Banks Boost Protections for Sterling Loans in Brexit Shadow

Banks Boost Protections for Sterling Loans in Brexit Shadow

(Bloomberg) -- The intensification of Brexit woes hasn’t entirely deterred banks from drawing up sterling deals in Europe’s leveraged loan market, but arrangers are cushioning themselves with additional protection.

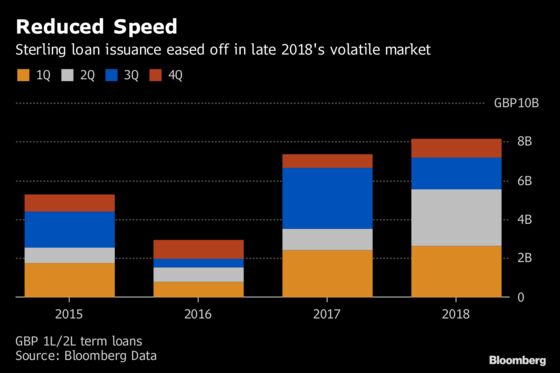

Transactions in the U.K. currency have become difficult as lenders sharpen their focus on credit quality due to the uncertainty around Britain’s future in the European Union, reducing the pool of liquidity. Still, banks are cautiously moving ahead with some deals.

Independent Vetcare Ltd. has found lenders for the sterling portion of its 1.2 billion pounds ($1.6 billion) loan refinancing and the buyout financing for catering business WSH Investments Ltd. includes sterling-denominated debt.

But RPC Group Plc’s debt financing is notable in its reliance on dollars and euros, even if the door has been left open to raise some sterling on a best-efforts basis.

Arrangers have walked away from some sterling deals deeming them just too risky right now, but some are still working with private equity sponsors that want to raise sterling financing.

To underwrite a sterling deal now, arrangers need to be highly confident in the credit story and how Brexit will impact the business. Banks may particularly prefer companies that are insulated from any possible change to trade laws in case of an exit from EU, and those that aren’t exposed to U.K. consumers.

Aside from credit comfort, good flex provisions are key and arrangers may hold preliminary discussions with lenders to gauge appetite and pre-place blocks of paper before formally launching, a tactic used on Independent Vetcare.

Another option that may be open to underwriters is switching currencies to include more euro debt if sterling funds prove hard to raise. Swaps and other types of price and structural flex can be very useful in terms of mitigating a bank’s syndication risk. But, an arranger cautions, swaps are not a "magic bullet" if the credit is weak.

Thin demand

Sterling liquidity has always been thin compared with euros, and institutional investors have become even more selective on credit and are quicker to reject a deal in syndication, said a London-based banker with a mandate for a U.K.-based borrower. By comparison, on a euro-denominated credit lenders are more willing to commit at the right price.

Loans denominated in pounds typically pay 75 to 100 basis points more in coupon than an equivalent euro facility. But a benchmark for euro loans, and the premium, is yet to be firmly established this year after the unsettled end to 2018.

For a "first-quartile" credit in sterling there will be buyers, but the appetite doesn’t currently go much further down the spectrum, the London-based banker said, adding that this attitude became more entrenched during the fourth quarter of 2018 as the reality of the U.K.’s departure kicked in. At the same time, investors including CLOs that might previously have committed small sterling tickets and swapped to euros backed off.

Along with banks, this leaves private credit and direct lending firms as key lenders. The "saving grace" for the sterling loan market is that this pool of liquidity has grown in recent years, said the arranger, but many of these funds are cautious on credit and a borrower that wants a substantial volume of debt will need to go into the euro market.

Another banker suggests 300-400 million pounds might be do-able for the right deal. As an example, IVC has raised 432 million of its term loan in sterling, and is looking to raise another 350 million sterling equivalent in euros.

Tilney Bestinvest Group Ltd. was the last sterling deal launched in 2018. Following a protracted sell-down, that was priced in December at 500 basis points over Libor at a discount of 97. Now, an arranger suggests 525 basis points at 99 as a potential starting point for new sterling term loans. In comparison, new CLOs in Europe will be looking for loan assets denominated in euros that pay at least 400 basis points.

(Ruth McGavin and Sarah Husband are leveraged finance strategists who write for Bloomberg. The observations they make are their own and not intended as investment advice.)

To contact the reporters on this story: Ruth McGavin in London at rmcgavin1@bloomberg.net;Sarah Husband in London at shusband@bloomberg.net

To contact the editors responsible for this story: Tom Freke at tfreke@bloomberg.net, V. Ramakrishnan

©2019 Bloomberg L.P.