Beyond Meat's Forecast Wows Wall Street as IPO Darling Delivers

Beyond Meat's Forecast Wows Wall Street as IPO Darling Delivers

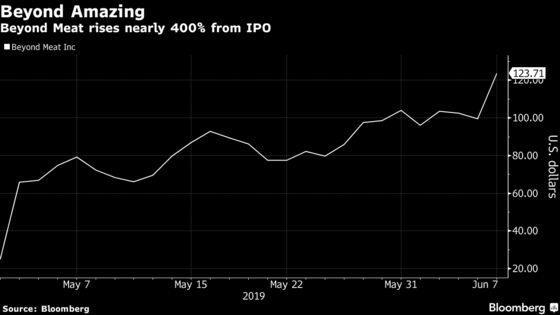

(Bloomberg) -- Beyond Meat Inc. shares soared to a record Friday after the faux-meat maker’s forecast for annual sales topped estimates.

Analysts are putting their faith in management’s comment that the company is being “very conservative” in its projections, and that the sales outlook doesn’t include foodservice customers until they are past the testing phase. This served as a green light for analysts to raise their revenue estimates above the IPO darling’s target.

Shares rose as much as 36% Friday to $135.80 each, a record high. The stock has gained more than 400% from its May 1 initial public offering price of $25.

The non-stop rally, however, has frustrated short sellers, who are trading in 34% of the stock’s limited float, which represents 19% of the shares outstanding. The shorts were down $155 million in mark-to-market losses Friday, bringing their losses to $321 since trading began, according to financial analytics firm S3 Partners.

Here’s what Wall Street has to say:

JPMorgan, Ken Goldman

“As long as Street forecasts fail to properly reflect BYND’s remarkable potential, we remain overweight.” Notes that “eventually this stock’s hefty valuation will more than offset the fast-growing fundamentals.”

Notes the importance of CEO Ethan Brown calling the forecast “very conservative” and telling investors that the company doesn’t include foodservice customers in guidance until they are past the testing stage.

JPMorgan has a $233 million 2019 sales target -- vs the company forecast of $210 million -- and the analyst says his estimate may be conservative. “It is conceivable that Tim Hortons alone (a current customer with nearly 5,000 locations that is not yet in guidance) could account for most of that gap.”

Rates overweight, price target to $120 from $97

Bernstein, Alexia Howard

The year sales forecast does not include the “onboarding” of new customers until they are post trial; due to this, the company management believes that the target may be conservative.

“The preliminary repeat rate is also encouraging in the 40%-50% range.”

“We continue to expect significant growth potential in the plant-based meat category and believe that Beyond Meat is well positioned as one of the front-runners leading the new wave of plant-based meat products.”

“Beyond Meat has traded in a highly volatile manner since its IPO likely partly due to its limited public float, and we expect continued volatility at least in the near-term.”

Rates outperform, price target to $107 from $81

Credit Suisse, Robert Moskow

“The stronger outlook has led us to increase our estimates for Beyond’s revenue potential and the size of the plant-based meat category’s addressable market in the medium term.”

Moskow boosts his 2019 revenue estimate to $224 million and his 2030 sales estimate to $3.5 billion up from $3 billion. He expects management to keeps boosting revenue guidance this year as the big chains like Tim Hortons “transition out of test and into full market distribution.”

“Accelerating distribution will fuel positive revenue revisions. Inbound interest from restaurant chains has increased following the tremendously positive publicity during the Beyond Meat IPO.” He now expects $750 million of sales to McDonald’s Corp. alone by 2030.

“A&W and Burger King restaurants both reported strong overall same-store sales growth in the stores that tested plant-based meat products. This is hugely important because it means that the brand is driving same-store foot traffic rather than just cannibalizing existing sales.”

Rates neutral, price target to $125 from $70

Bank of America Merrill Lynch, Bryan Spillane

“Superior product, first mover advantage and influencer-supported authenticity are competitive advantages as ‘old food’ competitors enter the market.”

“Expansion in Europe/Asia and added QSR (quick service restaurant) companies are potential areas of upside.”

“BYND is positioned well to disrupt the U.S. meat industry, but with risks as more companies ramp up.”

Rates neutral, price target $101 from $85

To contact the reporter on this story: Janet Freund in New York at jfreund11@bloomberg.net

To contact the editors responsible for this story: Catherine Larkin at clarkin4@bloomberg.net, Will Daley

©2019 Bloomberg L.P.