Banks Waking Up to Fintech Threat Throw Billions Into Digital

Banks Waking Up to Fintech Threat Throw Billions Into Digital

(Bloomberg) -- Scrappy online financial startups have spent the past few years building buzz, backing and the beginnings of a customer base.

For a while, the world’s banking giants largely ignored them. Now they’re starting to feel the heat—and fighting back with the most formidable weapon in their arsenals: cash.

Spain’s Banco Santander SA announced a few weeks ago that it will funnel 20 billion euros ($22 billion) into digital transformation and information technology in the next four years.

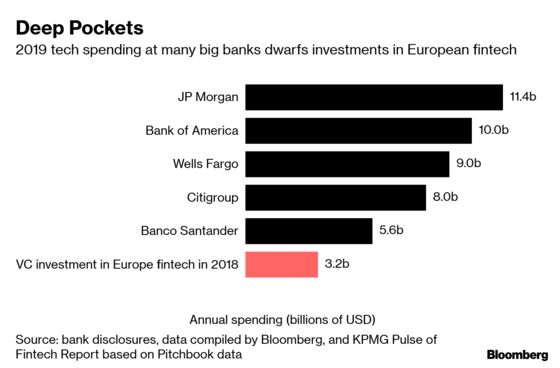

On an annual basis, that works out to one-and-half times all of the venture capital Europe’s fintech startups received in 2018—a disparity highlighting that, despite all their rhetoric about burying existing banks, fintech firms and neo-banks are still monetary pipsqueaks facing an uphill battle against entrenched competition.

“I am more pessimistic than ever for these startups,” said Mark Tluszcz, a partner at Luxembourg-based venture capital firm Mangrove Capital, who’s been a vocal skeptic of the fintech sector. “Even though we all love to hate our bank, we still fundamentally trust the bank that, if we put our money there, it is not going to disappear overnight. And the fintechs have struggled to win that trust.”

In a matter of years, digital banks like Revolut Ltd., Starling Bank Ltd. and Monzo Bank Ltd., all based in London, have attracted several million clients by offering perks like ultra-low-cost money transfers and pre-paid debit cards with no foreign transaction fees. Yet even though people open secondary accounts with these neo-lenders, they’re still reluctant to give them their salaries—let alone make them the main conduit for their retirement savings or mortgages.

This has bought big banks time to attempt to beat the fintechs at their own game, a challenge some are seizing more boldly than others. Even with its 20 billion-euro blueprint, Santander would be only No. 5 globally when ranked by annual technology spending; JPMorgan Chase & Co., the top spender, has committed $11.4 billion in 2019 alone.

The Spanish lender operates in about 30 countries worldwide and already runs Openbank, a standalone online and mobile-banking unit in Spain that has rolled out a host of snazzy products and services. It raised its digital game last year by starting a money-transfer platform called One Pay FX that uses Blockchain-inspired technology and allows its clients to send money abroad within hours, instead of the days it can typically take at a bank. Santander also now has an app-only bank called Superdigital in Brazil to target lower-income users who normally wouldn’t have a bank account, a model it plans to roll out across Latin America.

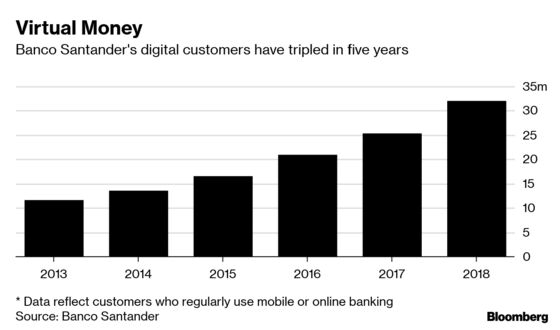

Working on all these fronts has helped Santander build an online and mobile customer base of 32 million, compared with 4 million users at Revolut, which recently got a banking license to allow it to attract deposits.

“We must as banks be able to service all of customers in all channels,” Ana Botin, Santander’s group chairwoman, told analysts and investors in early April at the bank’s investor day. She said the only way to do that with acceptable profit margins was to use a digital-based business model.

For now, fintechs say they aren’t spooked by the sizable tech budgets. Traditional lenders are merely trying to catch up, not push innovation, according to Monzo’s head of marketing, Tristan Thomas. “So far they seem to be focused on skating to where the puck is, rather than where it’s going,” he said.

And while most fintechs are turning losses, they have one big thing going for them: they don’t have outmoded technology weighing them down. Many major banks would need to spend billions of dollars just to bring their IT systems into the 21st century. Even Santander’s Parthenon back-end software platform is increasingly antiquated even though it is newer than what a lot of the other European banks use.

“While they can copy our features, they cannot copy our cost base,” Starling Bank said in a statement. “They have to contend with legacy technology, not to mention the massive costs of maintaining a branch network and the slowness to action that is inevitable with large bureaucracies.”

All those costs ultimately get passed on to customers in one way or another, according to Kristo Kaarmann, the chief executive officer and co-founder of TransferWise Ltd., which offers cheaper international money transfers. “If you spend a lot, you have to charge a lot,” he said, adding it would make far more sense, from a cost basis, for the banks to partner with fintechs than to try to duplicate their offerings.

Of the 20 billion euros Santander is spending by 2022, 3 billion euros annually will go toward operating expenses, like keeping its current technology running, licensing software, renting server space in data centers and paying the six-digit salaries needed to lure new hires in fields like data science and artificial intelligence.

The rest, 2 billion euros a year, will be used to invest in things like new computers and moving more of Santander’s data onto cloud computing so they can be more easily accessed through the Internet. Shifting to the cloud and changing internal management processes to those most often used by software companies will help the bank realize 30% cost efficiencies, according to Dirk Marzluf, Santander’s group head of technology and operations.

With financial rules in Europe forcing lenders to give startups read and write access to their customer’s data, big banks can’t afford to disregard the rise of fintechs. It’s not just the virtual banks encroaching on their turf—startups are offering to manage people’s retirement savings and giving investment advice without human intervention.

The risk for conventional banks is that they wind up being used as utilities that simply provide a safe place to deposit money, according to Tara Reeves, a London-based venture capitalist who has led investments in a number of fintech startups.

For now, though, their giant budgets will loom large over the fintech industry—especially if digital banks fail to win over deposits in the next few years.

Fintechs will need to build “a truly different customer journey” to capture significant market share, said James Lloyd, the Asia Pacific financial technology lead for consulting firm Ernst & Young LLP. “I don’t think it will be sufficient to just have another bank product in a digital format, offering a slightly better customer experience.”

--With assistance from Alfred Liu.

To contact the editor responsible for this story: James Hertling at jhertling@bloomberg.net, Daliah Merzaban

©2019 Bloomberg L.P.