The Bond Market Has Its Most Crucial Repricing Yet

The Bond Market Has Its Most Crucial Repricing Yet

(Bloomberg Opinion) -- The most resilient part of the $15.4 trillion U.S. Treasury market finally succumbed to the risk-off pressure circling the globe. It’s the strongest signal yet that bond traders are confident the Federal Reserve is going to stop raising interest rates soon.

Two-year Treasury yields tumbled as much as 10 basis points on Thursday, the biggest intraday drop since May and one of the largest since the Fed began its quarterly tightening pace in December 2016. At its low of 2.69 percent, the difference between that yield and the 2.25 percent upper bound of the central bank’s benchmark rate was the narrowest since the start of the year. That’s another way of seeing what Bloomberg News’s Liz Capo McCormick noted on Thursday: that some traders no longer believe the Fed will raise interest rates at all next year, and they’re even starting to doubt a move this month, which has long been considered a sure thing.

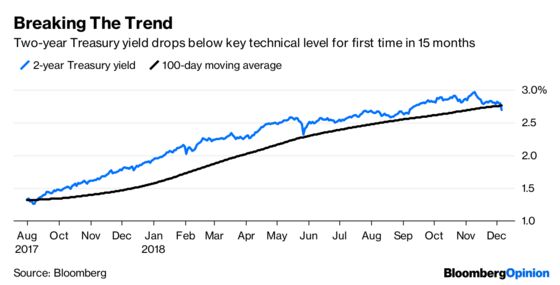

This capitulation at the short end is arguably the most important development yet this week in the world’s biggest bond market — even more notable than the first curve inversion in a decade. For the most part, two-year yields have steadily marched higher in 2018, save for a couple of blips in February and May as stocks whipsawed. Even during those episodes, though, the yield never broke through its 100-day moving average — an important technical indicator. This time, it easily cruised past that level (2.7575 percent) for the first time since September 2017. That was when, among other things, Kim Jong Un’s regime in North Korea spooked markets by conducting its most powerful nuclear test.

Of course, two-year Treasuries are among the most traditional flight-to-quality assets, so the rally makes sense given equity markets are slumping globally. But to some, this move feels different. “The ‘pain’ out there is abundant,” Tom di Galoma, managing director of government trading and strategy at Seaport Global Holdings, wrote in a note. Bloomberg News’s Edward Bolingbroke — who isn’t one for hyperbole — called Thursday “a dramatic day across the front-end of the U.S. rates curve.”

The move also serves to stave off a more full-blown inversion of the U.S. yield curve, at least for now. Ten-year Treasuries couldn’t keep pace with the front-end rally, leaving the spread between 2- and 10-year maturities at 12 basis points, compared with less than 10 earlier this week. That could be interpreted as bond traders expecting the Fed to ease up on interest-rate increases sooner than expected, which may prevent a “policy error” of tightening too quickly.

The Fed’s “dot plot” currently shows the median expectation for the longer-run neutral rate is 3 percent. As recently as a week ago, Treasury yields across the curve converged around that level, and the market felt balanced. The latest swings suggest that’s probably too high, and expectations seem to have readjusted closer to 2.75 percent. Again, that’s entirely reasonable given that Fed Chairman Jerome Powell adjusted his language to say interest rates now are “just below” neutral. Atlanta Fed President Raphael Bostic chimed in on Thursday, saying rates are “within shouting distance of neutral.”

The repricing of interest-rate increases this week has been “perfectly rational,” Jabaz Mathai at Citigroup Inc. wrote Thursday in a note. He had previously recommended buying 10-year Treasuries but now suggests taking profits on that trade, given that the Fed appears willing to provide support to equity prices.

“Treasuries have rallied to levels where we think it is prudent to take profits on long duration trades (especially for investors who went long at 3.25%) and to wait for better levels to re-initiate longs.

Any bounce in equity markets will lead to a sell-off in rates, as the Fed put goes out of the money. We expect this feedback loop to be a persistent feature of the equity-Treasury market relationship in 2019.”

Indeed, the unusual trend of bonds and stocks both losing money seems to be a thing of the past as markets enter a more volatile period. Some investors expected a tug of war between the two asset classes earlier this year, only to see stocks and Treasury yields both test multiyear highs in the second half of 2018.

That might finally be changing, if technical levels are to be believed. In addition to the two-year yield’s breakthrough of its 100-day moving average, the 10-year yield crashed through its 200-day moving average this week for the first time in about 13 months. That’s probably because large speculators who have bet against the market throughout 2018 were finally flushed out of their positions.

Say what you will about the first inversion of the U.S. yield curve and whether it’s just a quirk or a signal of something more significant to come. But the sharply lower yields across all maturities, and especially the short end, are sending an unambiguous message to the Fed: Slow down now before you make a mistake.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2018 Bloomberg L.P.