Fintechs Boom With Cash-Loving Argentines Stuck at Home

Fintechs Boom With Cash-Loving Argentines Stuck at Home

(Bloomberg) -- In Argentina, where cash is king, a strict lockdown to halt the spread of the coronavirus is finally pushing suspicious consumers into formal banking and online payments.

Before quarantines began March 20, more than half of all Argentines didn’t have a bank account. Many people -- scarred from decades of hyperinflation, seizures and devaluations -- instead preferred to make everyday payments in person and in cash. But now that they’re forced to stay home, demand for credit cards, new accounts and wallet apps has surged.

The shift in how people pay for goods and services has been a boon for digital payment platforms and banks. Mobile payments startup Ualá, backed by billionaire George Soros, issued 127,000 new prepaid cards since the lockdown began, a 20% jump in a month, while digital bank Brubank says it has more than 80,000 new clients. And Mercado Pago said the number of bills paid on its mobile wallet app doubled in the final two weeks of March.

“The change we expected over years is happening in weeks,” said Pierpaolo Barbieri, founder and chief executive officer at Buenos Aires-based Ualá. “Ever since the quarantine started, we’ve seen an unprecedented acceleration in requests for new accounts.”

The stay-at-home orders have already been extended twice, with no clear end date in sight.

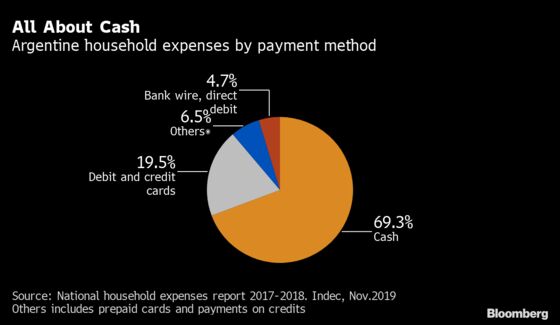

A November survey by national statistics agency Indec showed that almost 70% of all household expenses are paid in cash, with food and tobacco among top purchases. Underscoring how dependent most people are on hard currency, thousands of pensioners and other citizens rushed to collect government welfare payments and stood in long lines when banks reopened on April 3.

Informal Economy

One reason physical money is still so heavily used is because of the high proportion of Argentines in the gig economy. Almost half of all workers were in the informal sector, including jobs like street vendors and maids, according to a 2018 study by the Catholic University of Argentina’s research institute.

Juan Bruchou, Brubank’s founder and former Citigroup Inc. executive, said more inflow is coming from “clients who have never had a bank account before.” Brubank has no branches and users of its mobile-phone banking platform has climbed to half a million since its January 2019 founding.

Traditional banking service providers haven’t been left behind in the shift. Prisma Medios de Pago, whose clients include banks and financial institutions, has printed about 2 million debit and credit cards in the first month of the lockdown. The push is focused on pensioners and the so-called un-banked, said Liliana de Gregorio, Prisma’s head of operational engineering.

There’s plenty of room to grow, said Ualá’s Barbieri. “Argentina’s level of financial inclusion is below its peers,” he said. “Even within the region.”

The companies have also been aided by growing government efforts to provide some of their pandemic-related support vouchers through digital systems, said Stelleo Tolda, chief operating officer of MercadoLibre, the parent company of MercadoPago. Argentina and Brazil are two of the countries in the region that have tried this.

“We always say that paper money is our worst enemy,” Tolda said. “Being able to make a digital payment is a lot more efficient-- for security reasons, for tracking reasons, and now we’re also seeing for health reasons.”

©2020 Bloomberg L.P.