AT&T’s Debt Load Slows Its Metamorphosis Into Media Powerhouse

AT&T’s Debt Load Slows Its Metamorphosis Into Media Powerhouse

(Bloomberg) -- When AT&T Inc. acquired Time Warner Inc., investors fretted that show business was going to become a big distraction. But it’s the debt from that deal that’s turned into the real headache.

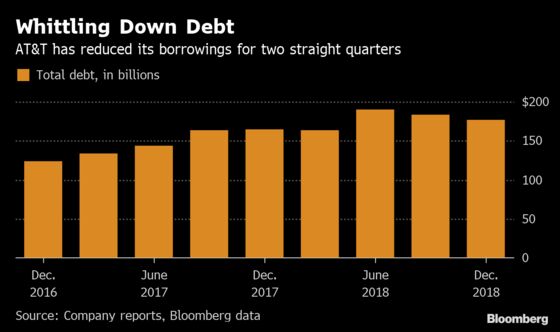

AT&T framed the $85 billion acquisition as a transformative move, giving the company the best films and TV programs to pipe into homes, mobile phones and tablets, and positioning the telecom giant to parry Netflix Inc.’s assault on pay TV. But a $176.5 billion debt pile is standing in the way, slowing AT&T’s ability to deliver on those promises.

“There’s a whole wish list of things that aren’t getting done until they improve their balance sheet,” said Jennifer Fritzsche, an analyst with Wells Fargo Securities who has a neutral rating on the stock.

AT&T, which reports financial results Wednesday, is under pressure to stem the loss of customers at DirecTV, win back mobile customers, build a 5G network, boost the dividend, develop an advertising business, fund new film and TV hits, and launch an HBO-centered streaming service. Yet topping the list of priorities is reducing how much it owes.

“We have one focus, paying down debt,” Chief Executive Officer Randall Stephenson said last month at a presentation in Washington.

The fiscal handcuffs have been clapped on AT&T at a time when the media and wireless industries are changing quickly, and a pause on any front could be risky. The company will need to spend many billions of dollars alone to create new 5G wireless businesses -- for airwaves, for a land-based fiber-optic backbone and for the new services consumers will want from a super-fast mobile network. To grow, WarnerMedia will also need money.

“If they stay committed, they can deleverage pretty quickly,” said Dave Novosel, an analyst at Gimme Credit. “They just have to avoid pitfalls like not spending enough on M&A, capital investments and spectrum purchases.”

Stephenson is making progress on that first front, showing two straight quarters of shrinking debt. The company has cut back on discounts for new phones, eliminated free trial offers for DirecTV customers and has raised prices for current subscribers. AT&T is also selling assets, like a stake in the Hulu video service and its New York office, to chip away at the debt.

The company has told investors it will raise between $6 billion and $8 billion by selling noncore assets. That should help deliver enough cash for the company’s $2.04 a share annual dividend, according to analysts at Bloomberg Intelligence.

What Bloomberg Intelligence Says

“AT&T’s sale of its minority stake in Hulu for $1.43 billion increases the company’s leeway to use free cash flow for dividend payments.”

--John Butler, telecom analyst

Click here to read the research

But the company also needs to move ahead on Stephenson’s plan to use its satellite, internet and wireless networks to deliver live TV, news, sports, and libraries of movies and shows like “Game of Thrones” and “Friends” to growing legions of subscribers. AT&T has steadily lost pay-TV subscribers since acquiring DirecTV for $49 billion in 2015 and has yet to prove that owning Time Warner can change that or squeeze a lot more from current customers.

Efforts to digest Time Warner have been also been hampered by top-level turnover, with the heads of HBO, the Turner networks and Warner Bros. all out the door.

“There’s a show-me situation now,” Novosel said. “They need to make it work.”

Investors haven’t had much to cheer about. AT&T lost an alarming 658,000 video customers in the fourth quarter, and posted its first ever annual decline in regular monthly wireless subscribers as it backed off lower-priced offers.

This quarter, analysts expect AT&T to lose hundreds of thousands of video customers, with wireless subscribers declining by more than 50,000.

Since the Time Warner deal closed on June 16, AT&T shares are down about 3 percent. Its closest peer, Verizon Communications Inc., which has far less ambitious media plans, is up 21 percent. Though Verizon’s annual revenue is $40 billion less than AT&T, its market value is more than $5 billion higher.

Add to that, AT&T is under pressure to deliver on its promise of releasing a vaguely Netflix-like streaming service in the fourth quarter. When it arrives, the company will be late to an already crowded field that includes Google’s YouTube TV, Amazon.com Inc., Netflix and Dish Network Corp.’s Sling TV. Walt Disney Co., the majority owner of Hulu, unveiled plans this month for its Disney+ family online video service.

“It’s like they are fighting a war on two fronts: deleveraging and integrating Time Warner,” said Todd Lowenstein, chief equity strategist at Highmark Capital Management. “The enormous debt leverage further compounds the problem and makes the model’s proof of concept mission critical to investors as they consider the sustainability of the dividend.”

To contact the reporter on this story: Scott Moritz in New York at smoritz6@bloomberg.net

To contact the editors responsible for this story: Nick Turner at nturner7@bloomberg.net, Rob Golum

©2019 Bloomberg L.P.