AB InBev Looks for a Long-Term Commitment

AB InBev Looks for a Long-Term Commitment

(Bloomberg Opinion) -- Anheuser-Busch InBev NV once tagged Bud Light as “the perfect beer for whatever happens.” Now it has to convince investors that its long-term debt should be viewed in the same way.

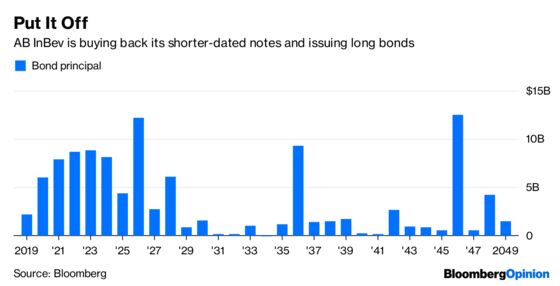

The world’s largest brewer announced on Thursday that it’s issuing $15.5 billion of bonds with maturities as long as 40 years, with proceeds used in part to buy back up to $16.5 billion of notes due from 2021 to 2026. Effectively, AB InBev is extending its more than $100 billion debt load, presumably to relieve the burden of paying higher principal payments in the next few years. In 2026 alone, it has more than $10 billion of debt scheduled to mature, more than double what it owes in 2020, according to data compiled by Bloomberg.

This is a somewhat bold move for a company that’s just a month removed from a Moody’s Investors Service downgrade to the lowest investment-grade tier. After all, analysts pinned the rating cut squarely on the fact that AB InBev’s leverage is expected to remain elevated in the near future. The brewer already opted to reduce dividend payouts to shareholders by half, which helps its cash flow. But as far as its borrowings are concerned, it appears that company officials view kicking the proverbial can down the road as the best option.

Last year, this sort of sale might have been a struggle. If the first two weeks of 2019 are any indication, though, debt investors seem to be (to borrow another Bud Light slogan) up for whatever. Buoyed by a broad feeling of risk-taking across global markets, the Bloomberg Barclays U.S. Corporate High-Yield Bond Index is up 3 percent already this year, and investment-grade company debt is outperforming Treasuries. It’s not quite a seller’s market — a junk-bond deal is finally happening, after no offerings since November — but it’s certainly a better environment than a few weeks ago.

The reason AB InBev is particularly worth watching is because it’s considered one of the leveraged behemoths that could cause chaos in the corporate debt market if its rating were ever to fall below investment grade. Others include Ford Motor Co., Campbell Soup Co. and Keurig Dr Pepper Inc. In the case of AB InBev, its liabilities soared because of its 2016 acquisition of competitor SABMiller Plc. For those who thought PG&E Corp. and its $18 billion of bonds could cause fears of a wave of “fallen angels,” imagine what a blue-chip company with five times the debt would do to investors’ psyches.

The bond pricing reflected that risk. The initial price talk for the $4 billion 30-year portion, for example, was a spread of 265 basis points above U.S. Treasuries. By comparison, AB InBev’s benchmark debt due in April 2048 traded earlier this week at a spread of just 210 basis points. When it was issued 10 months ago, the premium was 150 basis points. One last figure: To borrow for 40 years, the company went into the sale set to pay 290 basis points above long Treasury bonds.

Bloomberg News’s Molly Smith and Natalya Doris reported that the sale was said to draw orders of around $40 billion, which allowed AB InBev to increase the size of the offering. Predictably, the yield premium fell across maturities, with the 30-year and 40-year bond spreads each narrowing by 15 basis points. The company also increased the size of its tender offer for the shorter-dated notes from the initial $11 billion.

As my Bloomberg Opinion colleague Andrea Felsted noted last month after the Moody’s downgrade, there’s no quick fix for such a massive pile of debt. AB InBev is going to have to cut back on the ambitious deals and commit to the hard work of deleveraging and stabilizing its credit rating. Remember, S&P Global Ratings has had a negative outlook on AB InBev’s A- rating since March 2017. It considers the brewer’s competitive position “excellent” but its financial risk “significant.”

That can hardly be reassuring for investors considering parking their money away for decades. However, AB InBev thus far is largely moving in the right direction, even if extending debt doesn’t seem like it. This move at least gives executives some breathing room to get the company’s balance sheet back in order. Whatever happens in the coming years, similarly situated companies will most likely do the same. Because when it comes down to it, no one wants to be the poster child for a blue-chip company that became a fallen angel.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2019 Bloomberg L.P.