Blockchain's Appeal Limited for Retail Banks, McKinsey Says

Blockchain's Appeal Is Limited for Retail Banks, McKinsey Says

(Bloomberg) -- Retail banks have been slower to embrace blockchain technology and face greater challenges in reaping its potential benefits than their more adventurous counterparts in the investment-banking world, according to new research from McKinsey & Co.

Headwinds for retail lenders to adopt a shared system of distributed computer ledgers to manage day-to-day activities include a tougher regulatory environment for consumer finance and the success of existing alternative payment services such as Zelle, Matt Higginson, one of the authors of the report, said in an interview. The poor reputation of cryptocurrencies such as Bitcoin, which use blockchains to track and validate transactions, has also made the “retail banking sector nervous and cautious,” he said.

Investment banks are experimenting with blockchains to help do everything from issuing bonds to processing payments. Were retail lenders to embrace the technology it could bring benefits for processing remittance payments, managing regulatory issues like know-your-customer and fraud prevention, as well as helping with assessing the financial risk of new or existing customers, according to the report. Relentless pressure on banks to trim expenses could also encourage greater blockchain usage.

“Almost all of their attention, especially in developed markets, is on cost reduction,” Higginson said. “And where cost reduction is front and center they are prepared to look at petty much any opportunity.”

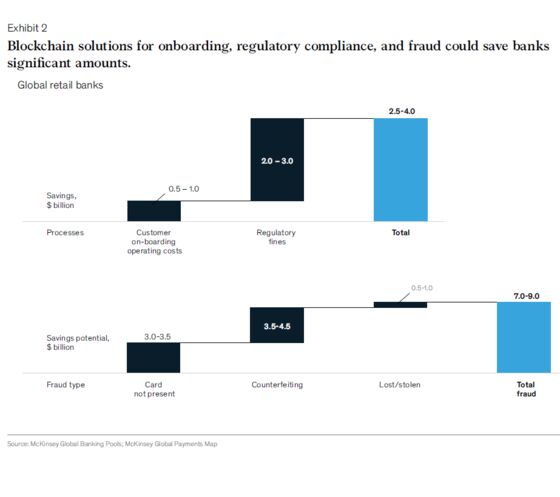

McKinsey estimates that $4 billion a year could be saved by applying blockchain technology to cross-border payments, with a further $1 billion saved annually in operating costs associated with on-boarding clients. “Blockchain solutions” could also reduce annual losses from fraud by as much as $9 billion, according to the report.

Such figures, as well as a greater understanding of distributed systems, could be part of the reason why McKinsey clients have changed their tune on blockchain over the past 18 months. Where previously the consulting firm’s customers asked how to prevent people from buying cryptocurrency with their credit cards, now their questions focus on how blockchain can change their businesses, said Higginson.

Even so, that doesn’t mean consumers on the end of these potential changes will be easily persuaded, said Atakan Hilal, another author of the McKinsey report. “It’s rather difficult in retail banking to change consumer behavior,” he said in an interview.

And that’s just one of a host of challenges to greater adoption. Other larger hurdles include fostering cooperation among firms that have historically viewed each other in the highly competitive banking industry as rivals, as well as the thorny problem of creating a trusted digital identity in a decentralized network, something performed in the legacy financial system by centralized parties like Equifax Inc.

If consumer identities could be created on blockchains, it would ease loan decisions for banks because they’d have an authenticated identification system in place, according to the report.

To encourage broader retail bank adoption exchanging dollars or euros for digital assets should be made easier “so that customers do not risk losses as they switch back and forth,” and a clearer regulatory picture would also help, according to the report.

--With assistance from Luke Kawa.

To contact the reporters on this story: Matthew Leising in Los Angeles at mleising@bloomberg.net;Alastair Marsh in London at amarsh25@bloomberg.net

To contact the editors responsible for this story: Michael J. Moore at mmoore55@bloomberg.net, Dave Liedtka, Brendan Walsh

©2019 Bloomberg L.P.