Argentina’s Dueling Peso Rates Threaten to Freeze NDF Market

Argentina’s Dueling Peso Rates Threaten to Freeze NDF Market

(Bloomberg) -- Argentina’s chaotic return to capital controls is claiming another casualty: The $530 million mechanism that allows exporters, importers and companies to hedge future debt payments.

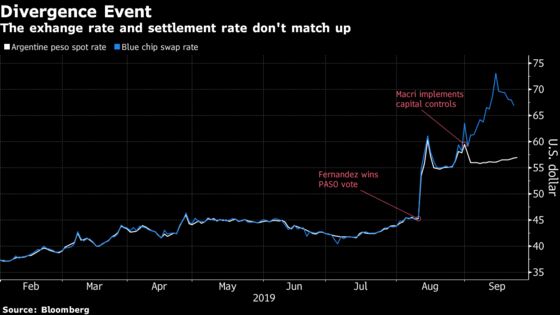

At issue is the rapid divergence between the nation’s official exchange rate and the so-called blue chip rate in the tumultuous three weeks since President Mauricio Macri imposed capital controls to stave off default amid investor panic after his unexpected primary defeat. Since the unofficial rate is 15% weaker, the settlement rate for non-deliverable forwards is open to question.

It’s such a worrisome situation that Goldman Sachs Group Inc., Pacific Investment Management Company LLC and at least three other firms notified the Emerging Market Traders Association, a powerful industry group that sets certain investing guidelines. That triggered price disruptions on Monday and Tuesday in some NDF contracts, postponing valuation either until two rates again converge or 30 days pass, according to the trade group.

“The doubts of the fixing opens a vacuum, both for investors and the dealers,” said Alejo Costa, a strategist at BTG Pactual Group in Buenos Aires. “The market will likely freeze.”

Read More: EMTA Notified of Exchange-Rate Divergence in Argentine Peso NDFs

Just $528 million of Argentine NDFs and other derivatives trade daily, a fraction of the $7.6 billion that change hands each business day across the border in Chile, according to the Bank for International Settlements. While the market remains open, the twin exchange rates mean it’s less likely traders will be willing to strike contracts. Yet it’s a key market for firms that need to hedge debt, especially in the short term.

Without clear and valid pricing, it will be difficult to keep the NDF market alive, according to Dirk Willer, head of emerging-market strategy at Citigroup Global Markets Inc. in New York. If enough members were willing to flag a divergence one day, there’s no obvious reason they wouldn’t the next, he said.

“The market probably disappears,” he said in an interview. “It seems somewhat hard to come up with a mechanism that allows the NDF market to function.”

It’s doubtful that the blue-chip rate will replace the one set at the Mercado Abierto Electrónico in Buenos Aires, said BTG’s Costa. Yet since capital controls began, the MAE fixing is “irrelevant for financial transactions,” he said.

For investors who wrote to the EMTA, including Pimco’s Ismael Orenstein, that parallel rate represents how actual transactions are being priced.

“In other words, the USD/ARS spot rate quoted in the ARS MAE (ARS05), the local onshore spot market, does not represent the actual rate of a financial transaction by an investor,” the Newport Beach, California-based investor wrote in his notice. “Instead, the rate at which an investor can actually transact in USD/ARS foreign exchange transactions is the [blue chip swap] rate.”

Cargill Inc., Amia Capital LLP and King Street Capital Management were among the money managers that sent notices to EMTA.

--With assistance from Ignacio Olivera Doll and Carolina Millan.

To contact the reporter on this story: Sydney Maki in New York at smaki8@bloomberg.net

To contact the editors responsible for this story: Carolina Wilson at cwilson166@bloomberg.net, Alec D.B. McCabe

©2019 Bloomberg L.P.