Big Muni-Bond Trades Drop With Wall Street Bracing for Headwinds

Big Muni-Bond Trades Drop With Wall Street Bracing for Headwinds

(Bloomberg) -- With muni-bond prices retreating from the highest in decades and the pace of debt sales poised to pick up, big block trades are on the decline.

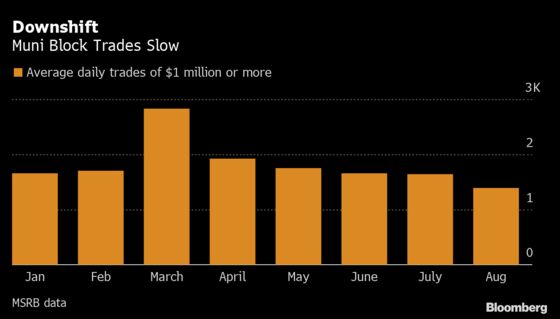

Average trades of state and local government bonds of $1 million or more fell below 1,540 -- the 10-year average-- in the second week of August and declined to about 1,330 during the last two weeks, according to Municipal Securities Rulemaking Board trade data. August was the first month this year to fall below the long-term average.

There may be many reasons behind the decline, said Citigroup Inc.’s Kevin Danckwerth, the bank’s co-head of muni-bond trading. The seasonal slowdown in debt payments, looming credit-rating downgrades and uncertainty about the presidential elections is giving investors pause, he said.

Adding to that is a heavy new-issue calender and yields that are holding not far from the lows hit early last month, when those on top-rated 10-year debt were as little as 0.54%. And mutual funds have been receiving a steady stream of cash, leaving them no reason to unload big lots of bonds in the secondary market.

“Investors have been able to source what they’ve wanted to buy in the primary,” said Danckwerth. “And frankly there just hasn’t been much selling because the mutual fund flows have been solid.”

The slowdown in big trades comes as the market is weakening. State and local government debt in August had its first loss in three months as yields edged up, and the fall is typically a difficult season because governments step up borrowing while the amount of cash returned to investors from principal and interest payments falls. On average, since 2013, municipal bond prices have declined in September, October and November, according to Municipal Market Analytics.

While muni mutual funds have raked in cash for 17 straight weeks, the flows have slowed to a trickle. Investors added about $139 million to such funds during the week ended last Wednesday, down from some $2.3 billion during one week in August, according to Refinitiv Lipper US Fund Flows data.

Capital Gains

But unless there’s money pulled out, fund managers aren’t keen on selling bonds that have appreciated in price because they’ll have to pay capital gains taxes and replace them with lower yielding securities, said Nick Venditti, senior portfolio manager at Wells Fargo Asset Management.

“It’s really hard to trade bonds in an economic manner,” Venditti said. “No one is super excited about flipping out of positions and losing that book yield.”

The decline in institutional-sized trades is noteworthy because it’s the first time in months that the daily average has fallen below the long-term average, despite the sizable amount of new bonds sales in the last two weeks of August, said Tom Doe, president of Municipal Market Analytics. MMA noted the trend in a client webinar last week.

“We know the bonds in the primary are being placed effectively, a good thing,” Doe said. “But it also means there’s perhaps less capital available in the secondary market and could be an issue should we have something of a more harsh correction later this year.”

But Citigroup’s Danckwerth said the trading decline shouldn’t raise concerns about liquidity. A key barometer of bond dealers’ willingness to commit capital, the competitive underwriting market, is strong, he said. Auctions of new municipal bonds are drawing between five and 10 bidders and sometimes more, compared with two or three at times in March, when a swift pullback by investors caused dealers’ inventories to surge and trading costs to soar.

“When I see that type of capital willing to be deployed by the dealer community, I feel like dealers are in a position to provide capital,” Danckwerth said. “We’ve added a little bit of risk over the past few weeks as the market’s cheapened up, but there may even be better opportunities as the year progresses.”

©2020 Bloomberg L.P.