Billionaire Greensill’s German Bank Draws Regulatory Scrutiny

Billionaire Greensill’s German Bank Draws Regulatory Scrutiny

(Bloomberg) -- When billionaire Lex Greensill won an $800 million investment from the SoftBank Vision Fund last year to develop new technology and expand his trade-finance empire, the bulk of the money went to a small, unprofitable German lender.

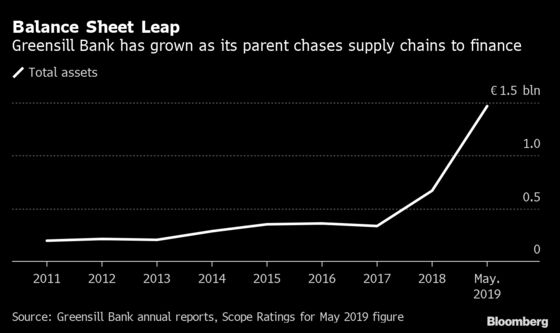

Greensill Bank, a 93-year-old firm known as NordFinanz Bank AG until the Australian financier bought it in 2014, suddenly found itself flush with capital. The size of its balance sheet increased more than seven-fold while it offered above-market interest rates to attract deposits that it would then invest in assets sourced by its parent, Greensill Capital.

The growth of the Bremen-based bank has attracted the scrutiny of Germany’s main regulator as well as its deposit-insurance program, according to people familiar with the matter. They worry that too many of the assets on the bank’s books are ultimately tied to the same source: British-Indian entrepreneur Sanjeev Gupta. The watchdogs have been reviewing the portfolio to determine the extent of the ties and are considering imposing caps or additional capital demands if they deem that the concentration isn’t low enough, the people said, asking not to be identified because the matter is private.

The regulators’ concerns highlight the challenges for Greensill as he takes on the large Wall Street banks in the business of supply-chain finance. A former banker himself at Morgan Stanley and Citigroup Inc., he has vowed to take a big chunk of that market by buying trade receivables or payables, packaging the short-term debt and selling it to investors. Greensill Bank functions as a “warehouse” for such deals, he told Financial News last year.

Gupta is the head of GFG Alliance. He invests in and revamps moribund steel and power plants. Securities linked to Gupta and arranged by Greensill were among investments at the center of a 2018 crisis at Swiss asset manager GAM Holding AG that brought down star trader Tim Haywood. They also featured prominently in supply-chain finance funds at Credit Suisse Group AG, for which the bank teamed up with Greensill.

The problem, in the eyes of the regulators, is that a large portion of Greensill Bank’s credit portfolio is made up of loans to customers of companies that Gupta controls, the people said. Debts sourced from a group of linked companies made up around two-thirds of loans at the bank, according to a report published in August 2019 by Scope Ratings, a privately held company based in Berlin that specializes in ratings of financial institutions.

Since the Scope report was published, the share of Gupta-linked loans has been cut and it’s possible that no regulatory steps will be taken, the people said. Greensill has also made a number of acquisitions to help grow and diversify its trade-finance portfolio, among them Finacity, a boutique that specializes in securitizing receivables.

Even if assets linked to Gupta have been reduced from previous levels, regulators are concerned about high concentration to a single group, the people said. Having a lot of assets tied to one source could leave Greensill Bank at risk of losing a big chunk of investment income should that source disappear, particularly since many of the assets are short-term.

The Association of German Banks, which runs the voluntary deposit-insurance program for private-sector lenders, recently concluded a probe into Greensill Bank that was conducted through an independent assessment unit. The review, which isn’t public, showed reservations about risk concentration in the bank’s portfolio, the people said.

‘Constructive Dialogues’

BaFin, too, views the Gupta-linked assets on the bank’s balance sheet as an excessive concentration risk and is considering additional capital demands and a cap on the exposure, the people said. BaFin hasn’t made a decision, and it’s also possible that the regulator won’t act if the concentration risk is reduced further.

“Greensill Bank is strongly capitalized, is in full compliance with its regulatory requirements, and all its trade receivables are fully insured,” said a spokesman for the firm. “We have regular, constructive dialogues with the appropriate regulators in Germany and all jurisdictions where we operate.”

Representatives for BaFin, the banking association and its assessment unit declined to comment, as did a spokesman for Gupta’s GFG.

