Bond Bears Can’t Get Their Story Straight

Bond Bears Can’t Get Their Story Straight

(Bloomberg Opinion) -- It’s been a great 24 hours for bond bears. The benchmark 10-year Treasury yield surged Wednesday by the most since November 2016, busting through key levels and forcing even the most ardent advocates of “lower for longer” interest rates to do some soul-searching.

The problem for these bearish investors and strategists, though, is they just can’t seem to get their stories straight.

Some of them point to Federal Reserve Chairman Jerome Powell’s remarks that the fed funds rate “is a long way from neutral” as justification for pushing long-term yields higher. After all, if the central bank pushes its key rate above the nebulous neutral level for a while, therefore raising short-term note yields, then investors holding 10- and 30-year Treasuries need to be compensated more than they are now. But Powell made those comments in the late afternoon Wednesday, after yields had already climbed more than 10 basis points.

If not that, then it was probably the stellar back-to-back reports on the U.S. economy released earlier that day. That unexpectedly good news surely set the tone for the world’s biggest bond market. But as I wrote on Wednesday, these two figures largely just raise the stakes for Friday’s payrolls data. A number that beats the average estimate of 184,000 jobs added is almost considered a sure thing at this point (Bloomberg’s “whisper number” is 204,000). It would seem to take a blockbuster to jolt yields significantly higher.

Then there’s the Bill Gross theory: An increase in hedging costs for European and Japanese investors has priced them out of the Treasury market. That could certainly be part of it. But the low point for hedged U.S. yields was set last week, and funding pressures are easing slowly but surely.

A similar argument could be made that bond traders are finally seeing the effect of pensions stepping out of the market. The mid-September deadline for companies to contribute to their retirement funds at a favorable tax rate has long passed with a lot of commentary but not much reaction. The yield curve steepened, as some thought would happen once long-dated demand dried up. Jim Vogel at FTN Financial Capital Markets indeed said, “It is fair to call this a zero liquidity event for long Treasuries” and remarked that it looked like “a flash sale.”

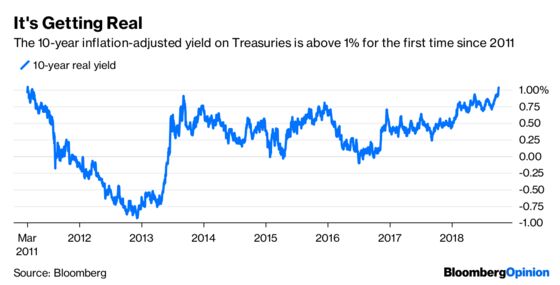

That’s not all that surprising, considering the break in key technical levels. In particular, DoubleLine Capital’s Jeffrey Gundlach and Citigroup Inc. strategists have cited 3.25 percent for the 30-year Treasury yield. Once past that mark, the selling intensified. Meanwhile, the market’s inflation expectations still aren’t as high as they were earlier this year, so the move has mostly been about economic growth prospects, as reflected by 10-year real yields rising above 1 percent for the first time since 2011.

The truth is, all of these probably played a role in what was an unexpectedly remarkable day in the $15.3 trillion market. The economic data led traders to offload Treasuries, which pushed yields above key levels. That encouraged more selling, and, without domestic pension funds or overseas investors to cushion the fall, momentum ruled the day. The fact that Powell made his comments late helped keep yields at their highs and encouraged follow-through during Asian trading hours. Bond traders, if they’re being honest, probably became too complacent with trading in the old range, and now they’re in a new one.

Yet that hasn’t stopped the prognostications from coming in fast and furious. From my Bloomberg News colleagues in Sydney, in a piece titled “Bond Bears Popping Champagne See Treasury Yields Even Higher”:

“In hindsight we wish we were even shorter on U.S. rates,” said Raymond Lee, a fund manager at Kapstream Capital Pty in Sydney.

But wait! Even those who expected yields to increase say the Treasury market may have gotten ahead of itself, according to others.

“The reaction in Treasury yields, particularly at the long end of the curve, seems outsized in nature compared with the reactions in Europe and the positive domestic data flow,” JPMorgan strategists including Jay Barry, who have been predicting higher yields in recent weeks, wrote in a client note.

And yet Sarasin & Partners Chief Investment Officer Guy Monson says he’s “afraid it just continues relentlessly and I am much happier with a 4 percent target than a 3.5 percent target” on 30-year yields.

So, which is it, bond bears? Is this the start of something bigger or just a knee-jerk repricing higher into a new trading range? The various pieced-together narratives make me tend to think it’s the latter, not to mention that relative-strength index analysis signals a consolidation ahead. But, like the Treasury market on Wednesday, I’m open to being surprised.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2018 Bloomberg L.P.