A $28 Billion Shopping List for Biogen

A $28 Billion Shopping List for Biogen

(Bloomberg Opinion) -- As the dust settles from the news that Biogen Inc. is halting studies of its lead Alzheimer’s treatment, it’s time to think about what comes next.

The biotech giant is in a bind. Biogen’s key multiple-sclerosis franchise and its rare-disease growth driver Spinraza both face competitive threats, and the firm’s risky pipeline will look very sparse once it does some needed pruning around Alzheimer’s, where it had devoted significant resources. That leaves M&A as logical place to turn for replenishing growth.

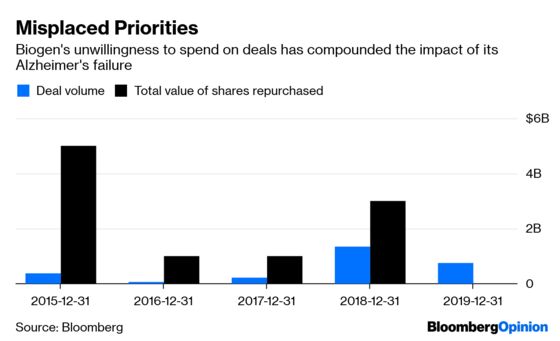

By M&A, I don’t mean takeovers like the company’s $877 million deal for Nightstar Therapeutics Inc. in March. Yes, the acquisition was ambitious by the firm’s recent standards, but Biogen needs more than that to move the dial, ideally in the form of both a near-term sales boost and long-term potential. That won’t come cheap in a buoyant market, and Biogen isn’t exactly in a strong negotiating position. Still, the firm’s Alzheimer’s failure should be the catalyst it needs to get over its unwillingness to spend big.

Biogen’s balance sheet isn’t the problem. It had $4.9 billion in cash on hand and $5.936 billion in debt at the end of 2018. And while its prospects for near-term growth are slim, the company still should generate $5 billion or more in annual free cash flow over the next few years. If Biogen is willing to lever up, it could afford an acquisition or acquisitions approaching or exceeding $20 billion in total.

A few names stand out of the crowded small-to-mid-cap biotech field that are within range and could have a real impact:

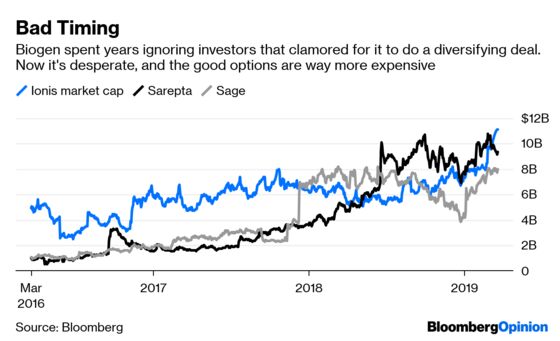

SAGE THERAPEUTICS INC.: The developer of depression remedies is among the possible targets that Mizuho analyst Salim Syed highlighted in a research note Thursday. The firm’s new drug Zulresso just won the first-ever approval from the Food and Drug Administration for treating postpartum depression, and its next-generation pill SAGE-217 has multi-billion dollar sales potential in a broader patient population. Expectations are high and upcoming trial data could disappoint, but early results were very promising and the possible upside could be worth the risk. Valued at $8 billion, Sage is one of the cheaper options that could truly make a difference for Biogen.

SAREPTA THERAPEUTICS INC.: Syed also suggested Sarepta, which has a marketed drug for a rare muscle-wasting condition and other treatments on the way. It’s a more logical fit for Biogen, which has turned Spinraza into a blockbuster in spinal-muscular atrophy. Several of Sarepta’s prominent pipeline programs are gene therapies, in which Biogen has shown clear interested. Sarepta wouldn’t provide a huge near-term sales boost relative to its $9.3 billion price tag, but it offers scale in an important new drug category that could help support long-term growth.

IONIS PHARMACEUTICALS INC.: Ionis and Biogen are already close. The smaller firm developed Spinraza, and the two companies signed an expanded research partnership last year under which Biogen acquire an 8.31 percent stake in the company. It might be time to deepen the relationship further. Acquiring Ionis outright would allow Biogen to consolidate ownership of Spinraza and other partnered programs and take control of a productive drug-discovery platform. Ionis has other marketed drugs and a large pipeline, and the fact that Biogen is a large shareholder could drop the $11.1 billion starting point for negotiations.

Even as these targets offer a potential path forward, their relatively lofty prices highlight the cost of Biogen’s strategic and financial parsimony. It could have leaped at these opportunities when they were less expensive and it was in a better negotiating position. Instead, Biogen chose smaller deals and an ill-advised Alzheimer’s gamble.

Biogen could wait for prices to come down, but it might not have that luxury if it’s independently minded. The firm’s diminished share price makes the company itself a potential acquisition target, and management won’t like the prices that bargain seekers propose. Be that as it may, for Biogen it may be a case of buy or be bought.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Max Nisen is a Bloomberg Opinion columnist covering biotech, pharma and health care. He previously wrote about management and corporate strategy for Quartz and Business Insider.

©2019 Bloomberg L.P.