The Next Round of Bank Scandals Will Be Personal

The Next Round of Bank Scandals Will Be Personal

(Bloomberg Opinion) -- Since the financial crisis, banking scandals have been expensive; now the attention may turn increasingly personal.

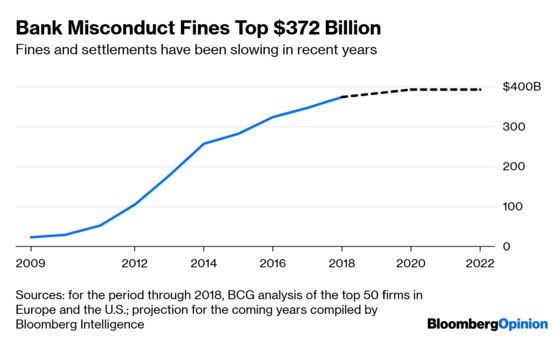

After more than $372 billion of fines, significant progress has been made in getting the industry to root out wrongdoing. Just last week, the European Commission fined five companies a total of 1.1 billion euros ($1.2 billion) for colluding in the foreign-exchange market.

Financial firms, still facing probes into their conduct in the bond market and their anti-money laundering controls, face another $20 billion or more of sanctions in coming years, according to Bloomberg Intelligence. The slowdown suggests the era of record fines may just be drawing to a close.

The industry has come far since the crisis. Regulators have clamped down on excessive risk-taking and incentives have been shifted. Compensation can now be clawed back from employees for errant behavior, and bonuses are paid out over a period of years.

The result is that banks appear to be far better equipped to decide how to deploy their balance sheet and to enforce rules against market abuse. But there’s one area to which less attention has been paid, and where firms are looking increasingly vulnerable: The personal conduct of their employees.

In the aftermath of the financial crisis, market practices that had gone unquestioned – almost to the point they were condoned – were rightly challenged. The same can be said for how individuals carry themselves in relation to colleagues and society more broadly. The #metoo movement has helped crystallize the type of behavior that should not be acceptable.

In 2018, the number of complaints to Britain's Financial Conduct Authority about harassment, bullying and homophobia jumped by 220 percent, according to the Financial Times. Of the 58 directors the regulator was investigating in December, 27 were being probed over failings of culture and governance, the newspaper said.

Non-financial misconduct matters because it cannot be separated from an employee's conduct in the workplace. It's just another form of bad behavior, as the FCA has recognized.

The cost to investors may not be so great in absolute terms, although it will only gain in importance as greater attention is paid to companies’ environmental, social and governance standards.

This threatens to be an even more uncomfortable form of scrutiny – and there are troubling signs that banks are out of step with the times.

Last year, HSBC Holdings Plc let its head of global markets lecture employees on the topic of conduct while he was under internal investigation for alleged sexual harassment, Bloomberg News has reported. The manager was also the bank’s most senior employee in meetings with the Federal Reserve while under probe.

An email from a horrified employee to the CEO might just have given the matter the appropriate degree of urgency after a probe that had lasted months. A few weeks after the town hall, the bank announced the global markets chief was retiring.

In another case, UBS Group AG’s handling of an allegation of sexual harassment has drawn the attention of the FCA. Five months after first suspending the alleged perpetrator, UBS still hadn’t started a formal disciplinary procedure and the individual left the Swiss lender, according to Bloomberg News. The FCA is now considering a formal review of whether the alleged rapist and a supervisor of the victim met the regulator’s own conduct standards, the Financial Times reported Friday.

Tackling these kind of issues will take time, and there will be missteps. While finance leaders have long vowed to change banks’ ways, the pace of adjustment lower down the ranks has been slow. As part of its work to create a healthier environment, the FCA will bring together mid-level managers and leaders later this month to help empower those below senior management to drive culture change.

More diverse leadership would help. While there are pockets of finance, such as asset management, where women are now running a number of businesses, the same cannot be said for banking. Overall, female executive representation in banking and financial services increased to 16 percent in 2017, up from about 13.3 percent in 2013, according to a study by Refinitiv.

There will always be bad apples – and more big banking mishaps cannot be ruled out. Past scandals have focused on widespread mis-selling, rigging and corruption. Expect how individuals conduct themselves away from actual dealmaking to get more attention in the future. It will be an uncomfortable adjustment.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Elisa Martinuzzi is a Bloomberg Opinion columnist covering finance. She is a former managing editor for European finance at Bloomberg News.

©2019 Bloomberg L.P.