Bond Guru Dan Fuss’s Inflation Alert Points to Market Challenges

Bond Guru Dan Fuss’s Inflation Alert Points to Market Challenges

(Bloomberg) -- Famed bond investor Dan Fuss recollects how spiking inflation in the 1940s and 1950s led to a sevenfold jump in the value of his family home. For him, a key trigger of that bout of price pressure is evident now.

The precedent is the way the Federal Reserve and Department of the Treasury are prioritizing cheap debt-financing costs to fund huge spending, the difference being the money is paying for once-in-a-generation pandemic relief rather than a war effort.

“Interest rates are very very low, much lower than in my lifetime, and I was born into the Depression,” Fuss, vice chairman of Loomis Sayles & Co., said in an interview. Bond investors should keep their powder dry given the risk of faster inflation, the 87-year-old said, adding “there’s no outstanding value in the fixed income markets.”

For now, markets are pointing to moderate price gains as the world recovers from the health crisis. One key gauge signals expectations for an average rate of about 2.2% in the U.S. over the next decade. The challenge for investors is protecting portfolios if inflation becomes a bigger problem -- possibly heralding monetary tightening -- given that many view bonds and stocks as already richly valued.

While Loomis Sayles’s Fuss has previously voiced concern about inflation risk, more investors and strategists are joining him in contemplating the possibility of higher price pressures.

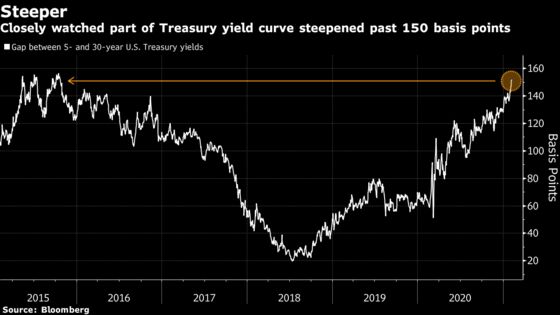

A closely watched segment of the Treasuries yield curve has steepened to levels last seen in 2015, driven in part by President Joe Biden’s planned $1.9 trillion pandemic relief package. Some commentators, such as former Treasury Secretary Larry Summers, have raised questions about the size of the package because of the risk of much faster inflation.

Fuss said the comparison with postwar markets is imperfect but still relevant. Stocks performed reasonably well in the 1940s before accelerating in the following decade. Yields on the most highly-rated corporate credit held steady after World War II but rose as much as 2 percentage points during the 1950s to 4.58%

©2021 Bloomberg L.P.