Bond Market Attack on Central Banks Leaves No Room for ECB Error

Bond Market Assault on Central Banks Leaves No Room for Error

(Bloomberg) -- Markets are turning up the pressure dial on central banks to boost policy easing.

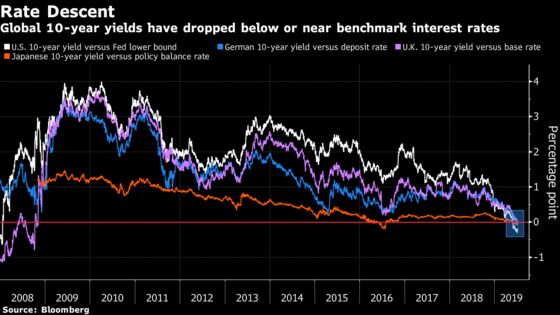

Benchmark bond yields have in unison dived below or close to key interest rates in the world’s biggest economies. While this has happened before in the U.S., it’s never been seen before in the euro area. That show investors expect the Federal Reserve and European Central Bank to deliver stimulus soon.

With markets now primed for rate cuts, if central banks fail to meet expectations they would lose credibility in the eyes of investors, unleashing volatility and spurring a flight to safety across bonds, currencies and stocks. That would raise the stakes for central banks searching for ways to ward off the next financial crisis.

“There becomes a tipping point where not satisfying the market is dangerous,” said Luke Hickmore, a money manager at Aberdeen Standard Investments. “Not satisfying this change in mood when we are at a sensitive point for economies, with the risk of tipping over to recession, would hit hard.”

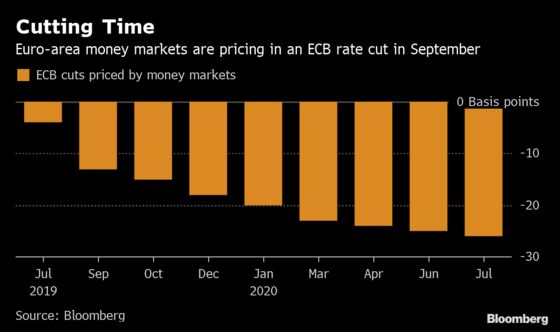

The first flashpoint could come today, as money markets have priced in a 40% chance that the ECB will lower borrowing costs at its policy meeting. Most strategists expect ECB President Mario Draghi to at least lay the groundwork for more stimulus in September, including quantitative easing.

Read More:

|

Traders are factoring in nearly 20 basis points of rate cuts for this year, while the aggressiveness of the bond rally after disappointing German manufacturing data Wednesday forced bund futures trading to be temporarily halted. Bund yields fell to minus 0.39% Thursday, approaching the ECB’s minus 0.4% deposit rate after breaking below it this month.

At the least, market pressure is pushing officials to make a decision about whether they need to start easing sooner rather than later, amid worries over their currencies appreciating against those of other countries who are taking action. The Fed is expected to cut interest rates by 25 basis points next week and follow that up with more this year.

“Central banks are about to go from one extraordinary easing cycle into the next extraordinary easing cycle,” said Richard McGuire, head of rates strategy at Rabobank. “There’s been no tightening cycle in between because frankly, there is no cycle. This just takes us one step closer to a de facto nationalization of financial markets.”

In the euro area, inflation expectations lingering near record lows show that markets have little faith in the ECB ever meeting its goal, leading to fears of “Japanification” -- a world of permanently low growth and monetary easing. Christine Lagarde, who is set to take over from Draghi at the helm of the ECB, is widely expected to lobby governments to do more of the heavy lifting through spending.

Germany’s 10-year yields have also fallen below Japan’s. Goldman Sachs Group Inc. is among those thinking bund yields will slide even further, predicting minus 0.55%. With these levels signaling a lack of faith in the ECB’s efforts, officials have begun studying a potential revamp of its inflation goal, which could embolden them to pursue stimulus for longer.

“Maybe we should be talking about the Germanification of Japan, given where the relative yields are,” said John Taylor, a money manager at AllianceBernstein Holding LP. “If only the ECB had exited QE when growth was above 2%, they might have given themselves a little bit more flexibility.”

Dovish Tilts

In the U.K., even the most hawkish Bank of England officials are beginning to dial down the prospects that the next move in interest rates could be higher. Markets are now pricing in BOE rate cuts amid heightened fears that Britain is facing a potentially damaging no-deal exit from the European Union.

For the Fed, its pivot from a cycle of rate hikes to an expected reversal of those comes as the yield gap between three-month bills and 10-year Treasuries remains below zero, a widely-touted signifier of recession. With the Fed meeting coming up, the ECB may be unwise to use the option of bringing back QE just yet, according to Peter Chatwell, head of European rates strategy at Mizuho Bank Ltd.

“Not only would it use precious firepower, but it would probably incentivize the Fed to cut more aggressively next week, taking the currency war a notch higher in intensity,” Chatwell said.

To contact the reporter on this story: John Ainger in London at jainger@bloomberg.net

To contact the editors responsible for this story: Ven Ram at vram1@bloomberg.net, Neil Chatterjee, Scott Hamilton

©2019 Bloomberg L.P.