Bonds Hold Value in 60-40 World, So Long as You Adjust for Risk

Bonds Hold Value in 60-40 World, So Long as You Adjust for Risk

(Bloomberg) -- As Mark Twain might have put it, the demise of debt’s value within the long-favored 60-40 stock-bond diversified portfolios is greatly exaggerated -- when you adjust for risk.

That’s the view of Cornerstone Macro LLC after analyzing returns of portfolios with a 60-40 stock-bond mix over about the past decade under various market scenarios. Benson Durham, who served on the Federal Reserve Board and New York Fed in addition working at private firms including Brevan Howard Asset Management, was among authors of two reports that detailed the firm’s conclusions.

The recent synchronized selloff in equities and Treasuries triggered a fresh round of warnings to rethink the strategy, with Bank of America Corp. calling it “the end to 60/40” and Goldman Sachs Group Inc. warning that losses from such portfolios could swell. Underpinning the concern is an economy that’s facing mounting inflationary pressures after spending years warding off the threat of deflation.

“Sixty-forty is not dead in a risk-adjusted sense,” Durham said in a telephone interview. “All of the angst about 60-40 comes from the fact that debt term premiums are very low. But with bonds you can reduce your overall portfolio risk, so you get more bang for your buck.”

In Cornerston’s analysis to find if Treasuries are beneficial as a risk hedge within 60-40 stock-bond portfolios, they expanded normal linear beta -- a measure of the average return on an asset given return of the market -- to a quantile regression schema that gives a broader read of outcomes under different scenarios.

“The beta of the Capital Asset Pricing Model fame is of limited use for war-gaming market hypotheticals,” the team -- which also included Cornerstone’s co-founder Robert Perli -- wrote in their Oct. 4 note. The Capital Asset Pricing Model is a core theory in finance that codifies the role of risk in expected investment returns.

In both risk-on and risk-off scenarios, enhanced beta analysis “shows that U.S. Treasuries and other fixed income asset still add meaningfully to portfolio efficiency,” they wrote in the second note published Tuesday.

And while bond term premiums have been falling, Durham says equity premiums have been on the decline as well over recent years.

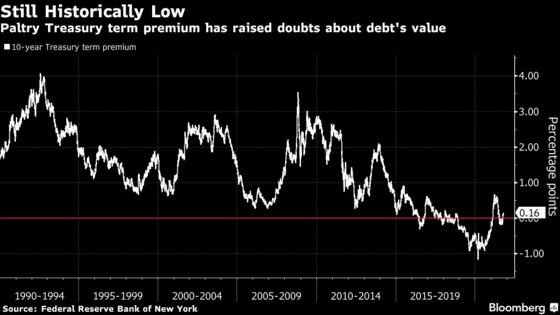

The jump in Treasury yields this year to about 1.55% has boosted 10-year term premium from deeply negative to about 16 basis points, according to a New York Fed model. Yet it remains well below its long-run average of about 150 basis points back through 1960.

Former Fed Chairman Ben S. Bernanke has noted that the Treasury term premium, or the compensation investors demand for the added risk of holding longer-term debt, is one of the three key factors that make up bond yields. The other two are the market’s expectations for interest-rate risk and inflation.

“There are really no perfect hedging alternatives to bonds, there is no tooth fairy,” Durham said. “And if you are just fixated on equity risk then obviously you buy equity puts, but that’s not the best way to hedge the portfolio because it’s expensive.”

In September, a portfolio of 60% stocks and 40% fixed-income securities posted the largest losses since March 2020, according to a Bloomberg model tracking the strategy. Treasuries lost 1% in September, and are on course for their largest annual losses since 2013, according to a Bloomberg index. The S&P 500 index lost 4.8%, the first monthly decline since January, leaving many investors wary about the strategy.

Durham pointed to the Sharpe Ratio, a common measure of risk-adjusted returns, as a better gauge to follow. A higher Sharpe Ratio indicates a better return-for-risk tradeoff.

“Tell me it’s dead in a Sharp Ratio world -- in a risk-adjusted world,” he said. “We’ve looked at all kinds of evidence in a risk-adjusted sense, and we can’t find proof of that.”

©2021 Bloomberg L.P.