Argentina Turns to Orthodox Policy Signals to Ease Dollar Craze

Argentina Turns to Orthodox Policy Signals to Ease Dollar Craze

(Bloomberg) -- After failing to stem a run on its currency with heavy-handed restrictions, Argentina is shifting tack and has begun adopting more orthodox economic measures to try to shore up investor confidence and lure capital back into the country.

It curbed growth in the money supply in October, raised interest rates and promised not to finance itself with temporary advances from the central bank in the short term, backtracking on some of the most expansionist monetary policies implemented as the pandemic hit.

The move represents Argentina’s latest attempt to curb demand for dollars after the peso plunged 24% this year in official foreign-exchange markets. Restrictions on accessing greenbacks have pushed investors and mom-and-pop savers seeking to protect themselves from inflation into parallel markets used to skirt capital controls, where the peso is 51% weaker.

“Although for now this shift is insufficient, it’s a sign they’re not moving further toward heterodox policies,” said Miguel Kiguel, an economist at the Econviews consultancy.

Argentina is facing a crisis on many fronts, with the economy expected to contract around 12% amid the coronavirus pandemic and inflation forecast to end the year at about 40%. Even after a $65 billion debt restructuring, borrowing costs are so high that the country can’t fund itself through debt markets, instead turning to money printing by the central bank.

Foreign investors are watching: BlackRock Chief Executive Officer Larry Fink said Thursday that the country had a long way to go before it could recover trust. On Friday, Walmart Inc. said it agreed to sell its business in Argentina to a local group.

The ruling leftist alliance has a reputation for shunning orthodox policy options, such as raising policy rates, and instead turning to obscure market restrictions and calls for patriotism to help fix issues such as the gap between the official and parallel currency. It’s a government that has also been willing to finance itself through central bank cash transfers.

An Economy Ministry official said that the government does not take orthodox or heterodox approaches, but rather only pragmatic approaches. It aimed to reduce public spending but that was upended by the pandemic, the person added.

Here are the measures the government has put in place in recent weeks:

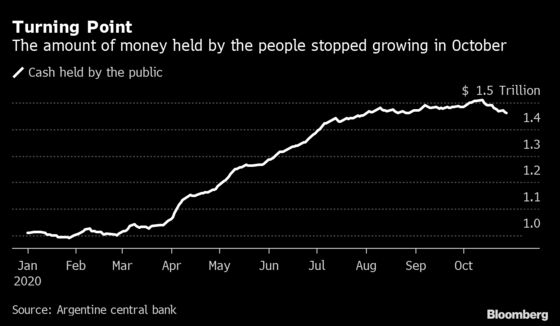

1. Peso expansion slows

The amount of cash held by the public has plateaued since August. The growth rate in the money supply, which had reached 83% per year in August, slowed to 81% in October. Analysts had cautioned that the ballooning number may lead to higher inflation.

“The excess of pesos is still high,” Kiguel said. “But the government is trying to be more careful. It’s a turning point, which shows that something has changed.”

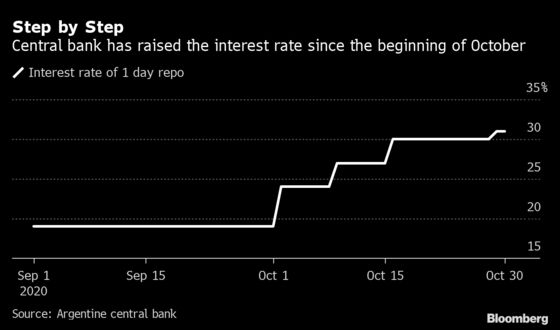

2. Interest raise increase

The central bank started raising interest rates on its 1-day repo notes on Oct. 1 to an annualized 31% from 19%. At the same time, the benchmark Leliq rate fell to 36%, from 38%. The weighted average on the two rates rose to 34.2%, from 32.6%, according to Diego Chameides, the chief economist at Banco Galicia in Buenos Aires.

That’s a reversal that contrasts with the government’s decision early in its administration to lower rates that had been as high as 85%. It should also help ease some of the pressure on the parallel peso, which has recently strengthened after touching a record low in October.

“This is a measure in the right direction, but it will probably be necessary to raise the rate further, given the higher expectations of inflation and exchange rate depreciation for the coming months,” Chameides said. Implied rates on the futures market suggest that a 45% devaluation of the peso is expected by October 2021.

3. Lower peso expansion

The government said this week it won’t ask for any more transitory advances from the central bank this year, but rather aims to obtain financing in local bond sales and use those proceeds to curb its requests from the monetary authority. It may still seek as much as 400 billion pesos ($5 billion) from the central bank through another avenue of money printing, known as dividend transfers.

Reducing the amount of peso issuance should also help curb demand for the dollar. It will likely ease the risk of ballooning inflation next year, said Alejo Costa, chief Argentina strategist for BTG Pactual in Buenos Aires. The timing is ideal ahead of a visit by an International Monetary Fund mission later this month to discuss a new program, says Costa.

“I think they at least want to show that they are not extreme, that an agreement with the IMF is possible with a gradual adjustment of monetary financing and the fiscal deficit,” he said.

©2020 Bloomberg L.P.