Best Emerging-Market Bonds Are From Argentina’s Junk-Rated MSU

Best Emerging-Market Bonds Are From Argentina’s Junk-Rated MSU

(Bloomberg) -- Back in July, it seemed as if the outperformance of junk-rated notes from Argentine power generator MSU Energy was an anomaly. Five months later, it’s a lot less of a surprise.

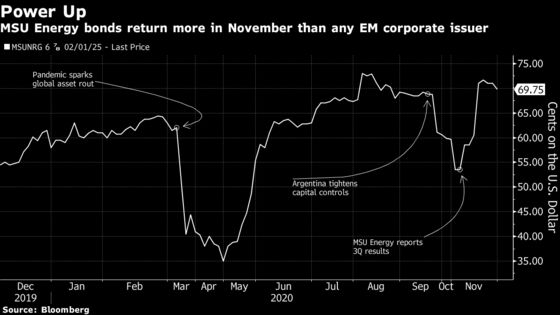

The company’s $600 million of overseas notes due in 2025 returned almost 31% last month, handily beating all other corporate peers from the developing world. The reason: Power plant upgrades that drove a 27% increase in third-quarter earnings, plus a steady stream of dollar-based revenue that leaves it less squeezed that other local firms by the latest foreign-exchange controls.

Chief Financial Officer Hernan Walker said on the quarterly earnings call last month that MSU isn’t expecting any changes to its revenue streams anytime soon. He cited long-term power purchasing agreements with the Argentine government that are paid in dollars and account for 92% of revenue. MSU, based in Buenos Aires, manages three natural gas-fueled power plants for a total 750 megawatt output capacity.

The rally is all the more remarkable because just four months ago, Argentina investors were buying the bonds on a bet that the nation’s sovereign debt restructuring, which took place in early September, would jump-start a recovery in South America’s second-largest economy.

That didn’t happen. Instead, the government’s patchwork economic policies sent investors fleeing as authorities tried to control a currency crisis and bring back foreign reserves that have slumped to a four-year low.

Argentine bonds, MSU included, tumbled in September, and sovereign bonds now trade at about 30 to 40 cents on the dollar, well below the 55-cent restructuring price. MSU’s bonds due in 2025, by contrast, fetch almost 70 cents on the dollar.

There are risks, including a $103 million loan from General Electric Co. that will keep MSU’s liquidity tight in the year to come, according to Roger Horn, an emerging-market strategist at SMBC Nikko Securities America in New York. There’s also a risk of payment delays from Cammesa, the state-controlled electricity wholesaler, Horn said in an interview.

Still, upgrades to two of MSU’s thermal energy power plants are giving investors faith the firm will prove a stable credit, Horn said. “The completion of the plant upgrades was a big catalyst for the gains,” he said.

MSU plans to repay the GE loan before the first principal payment comes due on the company’s 2024 bonds next November, Walker said last month.

©2020 Bloomberg L.P.