-rate strategist at Morgan Stanley.

Dealers’ net position in TIPS climbed to about $14 billion in the week ended June 19, Fed data show. It was under $10 billion as recently as April.

“That tells you that trading conditions are not very good in TIPS,’’ Dhingra said by phone. There’s “a confluence of factors that signal that inflation is not going to happen.”

Fed officials in their quarterly forecasts released in June lowered their forecast for 2019 inflation –- as measured by the deflator for personal consumption expenditures in the GDP accounts –- to 1.5% overall and 1.8% excluding food and energy. The CPI rate averages about 30 basis points higher than the PCE rate owing to differences in how they’re calculated.

It’s not just a U.S. problem. The European Central Bank also is contending with a slump in long-run inflation expectations, as measured by the five-year inflation swap rate five years forward, a benchmark.

To contact the reporter on this story: Liz Capo McCormick in New York at emccormick7@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Elizabeth Stanton, Mark Tannenbaum

©2019 Bloomberg L.P.