Argentina Debt Restructuring May Be Shaped by Just Two Words

Argentina Debt Restructuring May Be Shaped by Just Two Words

(Bloomberg) -- As Argentina looks set to restructure its debt, bondholders are trying to grasp the implication of two words written into most bond sales worldwide since 2014.

The debate is around a “uniformly applicable” rule that sits in the collective action clauses (CACs) that comes into play in case of a debt restructuring. If the government chooses to sign a single accord with bondholders, the clause implies all investors have to be treated the same -- whichever bond they hold and whatever its current value.

That option, known as single-limb vote, requires the backing of investors that hold 75% of the outstanding value of the bonds to be restructured. In the case of Argentina, it would then mean investors who hold a range of debt maturing from 2021 to 2117 are offered the same replacement asset or set of assets. And there’s the rub.

“Anytime you have a new standard and the standard promises some kind of equal treatment between creditors, that is a concern in a restructuring because creditors can always come up with arguments that they are not getting equally treated,” said Mark Weidemaier, a law professor at the University of North Carolina.

Argentina could be the first country in the world to test the new clause -- thus the confusion. Back in 2001, the Latin American nation defaulted on $95 billion of debt, before restructuring most of the bonds in 2005 and 2010.

A group of holdouts rejected the earlier offers and sued for full payment, citing an equal treatment -- or “pari passu” -- clause in the bond documents, which prevented Argentina from treating defaulted bondholders less favorably than exchange bondholders. The collective action clauses and the “uniformly applicable” wording is designed to avoid a repetition of those events.

Two Limb

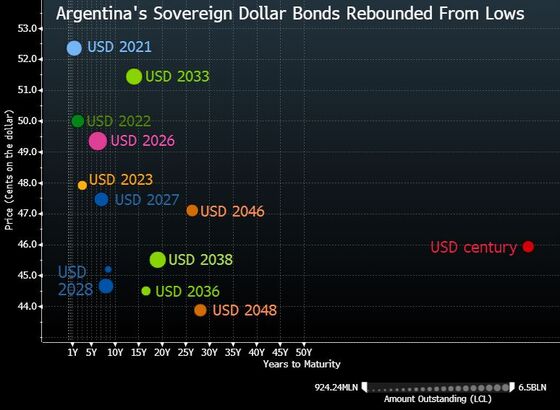

A single replacement bond would generate different returns to people that hold bonds maturing in two years or in a century. Far from applying the “uniformly applicable” rule, some investors may interpret that as the opposite.

A dispute could force Argentina’s government into a longer restructuring process in which it would need to negotiate with holders of all bonds -- a so-called second limb vote. That would require the support of just 66.67% of all bondholders in the restructuring, but also 50% of the holders of each note.

Read more about CACs: Fine Print on Argentine Bonds Becomes Crucial as Default Looms

A group of bondholders expects Argentina to pursue a single-limb vote, according to a person that is part of the negotiation but isn’t allowed to speak publicly.

Argentina’s debt load stands at $332 billion, including loans from the International Monetary Fund. Outstanding debt with private bondholders is about $148 billion. On Friday, the government announced it will delay again payments on its dollar-denominated notes known as Letes until Aug. 31 2020.

Divide and Rule

New President Alberto Fernandez has said Argentina is unable to pay its debt under current conditions and will start talks with the IMF and bondholders. The government hasn’t provided any details on how much it will renegotiate, how or when.

“The use that Argentina could give to the single limb or the two limb will depend on the terms of the proposal and also the market conditions,” says Eugenio A. Bruno, a Buenos Aires-based lawyer specialized in sovereign debt.

The uniformly applicable clause was added globally to ease investor concerns that debt issuers could differentiate between bondholders, offering better terms to some. The Argentine bond prospectus says the issuer has to offer “the same new instruments” or “an identical menu of instruments”.

“The way that I read the text, is just that you must give the same options to everybody,” Weidemaier said. “Bondholders are not entitled to be treated differently just because their bonds happen to have different terms or to trade at different prices.”

To contact the reporters on this story: Jorgelina do Rosario in Buenos Aires at jdorosario@bloomberg.net;Aline Oyamada in Sao Paulo at aoyamada3@bloomberg.net

To contact the editors responsible for this story: Carolina Wilson at cwilson166@bloomberg.net, Philip Sanders

©2019 Bloomberg L.P.