BOJ’s Dilemma Spurs Speculation on Reverse ‘Operation Twist’

BOJ’s Dilemma Stokes Speculation on a Reverse ‘Operation Twist’

(Bloomberg) -- Japan’s central bank, long a pioneer in pushing the envelope of monetary policy in its campaign to stimulate the economy, may yet add to its record of innovation.

The Bank of Japan’s current dilemma is that while its peers have eased policy -- or are set to do so soon -- it has refrained from additional action. That leaves Japan’s exchange rate vulnerable if other central banks’ moves drive down their currencies. A stronger yen would hurt Japanese exporter earnings and the stock market, and put downward pressure on prices.

Yet taking Japanese interest rates deeper into negative territory, or stepping up asset purchases, risks doing yet more damage to investment returns. Governor Haruhiko Kuroda himself issued a warning on that front last week.

This Gordian Knot-type conundrum has revived speculation about a so-called reverse operation twist. That’s where the central bank moves to cut short-term rates while supporting longer-term ones. In theory, it could head off yen appreciation, support institutional investors’ returns and boost bank stocks.

“Aggressive tapering alone would be viewed as major tightening,” if the BOJ just focused on cutting back its bond purchases, Yujiro Goto, head of foreign-exchange strategy at Nomura Holdings Inc. in Tokyo, wrote in a note Tuesday. That approach would risk a strengthening of the yen, he added.

That’s why “a reverse twist operation-type policy combination would be necessary,” Goto wrote.

In the original Operation Twist in the 1960s, U.S. policy makers attempted to shrink the gap between short and long-term yields. The Federal Reserve mounted another such maneuver in 2011.

BOJ watchers also floated the idea of a reverse twist back in 2016, when -- like now -- there were global economic headwinds and trenchant declines in longer-dated bond yields were stoking angst among Japanese investors.

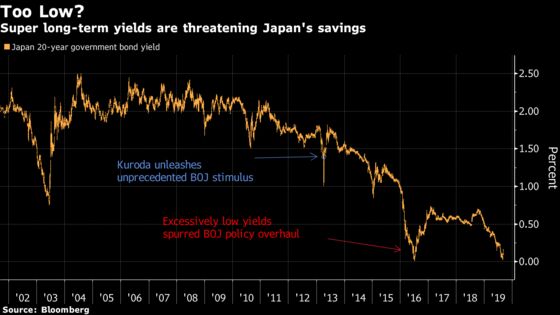

Kuroda said in an interview with the Nikkei newspaper last week that yields on 20-year and 30-year Japanese government bonds have “fallen a bit too far” and that returns for life insurers and pension funds have fallen significantly -- negatively affecting consumer sentiment.

Three years ago, instead of a reverse twist, the BOJ adopted a new framework, twinning the negative short-term interest rate it had adopted earlier in 2016 with a target for 10-year bond yields of around zero.

Trouble is the actual yield is now well below zero, at -0.20% in Tokyo trading late Wednesday. Japanese banks, insurers and pension funds have been piling into foreign securities in their hunt for returns, potentially stockpiling risk as they do so. Regulators have had to tighten scrutiny.

Given that the impetus for lower long term yields lately has been global, not local, there may not be much the BOJ can do to limit damage to savers if it steps up stimulus via interest rates. (There’s always other moves, like expanding exchange-traded fund purchases.)

While the BOJ could trim its bond buying to prevent any “violent” move in longer-dated yields, “it would not be surprising should Japan end up joining Switzerland and Germany in having its entire yield curve” below zero, Morgan Stanley analysts including Takeshi Yamaguchi wrote in a note last month.

To contact the reporter on this story: Christopher Anstey in Tokyo at canstey@bloomberg.net

To contact the editors responsible for this story: Malcolm Scott at mscott23@bloomberg.net, Paul Jackson

©2019 Bloomberg L.P.