An Alternative to ‘No Alternative’: How Bonds Snuck Up on Stocks

An Alternative to ‘No Alternative’: How Bonds Snuck Up on Stocks

(Bloomberg) -- A common narrative in markets is that with global rates so low, equities are the only game in town for investors with an appetite for upside. But after the worst selloff in Treasuries since 1980, the edge for stocks is starting to dull.

While yields are still low relative to history, the mantra of “there is no alternative” is losing its pull with 10-year Treasury rates nearly 80 basis points higher than they started in 2021.

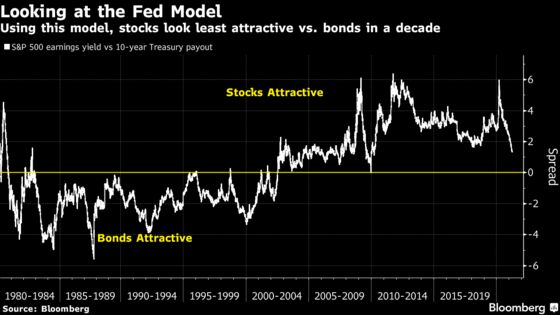

As a result, the so-called Fed model -- which compares corporate profits to bond yields -- shows that S&P 500 Index stocks are the least attractive relative to Treasuries in more than a decade. The equity benchmark’s earnings yield -- how much profits you get relative to share prices -- is about 1.3 percentage points above the yield on 10-year Treasuries. That’s the smallest advantage since 2010.

Minds are being changed thanks to the rapid repricing of the U.S. economic outlook -- nonfarm payrolls increased by 916,000 last month as more vaccines found arms and the government delivered trillions of dollars in fiscal aid. Meanwhile, as inflation expectations hit multi-year highs, Federal Reserve policy makers have made it clear that they won’t act preemptively to curb price pressures. Long-dated bond yields have rocketed higher as a result, breathing new life into the asset class after rates fell to all-time lows last summer.

“That we’ve had such a swift selloff in bonds while stocks have continued to hit new highs very much implies that the relative attractiveness of bonds is quickly improving,” said Dan Suzuki, Richard Bernstein Advisors LLC’s deputy chief investment officer.

Bonds may stay attractive for the next decade, according to a Bank of America analysis. The firm’s valuation framework -- which it says has proved 80% prescient over 10-year intervals -- forecasts returns of 2% per year over the next decade, analysts wrote in a note last month. That’s “close to levels that renders bonds compelling,” particularly if the 10-year Treasury yield hits the bank’s year-end target of 2.15%. The note yielded about 1.68% on Thursday.

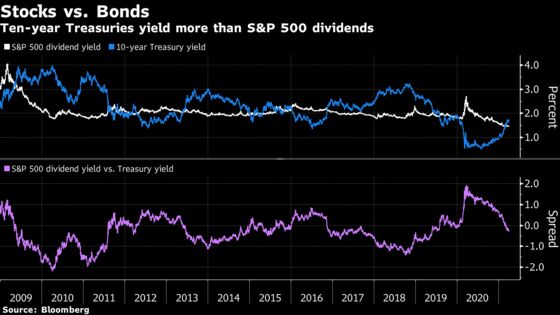

The rise in yields is also taking the shine off dividend-yield stocks. For the first time since late 2019, the S&P 500’s payout is below the yield on the benchmark note. As of Wednesday’s close, the S&P 500 had a dividend yield of 1.46%, 30 basis points below the yield on 10-year Treasuries.

On Thursday, there were 231 companies in the S&P 500 with a higher dividend payout than the 10-year Treasury rate, according to data compiled by Bloomberg. That compares with 341 companies at the start of the year.

“The 10-year yield finally passed the S&P 500 dividend yield and I think if those yields rise, it becomes a more and more attractive place to park some money,” said Ross Mayfield, investment strategy analyst at Baird. “There’s probably room for yields to continue to move higher -- 1.75% could be an attractive level. But if yields continue to rise, the price of those bonds is going to feel it. So it’s a tough balancing act for sure, but they’re becoming more attractive.”

Richard Bernstein’s Suzuki agrees. The Fed model and the dividend yield eclipse aren’t necessarily buy signals for bonds -- yet. Should the consensus in markets play out -- that the vaccine rollout will kick-start a surge in growth -- then bonds have the capacity to underperform equities further even as their valuations begin to look enticing, Suzuki said.

“But clearly, one’s interest rate outlook has a lot to do with how you view the relative attractiveness of stocks and bonds. We are in the camp that interest rates will continue to trend higher in the coming years, which makes the relative attractiveness of bonds all the worse,” Suzuki said.

©2021 Bloomberg L.P.