Bank of America Forced to Grind With the Fed on Pause

Bank of America Forced to Grind With the Fed on Pause

(Bloomberg Opinion) -- Bank of America Corp. didn’t sugarcoat the path forward for investors when describing its first-quarter results on Tuesday.

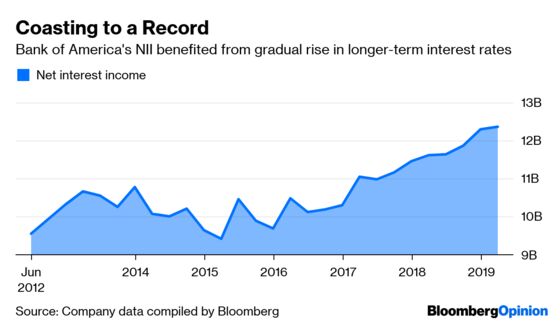

Yes, the bank generated a record profit, thanks to net interest income at its consumer unit. But Chief Executive Officer Brian Moynihan and Chief Financial Officer Paul Donofrio didn’t hide the fact that the pace of growth in NII was bound to slow this year, given that the Federal Reserve is most likely done raising interest rates for the foreseeable future. NII, remember, is the difference between revenue from loan payments and what the company pays depositors. In the rising interest-rate environment of the past two years, that spread has widened because large banks have been slow to increase yields on retail accounts.

During an analyst question-and-answer session, Moynihan was forthcoming when asked what levers he and the rest of his management team could pull when the broader economic backdrop wasn’t so favorable for banks.

“A lot of talk over the last few years about what was the contribution of rates — half of it came more or less from rates, and half of it came from hard work. We expect the half that came from hard work to keep coming...”

“We feel good just grinding out more customer relationships and more loans and deposits and more wealth management business from them. That will give us an ability to grow pre-tax in the mid to upper single digits...”

“As I think about it overall, this is a great franchise and we’re just grinding out the growth that’s embedded in it. That will produce, as we’ve said, mid-upper single digit operating earnings increase, combined with share count, will get you in double digits, and that’s pretty good.”

Promising to work harder and grind for everything is a nice thing to say, and it’s certainly better for investors than hearing the opposite. But it’s also something that any company can pledge. As long as the U.S. economy keeps plodding along at a decent clip (say 2 percent), management is confident it can outpace that growth. Donofrio said NII would probably increase 3 percent for 2019, down from 6 percent last year and 5 percent in the first quarter. That real talk sent Bank of America shares down as much as 2.8 percent to $29.

The uncomfortable truth for Bank of America and other huge retail banks is that they’ve stretched NII as far as they can on the backs of savers. Its net interest yield in the first quarter was 2.51 percent when the average 10-year Treasury yield was just 2.65 percent. How is that possible? Because the rate paid on consumer deposits is a mere 0.09 percent. For the most part, individuals have stuck with the big banks over the past few years even as the Fed boosted short-term rates nine times.

Perhaps consumers are just used to getting paid nothing to store their money since the financial crisis. Maybe the ever-evolving technology that comes with bank accounts is worth more to people than a few extra basis points of interest. Either way, it doesn’t seem as if Main Street is interested in parking cash in an online savings account — Goldman Sachs Group Inc.’s Marcus pays a 2.25 percent annual percentage yield, for example — instead of with Bank of America or JPMorgan Chase & Co.

In that sense, the flattening curve of the past two years never really mattered to companies like Bank of America. Suppose two-year Treasury yields rose 8 basis points and 10-year yields rose just 2 basis points. That would result in a major curve flattening move. But if the rate on deposits doesn’t budge at all, those couple of basis points on the long end are still a win for the banks. Last August, my Bloomberg Opinion colleague Stephen Gandel sought to quantify this payday.

The tailwind of expanding net interest margins represented relatively easy money. With interest rates now locked within a tight range, Moynihan appears to realize it’ll be a grind once again to deliver the kind of profits that shareholders expect.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2019 Bloomberg L.P.