Biogen Stays the Wrong Course After a Key Drug Failure

Biogen Stays the Wrong Course After a Key Drug Failure

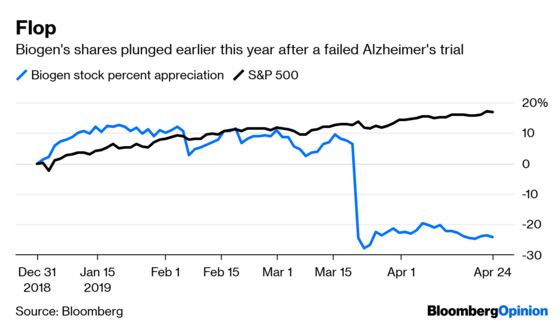

(Bloomberg Opinion) -- Biogen is by far the worst-performing large-cap biotech stock of 2019 after the March failure of its key Alzheimer’s drug pushed its shares down more than 20 percent. Its first-quarter earnings results announced on Wednesday, while beating analysts’ profit estimates, did little to turn things around. A much-needed strategic shift was missing.

Biogen’s Alzheimer’s disaster should have sent a clear message that its approach to a poorly understood disease is fundamentally flawed. Biogen took a step toward acknowledging that reality Wednesday by saying it won’t move forward with a previously planned study of that failed drug.

But it’s dragging its feet on a more thorough overhaul. Instead of scrapping similar programs, the company is still poring over data and hoping that a different approach that also has a spotty track record will prove more successful. Alzheimer’s medicines continue to be a significant portion of Biogen’s pipeline despite growing evidence that it should direct its resources elsewhere.

What should have been a seismic event for the company doesn’t appear to have changed its mindset all that much. Biogen’s biggest investment this year has been in its own shares, and the company continues to focus heavily on its internal neuroscience pipeline. The company plans to release data on 10 mid- and late-stage programs by the end of 2020.

A big proportion of these are high-risk bets, especially in the context of Biogen’s spotty R&D track record. Not every neuroscience ailment is as difficult to treat as Alzheimer’s, but a lot of new and unproven approaches are on that 10-drug list.

When asked on Wednesday’s analyst call whether he felt an urgent need to diversify through M&A, Biogen CEO Michel Vounatsos was not exactly committal. He suggested that the firm has the financial firepower to buy both shares and other businesses and went on to say that the company has already materially diversified its pipeline.

A deal that would truly move the dial would take the full commitment of Biogen’s cash, balance sheet and strategic focus. The firm’s leadership doesn’t seem willing to commit to that.

That’s concerning for investors who want a shift away from risky neuroscience bets. The company’s $877 million deal in March for Nightstar Therapeutics and its fairly distant eye-drug candidates doesn’t measure up to the firm’s near-term difficulties or count as significant diversification.

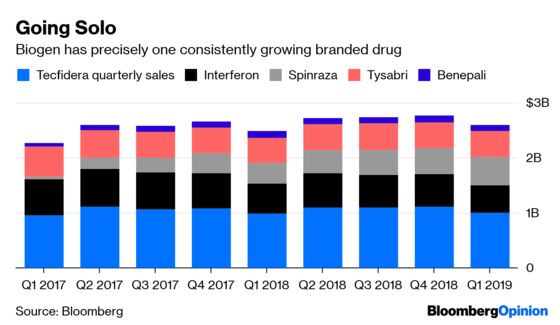

Biogen has only one branded drug that is consistently growing sales: Spinraza, its treatment for rare muscle wasting disease. The medicine’s strong international sales are the only reason the firm’s first quarter looked good, but its days of sure growth may be numbered. A promising gene therapy from Novartis AG is likely to hit the market this year, and Roche Holding AG has a different drug on the way as well.

Sales of the firm’s core multiple sclerosis franchise are eroding because of heightened competition, and a patent challenge to Biogen’s best-selling drug Tecfidera could accelerate the decline. Even if several of Biogen’s R&D bets hit, regulatory and introduction timelines are long enough that they may not be able to save the company’s sales growth from screeching to a halt.

Staying the course and hoping that research gambles pay off has been a losing strategy for Biogen. It’s past time for the company to try something new.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Max Nisen is a Bloomberg Opinion columnist covering biotech, pharma and health care. He previously wrote about management and corporate strategy for Quartz and Business Insider.

©2019 Bloomberg L.P.