Australia QE Program Shows ‘Signs of Success’ in First Week

Australia’s QE Program Shows ‘Signs of Success’ in First Week

(Bloomberg) -- Australia’s central bank is one week into buying government bonds in order to lower interest rates across the economy and the early verdict: so far so good.

The Reserve Bank of Australia has bought A$21 billion of securities ($12.8 billion) since last Friday, after setting an objective for three-year government bond yields of 0.25%, the same as the cash rate. That yield fell today to just 1.2 basis points above the target, while signs of funding stress in money markets have eased.

“A week into the RBA’s QE program and there are some signs of success,” said Martin Whetton, head of bond and interest-rate strategy at Commonwealth Bank of Australia.

The RBA is running two tracks at the moment with bond buying: one to return order to the market and the other to bring down borrowing costs in the economy via yield curve control. It got off to a good start as the initial announcement sent three-year maturities down toward the 0.25% target.

The central bank on Friday focused on shorter-end securities for a second consecutive day, buying A$3 billion of federal government notes maturing between May 2021 and April 2023.

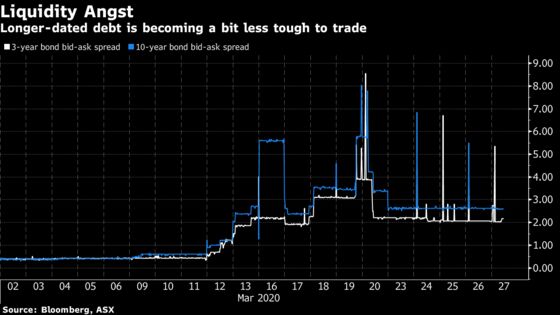

The spread to 10-year yields has dropped by almost half from last week’s six-year peak and the gap between three-month bank bill rates and overnight indexes swaps -- a key measure of how banks can readily raise funds -- is back down close to its five-year average.

Maximum Impact

The RBA is taking advice from the Australian Office of Financial Management, the government’s borrowing agency, which is closely connected with the market through its dealer panels. This relationship helps the RBA decide what lines to purchase along the curve to achieve maximum impact.

The government’s funding arm said Friday it will sell bonds next week for the first time since March 18. Prime Minister Scott Morrison’s ambitious fiscal stimulus plans to combat the virus’s impact on the economy mean the government will need to accelerate borrowing in coming months. The AOFM will auction A$1 billion of two-year bonds on Monday and then A$600 million in 2030 securities next Friday. It will also offer A$2.5 billion of T-bills on Thursday, the biggest offering of zero-coupon securities since December 2012.

The auctions signal that the RBA’s success in calming the market has been greatest at the shorter end. The longer-end was at times last week almost frozen, with yawning bid-ask spreads signaling an unwillingness for investors to trade some of the securities. Even as yields have come down more for higher maturities, it is clear that part of the market may be too fragile to absorb too much issuance just yet.

To date, the bank has received good attendance at its bond-purchase auctions, allowing it to see a full range of prices. This has allowed the RBA to field offers that are close to, or a bit above mid-market.

That basically means the RBA is getting these bonds a little cheaper than current market price and suggests dealers want to offload the stock. The other offers to sell at higher prices -- that are missing out at the auctions -- tell the RBA that while more dealers would be happy to offload, they’re not desperate to do so.

What Bloomberg’s Economists Say

“It’s taken the RBA under a week to demonstrate second mover advantage in the unconventional monetary policy game. Having learned from other central banks has seen the RBA unleash daily bond tenders across multiple maturities and issuers, in differing sizes. Flexibility has seen early wins, but the real challenge lies ahead as fiscal policy stirs and issuance picks up.”

James McIntyre, economist

It was a similar case with the state treasury corporations when the RBA bought semi-government bonds. The announcement helped narrow the difference between state and federal bonds, known as Semis and ACGBs.

On Tuesday, the central bank offered to purchase four lines of bonds and only three were bought. The fact that no one needed to sell July 2022 maturities told the bank that the market is happy with its holdings and there’s no real problem in that space. The RBA can then turn to pockets where there’s inventory on balance sheets that people want to get rid of.

“The long end remains driven by global factors. We expect to see semis narrow to ACGB and swap, which will help the market function, but this may not be immediate,” said Whetton.

The RBA also this week conducted FX swaps for dollars, acting as an agent for the Federal Reserve, in which it offered to deal $10 billion and ended up selling just $50 million. While the minimal response might look like a failure, in reality it simply highlights that there’s no big dollar crunch Down Under.

©2020 Bloomberg L.P.