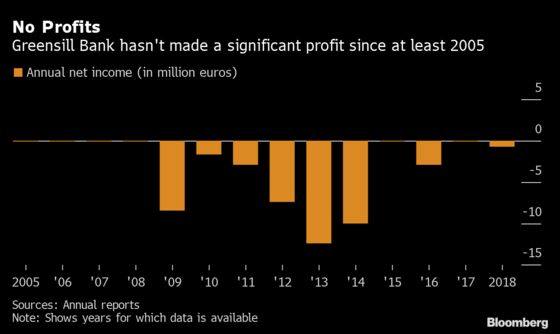

Neither Greensill Bank nor its predecessor have made an annual profit beyond a break-even in the decade through 2018, according to publicly available documents. Scope said the lender turned profitable in the fourth quarter of 2018, and posted an operating profit of 2.6 million euros in the first five months of 2019, helped by the recent capital injection.

Scope noted in its report that the financial performance of Greensill Bank “will depend crucially” on the parent’s ability to generate enough assets for the bank to invest in. Its performance is also impacted by costs to hedge against currency swings and insure assets against default, the report said.

The bank currently pays a 0.7% interest rate for euro deposits that are placed for a year. That’s the highest among the German banks listed on Weltsparen.de, a comparison website. Customer deposits more than tripled to 960 million euros from the end of 2017 to May last year, according to the Scope report.

Membership in the deposit insurance is crucial for banks operating in Germany to reassure clients their money is safe. Greensill Bank displays its association membership prominently on its website. Because it has no branches, it relies on brokers and retail websites to win customers.

BaFin may be particularly zealous in guarding against any potential issues after coming under fire this year for failing to prevent a massive accounting fraud at payments provider Wirecard AG. While Wirecard owned a German bank that was supervised by BaFin, the rest of the company wasn’t, because it was viewed mainly as a technology firm.

Greensill, too, describes itself as a fintech, though much of its technology is from third-party providers. In its early days, a lot of its business was tied to Gupta, for whose companies he has arranged hundreds of millions of euros in financings.

Haywood’s funds at GAM, for instance, held large amounts of notes tied to Gupta’s companies that were sourced by Greensill. The investments worked well for Haywood, who ran the firm’s second-biggest strategy by assets at the time. But after an internal probe uncovered potential misconduct issues by the fund manager, GAM suspended him in mid-2018, saying he didn’t do sufficient due diligence on some holdings and that he broke the company’s gift policy.

Haywood, who has since left GAM, has rejected the allegations.

His suspension triggered a flood of redemptions, forcing GAM to freeze Haywood’s funds because it couldn’t find a buyer fast enough for some of the assets. GAM eventually returned all investor money in the funds with a small profit, though it took almost a year to offload more than $1 billion of bonds linked to GFG projects.

Credit Suisse’s asset management arm, which had bought Gupta-linked assets as well through its supply-chain finance funds, also trimmed its holdings at the time.

When Masayoshi Son’s SoftBank Vision Fund agreed in May of last year to invest $800 million in Greensill Capital, it came at an opportune time. The collapse of Haywood’s funds had left Greensill without a major buyer of his trade-finance notes. GAM funds had also provided 300 million euros of direct loans to Greensill Capital through a vehicle called Laufer.

‘Liquidity Requirements’

“The Vision Fund’s investment will accelerate Greensill’s development of new technology to further improve access to capital for companies globally and meaningfully enhance the firm’s ability to support the development of a broad, liquid capital market for working capital finance assets,” Greensill said in a press release at the time. Greensill also said at the time that it would make a push into markets such as Brazil, China and India.

Most of the money went into the German lender, according to Scope and an interview with Greensill by Financial News last year. Having a “bank with oodles of cash” was a hedge against economic uncertainty, he told Financial News at the time. Greensill Bank “is as much as anything a warehouse that provides us with the ability to manage the liquidity requirements of our business.”

It’s not clear whether any of the Gupta assets GAM was liquidating ended up on the balance sheet of the freshly capitalized Greensill Bank at the time. SoftBank provided another $655 million capital injection in October, to finance Greensill’s global expansion and development of new products.

A spokesperson for SoftBank declined to comment.

©2020 Bloomberg L.P.