As Virus Spirals, Markets’ Bullish Bent Proves Tough to Dislodge

As Virus Spirals, Markets’ Bullish Bent Proves Tough to Dislodge

(Bloomberg) -- Anyone who used China’s health scare as an excuse to bail from stocks or redouble bets on bonds is learning again how hard it has become in American markets to shake investors of their optimism.

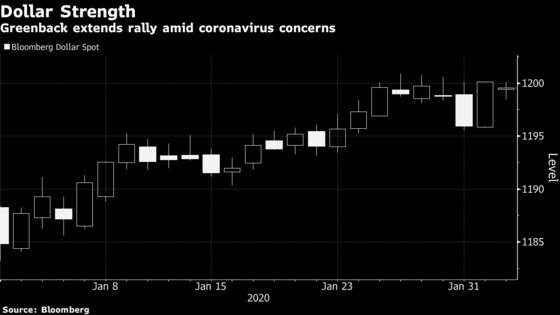

Even in a world ruled by fear over the scope of the coronavirus outbreak, risk assets are proving impossible to hold back whenever the pace of news flow levels off. Equities as measured in the S&P 500 are having the best two-day surge since October, while 10-year Treasury yields have now climbed the most in almost two months. The yen, a currency haven, is lower for the year again and credit spreads are contained.

That it’s happening as infection rates show no sign of slowing is testament to both the cold-blooded logic of traders and the persistent strength in the global macro backdrop. Convinced there’s no way to assess how bad the virus will get, they’re clinging instead to what they can confirm: especially solid U.S. earnings, a rebound in manufacturing data and a drumbeat of assurances from the Federal Reserve.

“We’ve seen this repeatedly -- May, August, October, and now -- external shocks, political and geopolitical events have difficulty slowing down the U.S. equities on the way up,” said Paul Christopher, head of global market strategy at Wells Fargo Investment Institute. “The long-term impact of the virus is still unknown, but the attention has shifted to things that are more predictable, like monetary policy.”

Coronavirus fears have dominated sentiment since mid-January, with infections topping 20,000 and the death toll rising to 425. Headlines on the outbreak sent the U.S. stock market to its worst days since August last week, while this week has seen two of its best.

With underlying data pointing to an expansion, several Wall Street strategists have reaffirmed outlooks. The virus shouldn’t derail the economy, Morgan Stanley’s Michael Wilson wrote in a note. Unless a pandemic develops, economic volatility will remain low, Evercore ISI’s Dennis DeBusschere said Tuesday.

“The data has been solid, inventories are low and consumption is firm,” DeBusschere, the firm’s head of portfolio strategy, wrote. “Given the collapse in yields and only a potential short-term impact on EPS, stocks are unusually attractive relative to bonds.”

Strategists in currencies and bonds markets haven’t rushed to alter forecasts. Despite the dollar’s best start to a year since 2016, Paresh Upadhyaya, a portfolio manager at Amundi Pioneer Asset Management, says the currency will still lose ground once global economic growth rebounds after the virus is contained.

“My outlook for a recovery in global growth has been delayed, not derailed,” Upadhyaya said Friday. China over the weekend moved to shore up its markets and economy with a massive injection of stimulus, bolstering optimism any downturn won’t have a lasting impact.

Eaton Vance maintains a “somewhat” weaker dollar position, said Eric Stein, the firm’s co-director of global income. In the Treasury market, JPMorgan Chase & Co.’s Alex Roever is convinced 10-year yields will move back just above 2% by year-end despite any haven bid. They hovered near 1.6% Tuesday.

The downturn in global factory data is likely ending, JPMorgan equity strategists wrote, with the signing of the phase one trade deal providing a boost. A gauge of U.S. manufacturing rebounded sharply in January, with the Institute for Supply Management’s purchasing managers’ index surging above the level that signals expansion.

“The latest health scare poses a significant risk to our constructive call, and could lead to continued de-risking in the short term,” strategists led by JPMorgan’s Mislav Matejka wrote in a note. But, they said, “the fundamental backdrop is supportive, and the fallout from the outbreak is unlikely to hurt activity prints over the medium term.”

Fourth-quarter earnings results have outpaced expectations, offering “a port in the storm for stocks,” according to Gina Martin Adams, an analyst with Bloomberg Intelligence. The S&P 500, with 227 reports through Monday, is set to post an EPS decline of 0.3% versus a year ago, she wrote in a note this week. Earnings were forecast to shrink by 1.9% heading into the season.

To be sure, the latest economic data and earnings reports describe periods prior to the virus outbreak. Treasury yields remain near the lowest since September and a key part of the yield curve recently inverting again, reviving concern about a potential slowdown in the U.S. The outbreak will cut U.S. first-quarter economic growth by 0.4 percentage point, Goldman Sachs Group Inc. said, as the number of tourists from China plunges and exports to the Asian nation slow.

Risk assets had been rallying since October, when the Fed began buying $60 billion of Treasury bills per month. The central bank said last month it would extend through April a program aimed at smoothing out volatility in money markets. Chairman Jerome Powell suggested the central bank stands ready to act if the coronavirus looks likely to hamper growth.

But to Gary Bradshaw, a portfolio manager at Hodges Capital Management, the recent pullback was an opportunity to add to some of his tech holdings.

“Those that missed the rally late last year and were looking for an opportunity to jump in used the pullback to put money to work,” he said by phone. “Nobody knows what the virus will amount to. But what’s giving investors optimism is solid earnings, good economic growth and low interest rates.”

--With assistance from Vivien Lou Chen, Elena Popina and Robert Fullem.

To contact the reporters on this story: Vildana Hajric in New York at vhajric1@bloomberg.net;Susanne Barton in New York at swalker33@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Chris Nagi

©2020 Bloomberg L.P.