Bond Traders Bail on the Fed Too Soon

Bond Traders Bail on the Fed Too Soon

(Bloomberg Opinion) -- Bond traders are ready to pick a fight with the Federal Reserve. Maybe too ready.

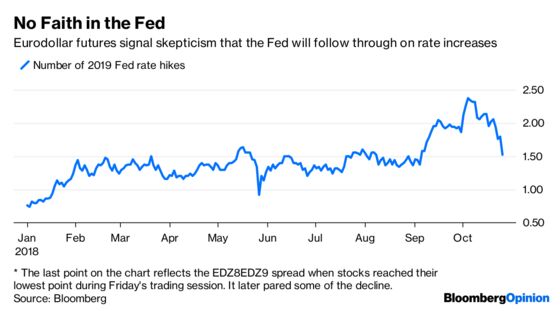

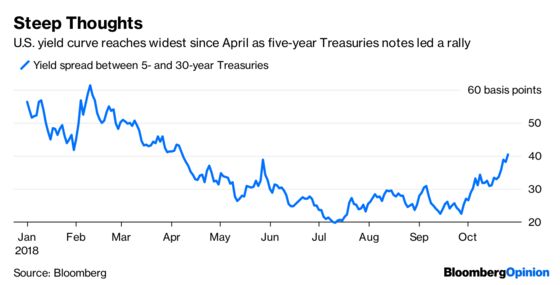

By just about any measure, they’ve begun to price out rate hikes in 2019 and beyond, betting in part that a stock-market rout that sent the S&P 500 toward a correction would cause central bankers to quit tightening policy. The eurodollar futures market at one point on Friday only expected about 1.5 moves next year, after baking in two increases just days earlier. Meanwhile, the Treasury yield curve from 5 to 30 years reached the widest since April, exhibiting a rare case of “bull steepening,” which is to say that shorter-term yields fell more than those at the long end. That’s because traders were altering their outlook for how high the fed funds rate may climb in the coming years. The five-year yield closed the week below 3 percent for the first time since September. Fed officials forecast their benchmark short-term rate will be above that from late 2019 through at least 2021.

Obviously, stocks matter to the world’s biggest bond market, so when the S&P 500 tumbles more than 10 percent from the record it set just last month, investors are going to get nervous and flock to the usual havens. Still, this seems like an overreaction from traders who have long been waiting for any sign that the Fed’s rate increases had caused something to “break” in the financial markets or the economy. Certainty, there’s been little indication that the latter is at risk — gross domestic product climbed a better-than-expected 3.5 percent in the third quarter on strong consumer and business spending. The U.S. employment report this week will probably show that American businesses added 193,000 workers in October, in line with the average since the start of 2017.

It’s not clear what rationale bond traders have for expecting the Fed to slow down, other than post-crisis precedent from Janet Yellen. Just before the equity markets opened on Friday, Cleveland Fed President Loretta Mester, a voter on the Federal Open Markets Committee this year, said that recent market volatility hadn’t changed her outlook and that investors were naturally reassessing risks. She’s among those officials who see the long-run fed funds rate at 3 percent, from a range of 2 percent to 2.25 percent now.

The previous day, in his first public speech since joining the central bank, Fed Vice Chair Richard Clarida echoed Chairman Jerome Powell in saying that “monetary policy remains accommodative.” That means more rate increases as long as the data support them. Though, as my Bloomberg Opinion colleague Dan Moss wrote, he might have also been trying to subtly walk back Powell’s “long way from neutral” construction, which probably contributed to the recent market fluctuations.

U.S. markets are trying to find a healthy equilibrium, particularly at a time when corporate earnings aren’t the pillar of strength they once were. For stocks, it’s being called a “repricing,” leaving the S&P 500 cheaper than at any time since Donald Trump was elected president. For the $15.3 trillion Treasury market, it opens up the risk of traders being caught off-sides if the volatility abates, as it has time and again this year. The five-year yield tumbled 18 basis points on May 29, only to increase by 21 basis points in the following four sessions. It dropped 15 basis points on Feb. 5, yet was back where it started in a week and a half.

Now, as Bloomberg News’s market reporters have noted, this bout of volatility is a bit different because it’s just as persistent as it is furious. That could make it trickier for Fed officials to brush it off. Plus, unlike in past episodes, Goldman Sachs Group Inc.’s index of U.S. financial conditions is near the tightest since March 2017. Tom Lee, head of research at Fundstrat Global Advisors, advised buying the dip in stocks because it tightened financial conditions by just as much as a quarter-point rate hike.

Lee also added that the “Fed ultimately has the market’s back.” Again, that harkens back to an old way of thinking about this Fed. Sure, Yellen cut back on rate increases when stocks slid 12 percent in August 2015 and 13 percent in January 2016. But, as Bank of America Corp. Global Economist Ethan Harris wrote Friday in a report, “We would not take too much solace from this experience. The economy and the Fed were in a very different place.” Specifically, the Fed was much less confident about how the market would handle rate hikes, whether the economy had recovered from the recession, and if officials could achieve their inflation target. None of those things is much of a concern anymore.

Lurking in the background of all this is the unusual political pressure on the Fed from Trump, who has lamented the central bank’s “loco” pace of interest-rate increases. To many observers, that will only strengthen policy makers’ resolve, rather than weaken it, so they don’t risk even the appearance of veering into the political arena. Obviously they’ll pause if economic data that affect their dual mandate warrant it — but propping up the stock market isn’t part of their purview. That’s something bond traders seem to have forgotten.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2018 Bloomberg L.P.