Blockchain Hype Missed the Mark, and Not by a Little

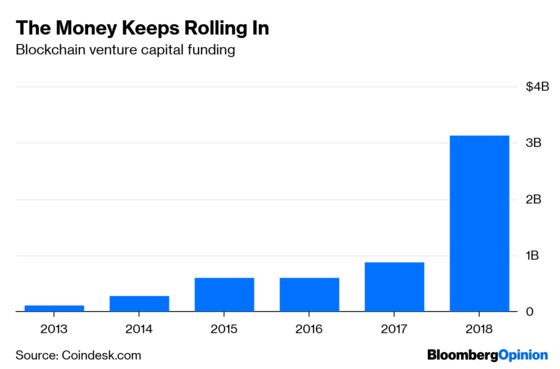

(Bloomberg Opinion) -- Bitcoin’s glory has been a bit tarnished by the bursting of its price bubble since late 2017. But enthusiasm for blockchain technology is still going strong, with venture capitalists throwing almost four times as much money at the sector last year as in 2017:

Some of the biggest deals included cryptocurrency exchanges Coinbase and Robinhood Crypto, nonprofit blockchain-based cloud-computing platform Dfinity, peer-to-peer payments company Circle, and China-based crypto services company PINTEC.

There’s a very good chance that some of these investments will pay off. Even if Bitcoin never recovers, other cryptocurrencies might rise to take its place, and those who own the crypto trading and payments platforms will prosper. And even if no cryptocurrency ever becomes a widespread medium of exchange, crypto may retain its value as an investment for those with a high tolerance for risk — a sort of digital gold. Even if it fails at that as well, it might still be fun to trade — a sort of digital casino for those who are bored with the stock market.

Yet even if none of these predictions are borne out — if cryptocurrencies get added to the list of ideas that were tried and eventually abandoned — there’s a possibility that blockchains, the technology that cryptocurrency is based on, might flourish. Blockchain, essentially, is just a decentralized ledger where records — including monetary transactions, but also potentially things like contracts, votes, document modifications and so on — can be verified without a centralized intermediary like a bank or a court. It would be very strange if such a technology ended up being useful for nothing at all.

For a few skeptics, however, that possibility is very real. Kai Stinchcombe, chief executive officer and founder of True Link Financial, wrote a blog post during the height of Bitcoin mania in late 2017 entitled “Ten years in, nobody has come up with a use for blockchain.” Stinchcombe noted that essentially all of the proposed uses for blockchain technology are more cheaply accomplished by existing intermediaries such as banks, courts, notaries, stock exchanges, big companies or government agencies.

Stinchcombe’s intuition is backed up by some economic theories. In recent years, economists have been scrambling to study the economics of Bitcoin and of blockchains. A 2018 paper by Joseph Abadi and Markus Brunnermeier argues that it’s impossible for any documentation system to be both reliably correct, decentralized and cost-efficient at the same time.

Banks and other human institutions, Abadi and Brunnermeier argue, are reliably correct because their business depends on it. If Bank of America starts stealing people’s money by processing payments incorrectly, there won’t be a Bank of America for much longer. But blockchains don’t have this feature, because the people verifying each entry in the system are different each time. Hence, trust has to be established every time records get modified, which is an expensive process. This is one reason, for example, that Bitcoin sucks up so much electricity.

Abadi and Brunnermeier also note that blockchains compete with each other. A group of blockchain users can always fork off and form a new blockchain. The economists model the resulting competition between the two chains using game theory. They show that forking may mean there are too many blockchains, leading to a chaotic equilibrium where people can’t coordinate on a single network.

Abadi and Brunnermeier might be wrong about the inherent costs of using blockchains. The current trust-establishing algorithms might eventually be replaced with much cheaper ones. But even if technology solves the cost problem, it doesn’t eliminate the need for human institutions to manage blockchain ecosystems. As Stinchcombe points out, blockchains don’t automatically prevent people from stealing your money, impersonating you or otherwise cheating you in ways that leave you little recourse. When someone steals your money through a bank, you often can go to court to get it back; if you relied on a blockchain, you’re out of luck.

This second point is emphasized by cybersecurity expert Bruce Schneier, in his own recent essay on blockchain technology. Schneier argues that blockchains require people to replace trust in institutions with trust in technology. Though institutions can obviously fail — governments and corporations can collapse, corrupt officials and employees can cheat customers and citizens — technology has a lot of much more pedestrian, mundane ways that it can fail people:

If your bitcoin exchange gets hacked, you lose all of your money. If your bitcoin wallet gets hacked, you lose all of your money. If you forget your login credentials, you lose all of your money. If there’s a bug in the code of your smart contract, you lose all of your money. If someone successfully hacks the blockchain security, you lose all of your money.

Schneier also points out that blockchain ecosystems aren’t completely free of the need for human institutions. In the case of cryptocurrency, these are the wallets and exchanges, companies that sell crypto-mining hardware. A recent example of this came when crypto exchange Bitfinex (probably) got ripped off by a company it was using to process payments, which may end up compromising the value of a cryptocurrency held by Bitfinex’s owners. All the techno-wizardry of blockchains can’t overcome the power of good old human dishonesty.

So although blockchains seem like an important technological advancement, they haven’t yet proven themselves. They remain high-cost solutions, often beset by chaotic competition, and they exist in ecosystems beset with dishonesty, fraud and human error. Blockchains might have a chance to change the world someday, but there’s also a chance they will prove useless.

To contact the editor responsible for this story: James Greiff at jgreiff@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Noah Smith is a Bloomberg Opinion columnist. He was an assistant professor of finance at Stony Brook University, and he blogs at Noahpinion.

©2019 Bloomberg L.P.