BOE Bemoans Liquidity Problems Analysts Say It Helped Create

BOE Bemoans Liquidity Problems Analysts Say It Helped Create

(Bloomberg) -- Investors are blaming the Bank of England for creating the very conditions it blamed for its communication flip-flop this week.

“A deterioration in liquidity conditions meant that it had become more difficult to infer a central path for policy expectations,” Monetary Policy Committee members said in minutes from the decision on Thursday. But that illiquidity was a result of uncertainty over the BOE’s own policy position, analysts said.

The central bank’s decision to keep interest rates on hold sent gilt yields and the pound sharply lower. It came just two weeks after Governor Andrew Bailey said we “have to act” on quickening inflation, cementing investors positioning for a rate hike.

“The cause of the market illiquidity was poor communication, which meant that they could not accurately infer market expectations,” said Peter Chatwell, head of multi-asset strategy at Mizuho International Plc.

“I would suggest a thorough review of the communications policy is overdue and is something that would benefit the U.K. public,” he said. “After all, it is the tax payer and the U.K. real economy more generally, which suffers from the excess volatility that these difficulties have caused.”

Market prices are prone to liquidity issues and uncertainty, which means they aren’t necessarily an accurate gauge of investor expectations. The difference this time was the scale of the distortions, which forced the MPC’s unusual complaint.

The minutes said that interpreting U.K. inflation markets was “not straightforward” because liability hedging by pension funds causes shifts beyond price-change expectations. Their comments reflect the difficulties extracting information from U.K. markets that have experienced value-at-risk shocks, forcing the liquidation of positions.

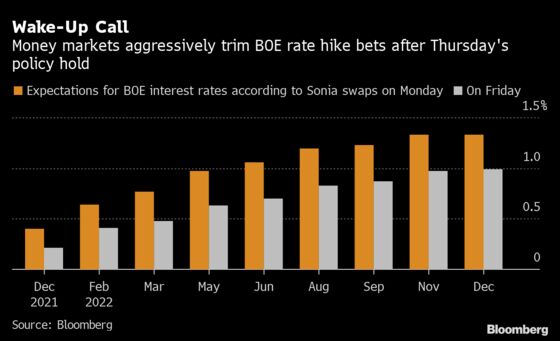

Before the decision, money markets had priced in as much as 130 basis points of tightening by the end of 2022, which would raise the Bank Rate to almost 1.5% from 0.1% currently. Inflation markets had also surged, with 10-year breakevens hitting their highest since 1996 and inflation swap rates pushed higher.

“If, as now appears the case, they thought too much was being priced for Bank Rate they had ample opportunity to deal with that in the run-up to the meeting,” said Cathal Kennedy, European economist at RBC in London. “The lack of guidance on how fast or how far they would go once they began to tighten had caused the market to price in too much.”

©2021 Bloomberg L.P.