Swedish Bond Market Dysfunction Draws Central Bank Criticism

Swedish Bond Market Dysfunction Draws Central Bank Criticism

(Bloomberg) -- Sweden’s corporate debt market isn’t providing investors with the price information they need, according to the country’s central bank.

Things came to a head two months ago, when 35 credit funds shut their doors on investors trying to flee at the height of the Covid-19 crisis. Money has since flowed back into the asset class and spreads have begun to recover. But a root cause of the selloff hasn’t gone away.

Cecilia Skingsley, first deputy governor of the Riksbank, says the basic problem is that Sweden’s corporate bond market is “characterized by low transparency in pricing.” And it’s gotten “even worse since the crisis hit,” she said in an interview.

It’s the latest warning about a market that has its stakeholders increasingly worried. Meanwhile, the Riksbank has hired advisers from BlackRock to help expand its bond purchases to target corporate debt. But the lack of price transparency means “we need to do a lot of analysis,” Skingsley said.

Jonas Osterlund, head of credit sales at SEB AB, says “all market participants still have things to do” to ensure bond valuations are fair in Sweden. “It’s an issue that became very obvious during a crisis like this one.”

Osterlund says part of the problem is that there’s no one place investors can go to get a definitive price. In neighboring Norway, all credit funds turn to a company called Nordic Bond Pricing. But in Sweden, Osterlund says the situation is “a bit strange.” And with funds using different sources, valuations for individual ISIN codes suddenly differ across the market.

Those price anomalies are exacerbated when volatility hits. “When there is distress in the market there can be huge differences,” he said.

In March, managers such as Spiltan Fonder AB had to temporarily shutter their funds as it became “practically impossible” to value the assets in their portfolios.

Valuation Leeway

Adding to the problem is a lack of public credit ratings in Sweden, which hasn’t gone unnoticed by the central bank.

“I’m critical of the fact that a high portion of issuers don’t have something as basic as a credit rating,” Skingsley said.

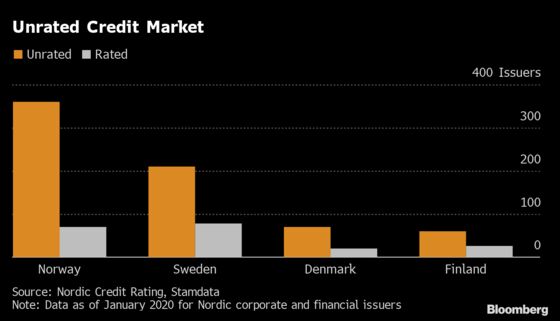

In contrast to the U.S. and Europe, corporate bonds in Sweden are still largely unrated with only 79 rated issuers out of a population of 290 corporate and financial issuers, according to year-end data compiled by Stamdata AS.

That gives fund managers in Sweden plenty of leeway when it comes to assigning values to their holdings. It’s one of the issues the Riksbank will need to deal with as it draws on BlackRock to guide it through purchases.

Historically, it has been too costly and time consuming for small and mid-sized issuers in the region to obtain a credit rating, according to Gustav Liedgren, chief executive at Nordic Credit Rating. “If more of these issuers get rated it will improve the bond market’s robustness,” he said.

“If the Riksbank bought unrated bonds we would be the first central bank to do so,” Skingsley said. “I’m not saying we can’t do it, but it would mean significant preparatory work and time isn’t endless.”

| Read More: |

|---|

|

©2020 Bloomberg L.P.