Bond Traders Are Skeptical of Bostic’s Steeper Yield-Curve Call

Bond Traders Are Skeptical of Bostic’s Steeper Yield-Curve Call

(Bloomberg) -- Federal Reserve Bank of Atlanta boss Raphael Bostic has been busy talking about the Treasury yield curve again. But rates investors aren’t yet convinced that it will rebound as he predicts following its recent turbo-charged flattening.

Bostic was among the loudest central-bank voices talking about the gap between the rates on different Treasury maturities around two years ago, when the curve was hurtling toward a so-called inversion -- when long-end rates drop below near-term ones in a distortion that’s often seen as a harbinger of recession. This time around he says that as the economy builds, he’s “confident that that the yield curve will steepen once again and get us back to more normal conditions” -- but, for now, the market appears skeptical.

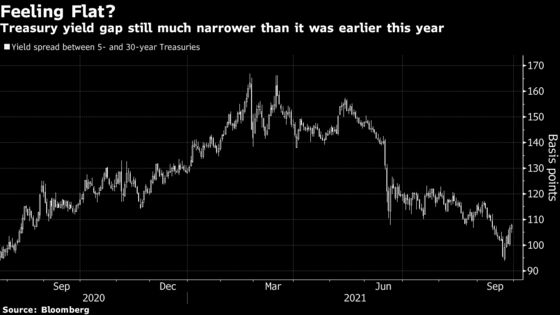

The widely-watched differential between 5- and 30-year yields plunged below 100 basis points in the wake of last week’s Fed decision, and while it has recovered to around 108 basis points, that’s still a far cry from its highs earlier this year. Fed officials like Bostic have often shown interest in the shape of the curve for what it says about the trajectory of economic growth; a steeper curve tends to coincide with stronger expansion prospects, so it’s perhaps unsurprising that Fed officials with an eye on normalizing policy would be of that view.

Long-end rates have certainly climbed in recent days, with the 30-year yield up more than a quarter of a percentage point since the middle of last week. Yet even amid that shift, positioning data suggests that some investors are holding on to long Treasury positions. And price action indicates traders are coming in to buy Treasuries when yields jump to attractive levels, potentially putting a lid on such moves.

And perhaps more crucially, the moves at the front end of the curve have been even more aggressive. The past week has seen money-market traders amp up their bets on the pace of Fed tightening, pulling forward their expectations for the first quarter-point rate hike by the central bank to late 2022, having earlier placed it in 2023.

That’s left the curve, by and large, in limbo. The market has shown almost no sign of the kind of telltale trades in futures or options that would suggest traders are once again taking on either steepening positions or flattening bets.

The steepening trade has been very popular in recent years, but a number of Wall Street banks have called time on it in the past few months in anticipation of a Fed hiking cycle, and there is little indication of that changing just yet.

Jonathan Cohn, a strategist at Credit Suisse Group AG, says the curve is set to tread water through the end of the year -- even though he just boosted his predictions for yields. He forecasts 5-year yields will rise to around 1.25% by year-end and that 30-year rates will reach 2.30%. That outcome would leave the gap between those maturities close to where it is right now.

©2021 Bloomberg L.P.