BlackRock and Ares Are Selling CLOs at Prices Signaling Recovery

BlackRock and Ares Are Selling CLOs at Prices Signaling Recovery

(Bloomberg) -- Money managers are selling collateralized loan obligations at yields that would have been unthinkably low just a few days ago, signaling that one of the more battered corners of the credit market may be healing amid the Federal Reserve’s unprecedented support for company debt.

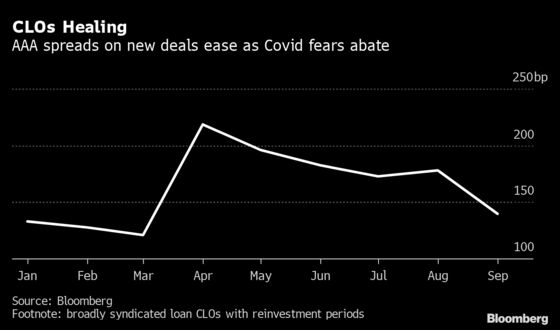

Ares Management Corp. is marketing a CLO that is expected to carry a risk premium, or spread, of just 1.28 percentage point more than the benchmark on its highest-rated portion, according to people with knowledge of the transaction. BlackRock Inc. sold a deal on Thursday with AAA notes yielding 1.27 percentage point more than the London interbank offered rate.

Collateralized loan obligations, or bonds backed by portfolios of leveraged loans, have been one of the last areas of corporate debt market to recover after security prices broadly plunged in March. As the Covid-19 pandemic weighed on company revenues, ratings firms began downgrading leveraged loans, which in turn spooked investors in CLOs. Even as recently as earlier this week, the risk premiums on KKR & Co.’s AAA notes priced at 1.5 percentage point more than Libor.

Spreads in Europe are similarly narrowing, with AAA risk premiums as much as 0.2 percentage point tighter than they were in August. For U.S. deals, the healing in recent weeks has come in part because asset managers have sold so few new CLOs, according to a Wells Fargo & Co. report dated September 9. August only saw $3.9 billion of new CLOs versus more than $9 billion in July, according to Bloomberg data.

“We believe AAAs are still too wide, relative to the rest of the CLO capital stack,” wrote the Wells Fargo analyst team led by Dave Preston.

There are other drivers. Ratings firms have been downgrading fewer leveraged loan borrowers, and even upgrading some. With the Fed cutting borrowing rates to near zero and supporting the investment-grade corporate bond market, some investors are looking for higher returns, and CLOs can be a good place to get that yield, said Jason Merrill, a strategist at Penn Mutual Asset Management.

Of course, before the pandemic, spreads were even tighter, often between 1.17 percentage point and 1.3 percentage point. Libor was much higher then, at around 1.7 percentage point in February compared with about 0.25 percentage point now. So total yields for investors are lower now.

And the securities are different now, too: before Covid-19, the money managers that put together these deals could buy and sell loans in the portfolio for five years, but in the last few months it’s been three years, which reduces risk for investors. Market participants anticipate new CLOs to soon come with four years of reinvestments.

Only the top-tier managers are expected to sell AAA CLOs at spreads of 1.3 percentage point or less. Other asset managers are looking to sell their AAA portions at spreads closer to around 1.35 percentage point, according to the people with knowledge.

©2020 Bloomberg L.P.