Bond Investors Are Bracing for a Bubble and Being Smart About It

Bond Investors Are Bracing for a Bubble And Being Smart About It

(Bloomberg) -- The fear of a global bond bubble bursting has the market on edge, but it takes a brave investor to bet against a rally that smashed so many records.

Instead, those seeking to guard against a sell-off are favoring less direct ways -- shifting into shorter-dated debt that’s less vulnerable to price swings, buying bearish options and boosting holdings of high-quality credit. Such trades represent a wager that the global economic pessimism, which has been driving the fixed-income surge, is somewhat exaggerated and that inflation still has a chance of picking up.

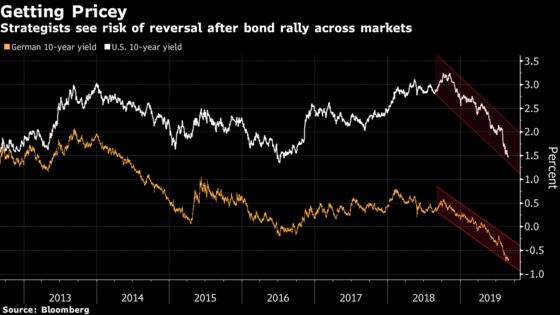

This year’s unprecedented rally has pushed yields on more than $17 trillion of global debt below zero, with Germany’s entire curve now negative. While that means buyers are guaranteed to make a loss if they hold the securities to maturity, many are still piling in on the hope of price gains, prompting some investors to warn that a bond bubble may be in the making.

“There is a significant risk of a sell-off at the moment,” said Luke Hickmore, a money manager at Aberdeen Standard Investments. “A big sell-off would occur if the big global risks -- the trade war or Brexit -- ease off or central banks underwhelm with their policy response.”

Yields have risen as a number of risks -- from Brexit to Italian and Hong Kong politics -- all eased at the same time, while traders pare back bets on fresh bond-buying from the European Central Bank next week.

Thirty-year German yields have rebounded back to 0% from a record low of -0.31% reached in mid-August, with the premium over five-year bonds at its highest in over a month. Similar long-end rates in the U.S. have surged back above 2% from an all-time low of 1.90% last week.

The concern that the bond rally may lose steam is also being fueled by the prospect of governments stepping up fiscal spending -- a move that would entail increased debt supply that would weigh on fixed-income prices. Germany is said to be considering boosting budget support to its struggling economy.

“We know not the day or the hour, but risks for bonds are mounting and it is time to cover longs,” Societe Generale SA strategists led by Subadra Rajappa wrote in a note. “Bonds are pricing in significant uncertainty premium and policy accommodation, and are vulnerable to a sell-off.”

Investors may also be looking to lock in profits after investment-grade bonds have returned nearly 8% this year, according to Bloomberg Barclays Indices.

Option Strategies

Bond bears have gotten badly burnt in recent years, with even heavy hitters such as Bill Gross and Ray Dalio getting calls wrong. So, many who seek to bet against the rally are turning to options -- positions that will pay off on debt declines, with the maximum risk limited to losing the premium paid.

Investec Asset Management took profit on long positions in Treasuries, and has bought options to sell the yen as a proxy for bearish bets on Japanese debt.

“The simple view is bonds are undoubtedly expensive,” said Russell Silberston, a money manager at the fund. “We have taken out some yen put options in small size as these are highly correlated with yields.”

Resco Asset Management is also using derivatives to position for bond declines, and in the U.S. the firm has bought put options in five-year Treasuries with an October expiry. While the premium was high due to a jump in market volatility, a bearish position is worth it given how low yields are and the large amount of monetary easing already priced in, according to money manager David Ric.

“Low yield doesn’t mean low risk,” Ric said. “The massive bazooka” of monetary stimulus “is probably already priced,” he said.

Cutting Duration

Another way to insulate a bond portfolio is to shorten its duration, a gauge of how sensitive holdings are to interest rates, by increasing allocations into shorter-dated securities.

While many money managers taken duration to extremes -- snapping up Austria’s 100-year bond and pushing the premium on longer-dated debt to a 58-year low -- some are going the other way.

JPMorgan Asset Management saw increased inflows into its European ultra-short duration fixed-income fund, with 15% of its assets coming in this year alone. TwentyFour Asset Management’s Chris Bowie is paring maturities and sees short-dated U.K. debt as offering better protection against volatility.

“The blind hunt for yield will continue but pockets of investors are starting to question when the music stops, what am I actually invested in, is this risk profile appropriate for me?” said Jemma Clee, head of investment specialists for EMEA at JPMorgan Asset. “It’s a risk-off trade for a fixed-income investor.”

Bonds are the most expensive since 1999 and that raises the chances of a rapid sell-off, TwentyFour Asset’s Bowie wrote in a note citing a duration-yield model. In addition to cutting duration, he is boosting the credit quality of his portfolio to minimize risk.

“At this very late stage of the cycle, we believe now is not the time to be reaching for yield by increasing credit risk, and consequently prefer to keep our credit spread duration low and our credit quality high,” Bowie said. “Corrections in risk assets can be swift and painful.”

--With assistance from Tanvir Sandhu.

To contact the reporters on this story: John Ainger in London at jainger@bloomberg.net;Charlotte Ryan in London at cryan147@bloomberg.net

To contact the editors responsible for this story: Ven Ram at vram1@bloomberg.net, Anil Varma, William Shaw

©2019 Bloomberg L.P.