Beyond Meat Craters on ‘More Depressed Than Expected’ Sales

Beyond Meat Craters on ‘More Depressed Than Expected’ Sales

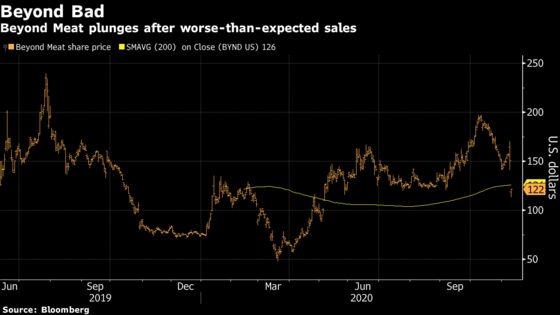

(Bloomberg) -- Beyond Meat Inc. shares plummeted on Tuesday after the veggie-burger maker reported third-quarter revenue that was 28% below the consensus view.

Beyond’s retail channel is being pressured by Impossible Foods’ entry into the market, Bernstein analyst Alexia Howard wrote. She called the quarterly sales result “even more depressed” than anticipated. Howard rates the stock underperform and slashed her price target to $89 per share from $136, citing a “tougher-than-expected outlook for the next few quarters.”

The shares fell as much as 25% to $113.26, marking the biggest intraday decline since June 2019. Shares touched the lowest since May.

Jefferies Rob Dickerson told clients in a note that the third-quarter “dent” will likely “lower conviction on 2021 growth trajectory potential” given that the “timing and magnitude of both revenue and margin recovery” were not spelled out by management. Dickerson rates Beyond Meat hold (price target $117 from $118).

Elsewhere, the drop in the stock price spurred two analysts to upgrade their opinion on Beyond Meat shares.

The decline makes the stock attractive, given that McDonald’s Corp. is working with the company to roll out plant-based patties, said Piper Sandler analyst Michael Lavery, who lifted his rating to overweight from neutral while lowering his price target to $144 from $178.

“We see opportunity as a long-awaited McDonald’s launch is set to start, and encouraging vaccine news may help food service broadly,” Lavery wrote in a note to clients. A survey conducted by Piper also suggests plant-based foods appeal to younger consumers, which could drive growth over time as customers age, the analyst said.

UBS analyst Erika Jackson upgraded the stock to neutral from sell, citing the third-quarter earnings-related selloff. Jackson wasn’t surprised by the postmarket drop as the company saw “outsized foodservice headwinds” and “elevated price/mix headwinds.” But following the plunge, she said her “lower estimates, Covid-19 challenges, and price/mix headwinds” are already reflected in the stock price.

Further, Jackson estimates that the El Segundo, California-based company’s collaboration with McDonald’s could add around $150 million of annual revenue. She is also positive on the 10,000 new new points of distribution the company added in the third quarter.

But risks remain over the next 12 months, she said. They include continued promotional and pack-size headwinds, increased marketing spending as Beyond Meat “aims to reach new households” amid more intense competition and a recession that may lead to a consumer trade-down. Jackson trimmed her price target to $107 from $110.

Read More: Beyond Meat May See More Earnings Volatility: BI

Still, some on Wall Street were not as optimistic about the collaboration with McDonald’s. Adam Samuelson, an analyst at Goldman Sachs who rates Beyond Meat sell, wrote that “increased uncertainty on the nature and scope of this relationship will be a headwind to shares, and more broadly reinforces our concern that Covid is delaying incremental menu innovation at food-service operators that can slow trial and household penetration,” tempering the near- to medium-term growth trajectory for Beyond Meat.

Beyond Meat’s stock closed at $150.50 a share on Monday, up about 500% since a May 2019 initial public offering at $25.

©2020 Bloomberg L.P.